Webster Financial Corporation (NYSE:WBS) is a Stamford, Connecticut-based regional commercial bank with operations across New England and parts of New York.

Webster Q2’23 Presentation

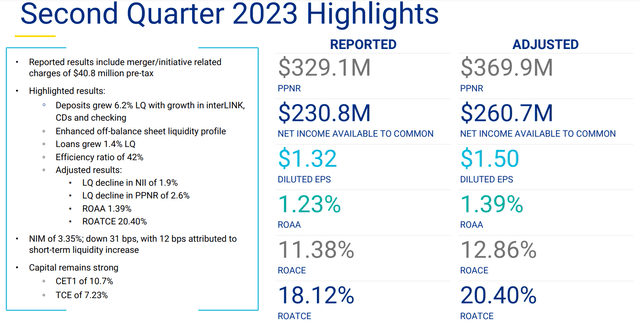

Through these activities, Webster has seen Q2’23 revenues of $1.02bn, a 64.91% increase, alongside a net income of $232.73mn – a 28.87% increase – and a free cash flow of $240.88mn- a 42.47% decline driven by poor financial cash flow results.

TradingView TradingView TradingView

Introduction

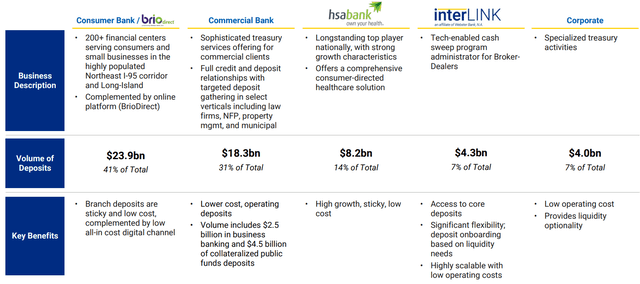

Webster’s business remains significantly more segmented than that of peer commercial banks; the company operates through five principal verticals including its consumer bank- including the ‘briodirect’ brand, the company’s commercial bank, ‘hsabank’ which services healthcare financial solutions, ‘interLINK’ which provides cash sweep programs- essentially the use of excess cash to pay down debt and converting the cash into debt security, and Corporate, treasury activities.

Webster Q2’23 Presentation

By operating across the commercial banking landscape, Webster positions itself to better access capital and be resilient in the face of macro headwinds, seeing real increases in revenues and net income in the turbulent environment of the past year.

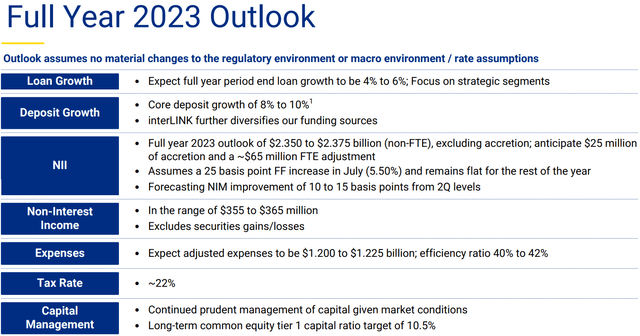

Coming to the end of the year, Webster visualizes significant full-year loan growth, core deposit growth nearing the double digits, rising net interest income, a well-managed expense base, and risk-averse capital management strategies.

Webster Q2’23 Presentation

While Webster maintains a sound operational strategy, its biggest draw is how underpriced it is; investors remain fearful of both regional banks- due to recent failures- and commercial banking- with high interest rates increasing capital costs for SMEs and larger corporations alike- but Webster manages these risks much better than the market has priced and thus is a ‘strong buy’.

