Investment Thesis

I recommend holding WEG (OTCPK:WEGZY) shares. In 2Q24, the company surprised the market, which believed that the incorporation of Regal Rexnord’s assets could put pressure on WEG’s margins, but that did not happen.

Once again, WEG proves its great resilience. However, the valuation is extremely stretched compared to its peers, which are also great companies, making it impossible for an analyst who follows the value investing philosophy to recommend buying.

Review Of WEG Results

The company reported strong results, and below I will analyze each segment in detail. It is worth noting that the company reports results in BRL, and I will convert them considering 1 USD = 5.21 BRL as the company reported.

Earnings Release (IR Company)

Revenues – Growth Through M&A

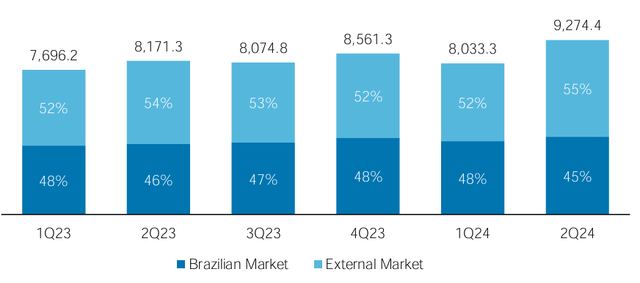

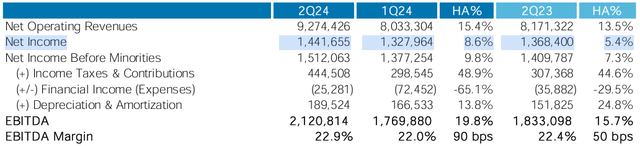

Net revenue increased 15.4% in the quarter and 13.5% in the year, reaching BRL 9.27 billion ($1.78 billion). As mentioned in the previous chapter, the result was benefited by the rise in the dollar in the period, from BRL 4.95 in 2Q23 to BRL 5.21 in 2Q24.

Net Operating Revenue by Market (figures in R$ million) (IR Company)

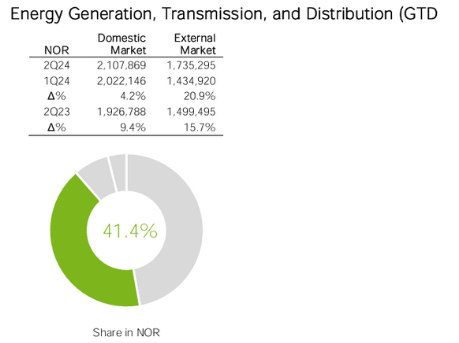

In Brazil, the highlight was the evolution of long-cycle equipment, mainly in the Energy Generation, Transmission and Distribution (GTD) unit. Short-cycle equipment was supported by the commercial motor and reducer businesses. On the negative side, the highlight was the revenue from distributed solar generation.

GTD (IR Company)

In the foreign market, the result was driven by the Power Transmission and Distribution (T&D) business in North America. Global industrial activity in segments such as Oil & Gas and Water & Sanitation was also highlighted.

I would like to remind the reader that in the quarter I will incorporate the results of Regal Rexnord, and excluding the results of Regal Rexnord, organic growth would be 9%. Finally, in my view, the diversified positioning, with presence in different geographies, markets and products, is a positive point for the company.

Costs And Margins – Incorporation Did Not Affect Profitability

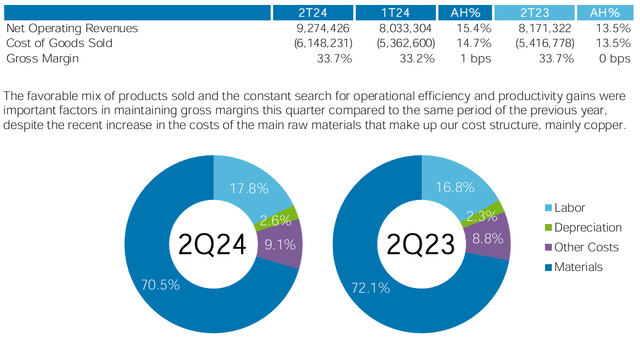

Costs rose sharply, rising by over 10% in the year and quarter. One of the reasons for this was the rise in copper prices during the period. However, since the increase in costs was lower than the increase in revenue, we saw an increase in gross margin.

COGS (IR Company)

But the big surprise in the results comes next. There was a fear that Regal Rexnord’s margins could reduce WEG’s consolidated profitability level, but this did not materialize.

