A shot of a pipeline construction site.

Anybody remotely familiar with the concept of passive income probably knows many of the more popular quotes on the subject from investing legends. They’ve probably even read them in articles here on Seeking Alpha numerous times.

Still, I would contend that some quotes are so filled with breathtaking wisdom that they are worth repeating. So, for the sake of this article, I’ll start with one of my favorites:

If you don’t find a way to make money while you sleep, you will work until you die. Berkshire Hathaway Chairman and CEO Warren Buffett

Regular and recurring bills are a rite of passage when somebody enters adulthood. For most just starting as young adults, they will have to earn an active income from a job or a business to support themselves. Until they earn dividends/distributions, interest, music or book royalties, etc., they will always depend on their next paycheck to live.

In my view, this is what makes income investing so appealing when it is done right. This is because it is very tangible. Brick by brick, each month of retirement and taxable account contributions moves me closer to financial independence (when passive income matches or exceeds expenses).

Western Midstream Partners LP (NYSE:WES) is a master limited partnership that I don’t own in my portfolio. However, the recent 52.2% hike in the quarterly distribution per unit to $0.875 couldn’t help but get my attention.

Today, I’ll be initiating coverage in the MLP with a buy rating. As I’ll discuss, WES’ extensive energy infrastructure network spans throughout much of the United States. The company recently brought a major growth project online. WES also anticipates that it will reach its desired leverage ratio by the end of this year, which supports its investment-grade credit ratings. Lastly, the unit price appears to be trading moderately below my fair value estimate.

More Growth Could Be Ahead After An Impressive First Quarter

WES 10-K Filing

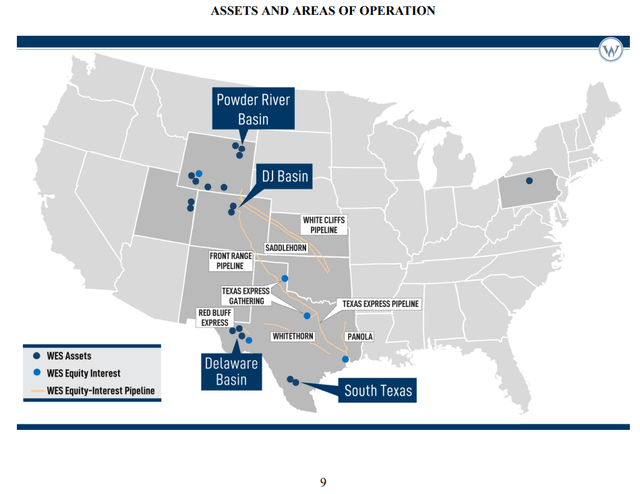

Western Midstream Partners is one of the largest publicly traded midstream companies in the United States. The company’s infrastructure is critical to supporting energy producers in many of the most energy-productive regions within the country.

WES owns more than 14,000 miles of natural gas, crude oil, and NGL pipelines. That includes seven natural gas pipelines, 12 crude oil/NGLs pipelines, 21 gathering systems, and 69 processing and treating facilities.

For more context, WES was initially formed in 2007 by Anadarko Petroleum to own, operate, acquire, and develop midstream assets. In August 2019, this shifted to Occidental Petroleum (OXY), when it acquired Anadarko.

As of May 3, OXY owned 185.2 million units of the partnership. That represents 49.9% of WES’ total outstanding units, with the other half (50.1%) being owned by institutional and retail investors.

Unsurprisingly, OXY is also WES’ biggest customer. In 2023, the energy giant accounted for 59% of the partnership’s total revenue, 34% of natural gas throughput, 86% of crude oil and NGLs throughputs, and 78% of produced water throughput.

On paper, this concentration with a relatively large customer may seem concerning. But I’m inclined to agree with fellow analyst Leo Nelissen’s observations in a recent article:

While one may make the case that dependence on one major player is a risk, I believe in midstream, that’s not the case.

After all, Occidental needs midstream assets to support its operations. It cannot easily switch to a competitor, as it is “forced” to rely on existing infrastructure.

Even if it wanted to, OXY couldn’t efficiently switch to a competitor. The company is a big enough energy producer that there wouldn’t be any one competitor to WES with enough capacity to absorb all of its business.

As you would expect from a midstream company, WES’ revenue stream is also mostly insulated from commodity-price volatility. This is because 95% of natural gas volume and all crude oil/produced-water volumes fell into the fee-based category contracts as of December 31, 2023.

WES Q1 2024 Earnings Press Release

On May 8, WES kicked off the first quarter with a solid start to 2024. The company’s revenue climbed 20.9% year-over-year to $887.7 million during the quarter. That was $24.6 million better than Seeking Alpha’s analyst consensus for the quarter.