Valuation & Financials

Trailing Company Performance

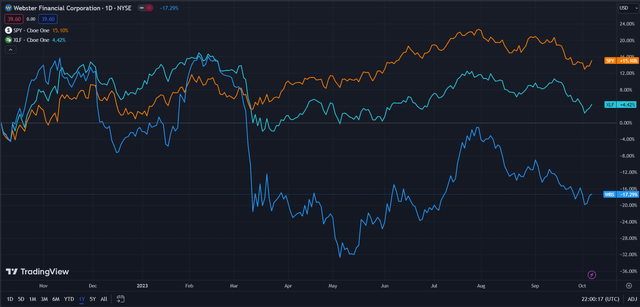

In the TTM period, Webster’s stock- down 17.29%- has experienced poorer price action to both Financial Select Sector SPDR Fund (XLF) – up 4.42%, representing the rest of the financial services industry, and the broader market, as represented by the S&P 500 (SPY) – up 15.10% in the same time period.

Webster (Dark Blue) vs Industry & Market (TradingView)

As aforementioned, Webster’s weaker price performance is likely derivative of market fears surrounding its presence both as a regional bank and commercial bank.

And since the financial services industry is exposed to a wider range of risks and benefits than Webster and XLF is principally composed of larger, more capitalized banks, Webster has underperformed XLF as well.

Comparable Companies

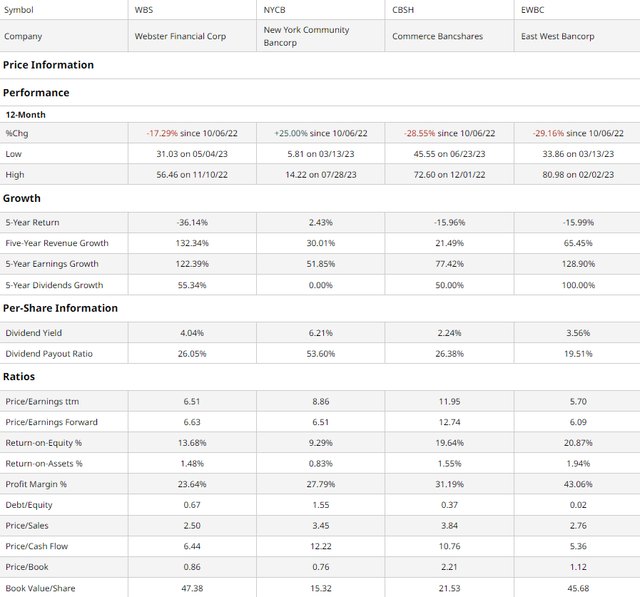

The regional commercial banking industry, by its very definition, is a geographically segmented sector with services specialized to the needs of the given region. As such, there are few publicly listed direct competitors to Webster and I sought to compare it to similarly sized regional banks. This group includes Hicksville-based New York Community Bancorp (NYCB), which operates across New York, the Midwest and is expanding into Florida and Arizona, the Kansas City, Missouri-based Commerce Bancshares (CBSH), and the Pasadena, California-based Chinese-America servicer, East West Bancorp (EWBC).

barchart.com

As demonstrated above, besides New York Community Bancorp, all three of Webster’s peers have experienced negative share price action, likely attributed to larger market headwinds. Despite, this, due to Webster’s superior multiples-based value and growth capabilities, I believe Webster has room for reversion.

For instance, Webster maintains the second-best trailing and joint-second-best forward P/E ratios, alongside the lowest P/S, second-lowest P/CF, and second-lowest P/B, demonstrating value across all three financial statements.

Additionally, the company sustains the greatest revenue growth and second-highest earnings growth among peers. And with the highest book value per share and a reasonable debt/equity, Webster remains a safe asset.

Moreover, Webster provides the second-highest dividend with a very conservative payout ratio that signals stability and long-run income growth for investors.

Valuation

According to my discounted cash flow analysis, at its base case, the net present value of Webster is $48.10, meaning, at its current price of $38.99, the stock is undervalued by 19%.

