Investment thesis

The Financial sector is substantially lagging behind the broader U.S. stock market this year due to massive pessimism regarding the banking industry after multiple U.S. regional banks’ failures. But my analysis suggests that one of the largest American banks, Wells Fargo (NYSE:WFC), is fundamentally strong and well-positioned to expand its business over the long term. And this strong bank’s stock is currently trading far below its intrinsic value, according to my valuation analysis. It is also crucial that the stock currently offers an attractive forward dividend yield. All in all, I assign WFC stock a “Strong Buy” rating.

Company information

Wells Fargo is one of the top four largest banks in the U.S., with a diversified portfolio of financial services and a nationwide network of several thousand branches nationwide.

The bank’s fiscal year ends on December 31 with four reportable segments: Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, and Investment Management. According to the latest 10-K report, the Consumer Banking and Lending segment contributed almost half of the banks’ total revenue in FY 2022.

Financials

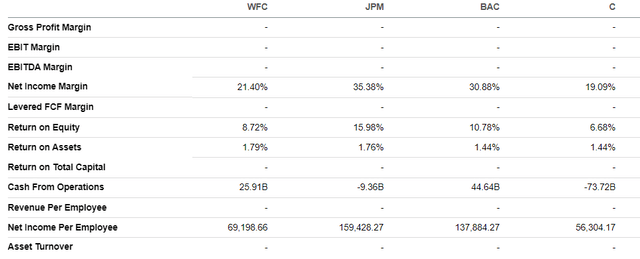

Wells Fargo got the highest possible “A+” profitability grade from Seeking Alpha Quant. On the other hand, WFC’s net income margin is notably lower than the sector median. So are the ROE and ROA. At the same time, current profitability metrics are better than the five-year averages. Among the “Big Four”, WFC’s profitability metrics are in third place, by far lower than the giants called JPMorgan Chase (JPM) and Bank of America (BAC).

Seeking Alpha

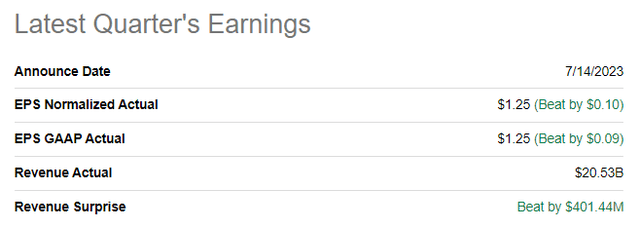

The latest quarterly earnings were released on July 14, when the bank topped consensus estimates on the top line and the EPS. Revenue showed strong growth momentum with a 21% YoY growth. The strength in revenue was primarily due to a 29% increase in net interest income, which was partially offset by an 8% drop in fee revenues. The adjusted EPS followed the top line and widened from $0.82 to $1.25.

Seeking Alpha

Financial performance in the latest quarter was strong, with double-digit revenue growth, apart from the Investment Management segment, which demonstrated a 2% YoY revenue decline. The decline in the Investment Management business looks fair in the current circumstances and temporary, not secular. What is good is that the bank demonstrates a solid ability to absorb tailwinds in the form of increased interest rates, meaning the bank is navigating the current environment successfully.

Demonstrating solid profitability and strong current growth momentum allows the bank to sustain a strong balance sheet with a Common Equity Tier 1 ratio of 10.7% as of June 30. Having a strong balance sheet allows the bank to conduct stock buybacks and pay dividends to shareholders consistently.

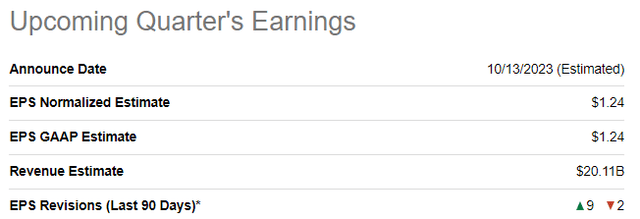

The upcoming quarter’s earnings are scheduled for publication on October 13. Quarterly revenue is projected by consensus at $20.1 billion, indicating a 3% YoY growth. The adjusted EPS is expected to shrink slightly from $1.30 to $1.24 as the increased costs will pressure the bottom line. At the same time, I think the expected deterioration of the bottom line is cyclical and not secular.