What was behind these superb results to start the year? The answer is a growth in demand for the company’s midstream services.

WES’s natural gas throughput surged 21% higher over the year-ago period to 4,990 million cubic feet per day in the first quarter. This was attributable to higher volumes at the Powder River Basin complex due to the acquisition of Meritage which closed last October for $885 million. Higher volumes at the West Texas and DJ Basin complexes from higher production in the area also played a role.

The company’s crude oil and NGLs throughput decreased by 8% year-over-year to 565 thousand barrels per day during the first quarter. That was mostly the result of divestitures of Whitehorn LLC, Mont Belvieu JV, Saddlehorn, and Panola. This was partially countered by greater volume at the Thunder Creek NGL pipeline acquired as part of the Meritage acquisition. Higher volumes at the DBM and DJ Basin oil systems stemming from increased areas production also somewhat offset divestitures.

WES’s produced-water throughput rose by 18% over the year-ago period to 1,126 thousand barrels per day for the first quarter. That was entirely driven by higher production.

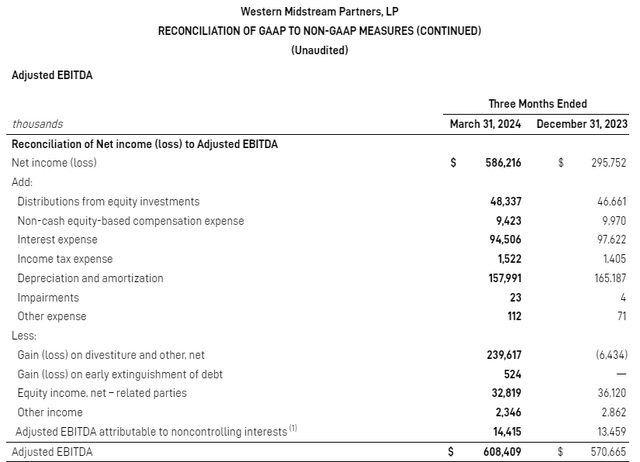

Thanks to these healthy operating results, the partnership’s adjusted EBITDA grew by 6.6% year-over-year to a record of $608.4 million in the first quarter.

WES Q1 2024 Earnings Presentation

Moving forward, the outlook for WES is quite bright. This is because, in April, the partnership brought its Mentone Train III project into service.

According to President and CEO Michael Ure’s opening remarks during the Q1 2024 Earnings Call, this was the first major construction project WES completed as a stand-alone enterprise. The partnership anticipates that this project will boost its natural gas processing capacity by around 18% in the Delaware Basin.

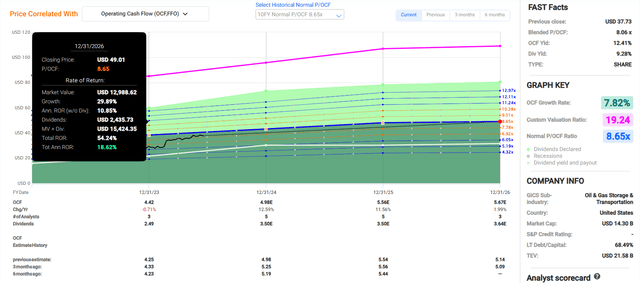

That is mostly what is guiding the FAST Graphs analyst consensus (among five analysts) that operating cash flow per unit will rise by 12.6% in 2024 to $4.98. Growing capacity and a full year of Mentone Train III operations are expected to result in an additional 11.6% growth in operating cash flow per unit to $5.56 for 2025 (among five analysts). Finally, a 2% growth in operating cash flow per unit to $5.67 is currently expected for 2026.

The other catalyst that is behind these growth estimates is the ongoing North Loving cryogenic processing plant. The company projects that 80%+ of its $775 million midpoint capital expenditures for 2024 ($700 million to $850 million) will be dedicated to the construction of this plant.

WES thinks that the plant remains on track to come online in Q1 2025. So, just as much of the initial Mentone Train III boost dissipates, the partnership will then have the North Loving plant as a tailwind.