EBITDA Margin (IR Company)

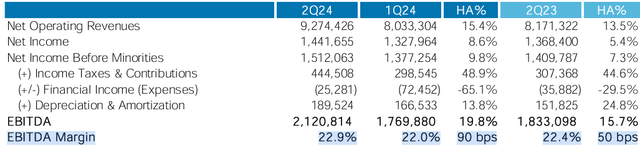

As you can see, the company achieved an incredible EBITDA margin of 22.9%, an increase of 90 bps in the quarter and 50 bps in the year. As a result, one of the risks in my thesis at the beginning of coverage did not materialize, which was that the acquisition could negatively impact results.

Net Income – As Expected

Net income increased 8.6% in the quarter and 5.4% in the year, reaching BRL 1.4 billion ($276 million) due to improved operating margins, but offset by the higher effective tax rate.

Net Income (IR Company)

I listed the risk of the higher tax rate in my coverage initiation report. The increase in the effective tax rate was expected due to the new transfer pricing regulation, which was expected to raise the rate by 200 bps to 300 bps. However, the rate came in even higher, ending the quarter at 22.5%. I believe the normalized level for 2024 onwards will be something closer to 21%.

Valuation – Still Very Expensive

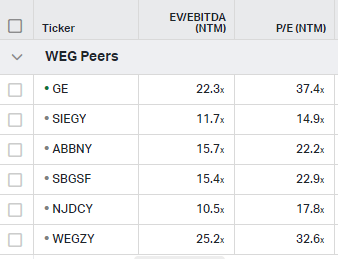

To value the company, I will use the comparative evaluation method with EV/EBITDA and P/E multiples. Thus, I will compare WEG with its peers GE (GE), Siemens (OTCPK:SIEGY), ABB (OTCPK:ABBNY), Schneider Electric (OTCPK:SBGSF), and Nidec (OTCPK:NJDCY).

Valuation (Koyfin)

When we calculate the sector average of the EV/EBITDA multiple, we arrive at 16.8x EBITDA, that is, trading at 25.2x, WEG has a 50% premium to the sector average. In the P/E multiple, we have a sector average of 24.6x, and WEG is trading at a premium of 32%.

For me, as an analyst who follows the philosophy of value investing, there is no way to recommend buying the shares, especially with revenue growing organically by only 9%.

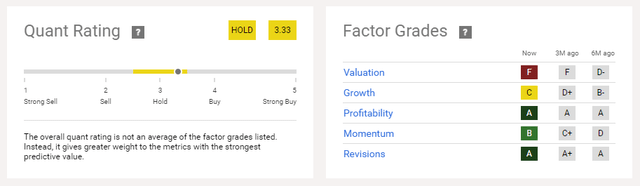

To raise the recommendation, I need the P/E multiple premium to be reduced to around 15%, making the company’s valuation fairer. Therefore, I reiterate my recommendation to hold WEG shares, and I am confident when I see that the Quant Rating and Factor grades indicate the same recommendation.

Quant Rating And Factor Grades (Seeking Alpha)

Potential Threats To The Bearish Thesis

As for the risks to my thesis, despite the company being expensive and showing a slowdown in revenue growth, it is undeniable that the momentum of the shares is very strong.

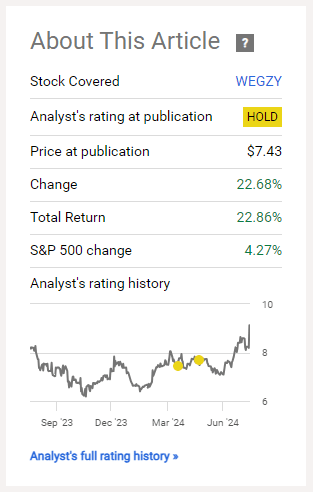

WEG: Difficulty In Maintaining Strong Growth, Valuation Appears Stretched (The Author)

Above is my report when I started coverage, with arguments in line with this report, and despite this the company has had a nice share price appreciation of 22% since April 3rd.

The risks of not investing in a company with operational excellence, although expensive, are numerous and investors must be diligent in their analyses before investing in the company.

The Bottom Line

WEG reported good results, surprising the market, which believed that the incorporation of Regal Rexnord’s assets could negatively impact WEG’s high margins.

This did not happen, which once again proves that the company has excellent managers. However, the valuation is extremely high when we look at the EV/EBITDA and P/E multiples, making it impossible to recommend a buy.

Based on this analysis, I recommend holding WEG shares. In my opinion, investors should wait for an event that implies a drop in the share price to buy the asset with a better risk/return ratio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here