Seeking Alpha

As I always say, large banks have a substantial competitive advantage due to their massive scale, which allows them to decrease customer acquisition costs, which is crucial for the banks over the long term to maximize shareholders’ wealth. For example, WFC provides a wide portfolio of financial services, which makes it a strong “one-stop shop” for financial services. That said, the bank has substantial opportunities to cross-sell its services, meaning that once someone becomes a client of one of WFC’s business lines, he is highly likely to remain with the bank in terms of other services. Therefore, I believe that the bank is well-positioned to grow in terms of revenue and profits in the long term.

Valuation

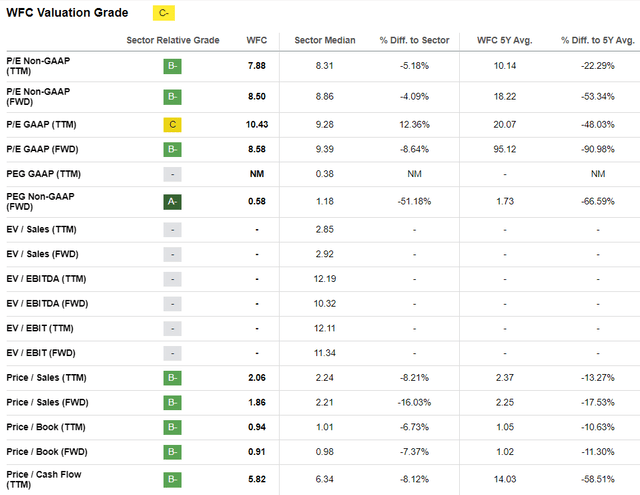

The stock declined about 1.5% year-to-date, significantly underperforming the broader market. On the other hand, WFC’s stock performance is approximately in line with the Financial sector (XLF). Seeking Alpha Quant assigns the stock a low “C-” grade, primarily due to a high TTM GAAP P/E ratio. Apart from that, multiples look decent, especially compared to historical averages. Valuation ratios related to profitability are by far lower than historical averages. Price-to-book ratios are closer to historical averages, but still, the gap is at double digits. To me, that is a clear indication of the undervaluation.

Seeking Alpha

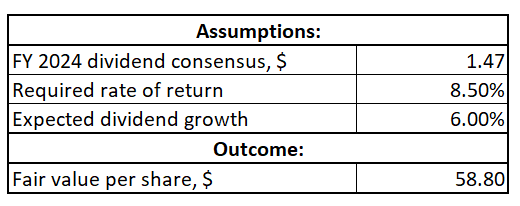

To get more conviction regarding the valuation attractiveness, I want to proceed with the dividend discount model [DDM] approach. I use an 8.5% WACC for the valuation of the largest U.S. banks, which I consider fair. I have dividend consensus estimates suggesting an FY2024 payout of $1.47. Dividend growth is tricky, and WFC has an unstable track record in recent years. I use the last three years’ sector median dividend growth rate and round it down to 6% to be conservative.

Author’s calculations

According to my DDM calculations, the stock’s fair price is almost $59. This indicates a massive 43% upside potential, making the stock very attractively valued.

Risks to consider

Wells Fargo is subject to substantial macroeconomic risks as a banking institution. Holding a large consumer loan portfolio encompassing various loan types such as mortgages, credit card debts, and personal loans, the bank’s risk is inherently related to the repayment ability of its borrowers. Currently, despite demonstrating GDP growth, the U.S. faces massive macroeconomic uncertainty. Federal Funds rates are their highest since the beginning of the century, and there is a probability that another hike might come this year. This suggests a highly likely slowdown in business activities and a potential rise in the unemployment rates. Although I do not anticipate that an increase in unemployment will drastically undermine the quality of WFC’s loan portfolio, it is very likely to influence the market’s perception of banks negatively.

Disruption from fintech is another big challenge confronting the banking sector. Being one of the oldest, the Financial sector is experiencing vast technological shifts. With an increasing number of transactions being conducted digitally, customers are showing a preference for much less time-consuming online banking services available via their smartphones rather than visiting physical branches. The large scale of Wells Fargo poses a risk in terms of effectively adapting to these changes.

Bottom line

To conclude, WFC is a “Strong Buy”. While the current challenging macro environment is undisputable, my valuation analysis suggests that the market already has priced in pessimistic scenarios for the macro environment. It is also important to mention that at the current stock price, it offers an attractive 3.4% forward dividend yield. Wells Fargo is one of the largest American banks, and it is fundamentally strong to continue expanding its business and increase value for shareholders.

Read the full article here