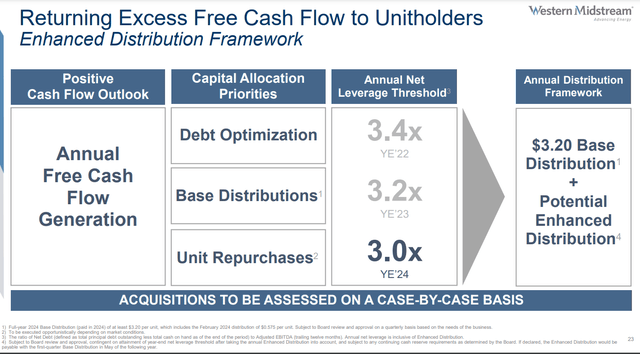

On the balance sheet front, WES is also doing well. The company’s trailing twelve month net leverage ratio was 3.3x in Q1 2024. Now that Mentone Train III is online, the uptick in adjusted EBITDA should help WES reach its targeted net leverage ratio of 3x by the end of this year. Such a leverage ratio comfortably supports the company’s BBB- credit rating from S&P on a stable outlook (unless otherwise sourced or hyperlinked, all details in this subhead were according to WES’ Q1 2024 Earnings Press Release, WES’ 10-K Filing, WES’ Q1 2024 10-Q Filing, and WES’ Q1 2024 Earnings Presentation).

Units Could Be Worth $45 Each

FAST Graphs, FactSet

If WES’s respectable operating fundamentals weren’t enough, units also look to be on sale right now.

WES’s current-year P/OCF is 7.7. That is moderately below the 10-year normal P/OCF of 8.7 per FAST Graphs. I believe that the valuation headwind of a higher interest rate environment (versus the past) in the years ahead is offset by WES’s improving balance sheet. This is why I believe that an eventual reversion to the 10-year normal P/OCF is a reasonable expectation.

The calendar year 2024 will be 48% complete after this week concludes. That means another 52% of 2024 and 48% of 2025 is still to come in the next 12 months. This is how I’m weighing the FAST Graphs 2024 and 2025 analyst consensus for OCF per unit. That gives me a 12-month forward OCF per unit input of $5.26.

Applying a valuation multiple of 8.7, I arrive at a fair value just above $45 a share. Relative to the current $38 share price (as of June 19, 2024), this would be a 16% discount to fair value. If WES matches the growth consensus and reverts to my fair value multiple, it could generate 54% cumulative total returns by the end of 2026.

The Fundamentals Support Future Distribution Growth

WES’s 9.3% forward distribution yield is leaps and bounds greater than the 4% forward yield of the energy sector. That is enough to earn an A on forward dividend yield from Seeking Alpha’s Quant System.

WES’ generous starting yield alone is enough to catch my attention. Yet, the appeal doesn’t end there, either. The distribution looks to be rather sustainable as well.

That’s because free cash flow came in at $225 million in the first quarter. Against the $223.4 million in distributions paid to partners, WES had $1.5 million in leftover free cash flow after distributions (and capital expenditures). In other words, the distribution was completely covered by free cash flow.

The partnership expects to generate $1.15 billion in midpoint free cash flow in 2024 ($1.05 billion to $1.25 billion). Additionally, WES is confident that it will come in at the high end of this guidance. Accounting for the ~$340 million in quarterly distributions the company is slated to pay in Q2-Q4, total distributions paid in 2024 will also be ~$1.25 billion (per WES’ Q1 2024 Earnings Press Release and WES’ Q1 2024 Earnings Presentation).

WES’ complete coverage of both capex and distributions should lead to distribution growth in line with business growth in the years ahead. Thus, I think at least low-single-digit annual distribution growth is a realistic expectation. Couple that with a nearly double-digit yield and this makes WES intriguing in my opinion.

Risks To Consider

WES is a quality MLP. However, no investment is right for everyone. WES is no exception.

As I alluded to earlier, OXY is WES’s largest customer. The risk of OXY switching to other midstream providers is minimal.

However, WES still faces counterparty risk. If OXY ran into financial difficulties, that could become a problem for the partnership as well. Even if that doesn’t happen, a sudden shift in OXY’s drilling activity could also hurt the company. The realization of either of those events could prompt a distribution cut from WES. That could materially harm the performance of the underlying stock as well.

If drastic enough, the fallout from such an event could include a downgrade in WES’s credit ratings. That could raise its cost of capital and damage its future growth prospects.

Another risk to WES is the regulatory climate. If the company can’t bring projects into service on budget and on time, that could also diminish its growth potential.

Summary: An Interesting Combination Of High-Yield And Value

WES is a business that looks to be doing well. Operationally, its biggest project yet was just brought into service in April. The company’s timeline to bring another major project into service early next year is holding up. These events should also bring leverage down to a very viable level in the long run.

Finally, units could be priced at a valuation sufficient to produce 50%+ cumulative total returns in the next two and a half years. This is why I’m beginning coverage with a buy rating for WES now.

Read the full article here