Intro

Westrock Coffee Company (NASDAQ:WEST) operates in the consumer defensive sector where the company provides coffee, tea, and extract solutions to a range of associated industries. The company focuses on an array of packaging solutions as well as digital traceability which focuses on delivery services on the back end. The company was founded in 2009 but went public just over 12 months ago.

If we pull up a chart of Westrock’s technical chart since it has gone public, we can see there is not much to like here. The stock spiked past $14 a share in December of last year but since then has been printing repeated lower lows and lower highs. In fact, Westrock’s share price now finds itself trading at approximately $8.90 a share which is well below the company’s IPO price of $10 a share.

Westrock Technical Chart (StockCharts.com)

The reason for the downturn is pretty self-explanatory. Top-line sales have struggled to gain traction in terms of growth and the company continues to report negative earnings (-$26.8 million in Q2 this year). Whereas the beverage solutions segment did grow its sales by 11% in the quarter, the smaller-sized ‘Sustainable Sourcing and Traceability’ segment witnessed a significant drop in sales (33%) and reported negative EBITDA consequently. Suffice it to say, that present trends point to more volatility in WEST over the near term which is why we are assigning a ‘Sell’ rating on the stock at this point in time.

Hope Springs Eternal With Conway Expansion

The investment case here on the long side is the significant spike in growth that is expected of Westrock over the next 5 to 10 years. We state this because the new Conway facilities are expected to be a game-changer for the company in terms of being able to meet demand at scale.

Why do we state this? Well, due to red-hot demand, Westrock will now have two 500,000-square-foot facilities instead of the single facility which was earmarked on day one. Modern manufacturing equipment will facilitate the production & packaging of various coffees, teas & juice-related products at scale. Furthermore, the benefit here from Westrock’s standpoint is that it has been selling out its production lines well before products have come on stream. Suffice it to say, that expansion in Conway would not be happening if the demand for Westrock’s products and services was not there. The CEO (due to the expansion at Conway) is now projecting $125 to $150 million in annual EBITDA once all production lines are up and running. Suffice it to say, given where Westrock is today (EBITDA growth is negative 8%+ over a trailing twelve-month basis), one would think that this expected growth would do wonders for the share price over the long haul. Not so fast.

Cost Of The Company’s Growth From A Shareholder’s Standpoint

Firstly, we do not doubt that Westrock will report a significant improvement in profitability over the next five to seven years, but the real question here is at what cost. Look at where the company stands at present. In recent months, for example, Westrock has been reporting negative EPS revisions compared which means cash-flow generation will most likely remain subdued in upcoming quarters. The CEO spoke on the recent Q2 earnings call about how capital has continued to be plowed into the Conway expansion to the detriment of reporting higher earnings in the near term. This is all well and good for the future of Westrock but what about the fate of the existing shareholder? How will his or her investment fare out over the next 5 years or so?

Operating cash flow of -$45.3 million over the past four quarters & $56.6 million in fiscal 2022 continues to pressure the financials. Furthermore, the number of shares outstanding now comes in at almost 90 million shares. To put this number in perspective, over the past 9 months alone, a long investor in WEST has seen his stake in the company (in terms of ownership) almost half in value. Therefore, the slower it takes a fully operational Conway to get up and running concerning achieving those lofty EBITDA targets, the more risk the current WEST long investor has.

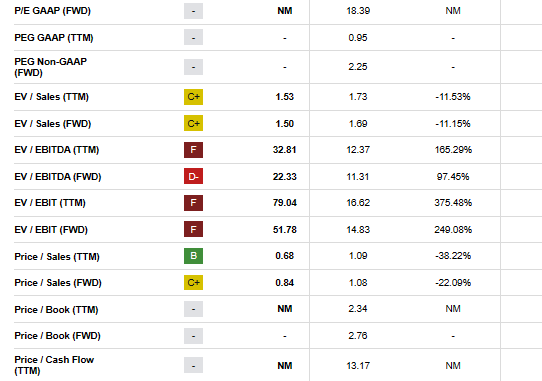

The crux of the issue here is that valuation matters even for companies that are expected to report significant earnings growth going forward. As we see below, the only encouraging valuation multiple that Westrock has going for it at present is its sales multiple (trailing sales multiple of 0.69). However, this multiple has to be taken with a pinch of salt given the company’s reported negative equity, negative GAAP earnings, and negative cash-flow positions at present.

WEST valuation metrics (Seeking Alpha)

Conclusion

Therefore, to sum up, there is no doubt that Westrock’s financials in terms of sales and earnings will be in a much brighter position come three to five years. The ‘cost’ of this growth though is what present long investors should cue into. Despite successful equity raises and capital from outside investors, Westrock’s financials look like they will remain under pressure for the time being which will consequently affect the share price. We look forward to continued coverage.

Read the full article here