My model, calculated over 5 years without built-in perpetual growth, assumes a discount rate of 10%, reflecting the rising cost of capital and a high level of implied volatility for the stock. Additionally, while the historic 5Y average revenue growth rate of Webster was 24.72%- skewed upwards by the 2021-22 growth of 114.90%- I projected a forward 5Y revenue growth rate of 10%, driven by the company’s fast-growing subsidiary-driven strategy and sustained higher interest rates.

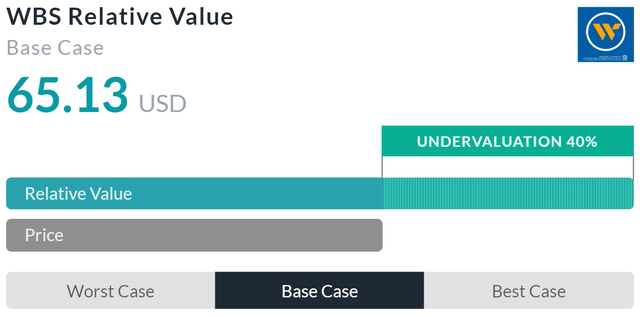

Alpha Spread

Alpha Spread’s multiples-based relative valuation tool corroborates my thesis on undervaluation, estimating a relative value of $65.13 meaning the company is currently undervalued by 40%.

Thus, taking an average of my net present value and Alpha Spread’s relative value, the fair value of Webster is $56.62 – a 29.5% undervaluation.

Webster’s Balance Sheet Remains Strong But is Discounted by the Market

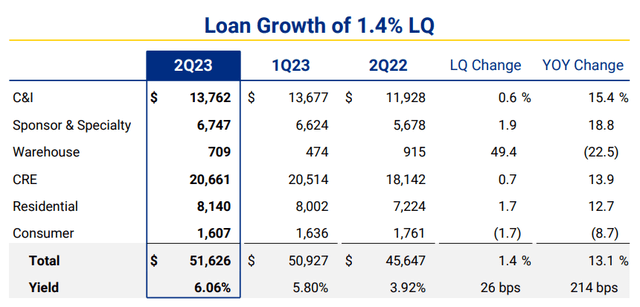

A key component of my thesis is that Webster’s risk management makes its financial position superior to that of peers and thus should not be priced like other regional commercial banks. For example, Webster’s loan portfolio is highly diversified; Commerce and Industry lending- general loans used for purposes from working capital to capex- makes up a growing part of the company’s portfolio, while commercial real estate, residential, and sponsor and specialty lending make up other significant parts. While most fixed income operates on similar convexity dynamics to interest rates, the portfolio diversity here makes it so that downturns in a particular sector will not significantly increase insolvency risk for Webster.

Webster Q2’23 Presentation

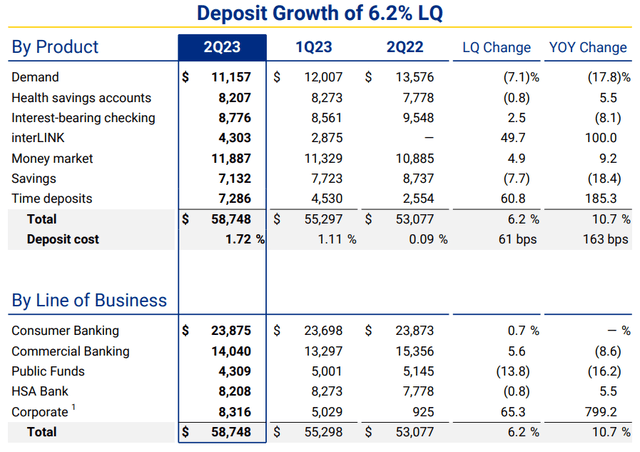

Yet, an even larger aspect of Webster’s ability to sidestep the risks that have left other regional banks vulnerable is the range and diversity of deposit origination, with deposit sizes larger than loans- this in turn supports solvency and with high yields, still allows the company to turn a decent profit. And unlike loans, many of these deposit sources operate differently than one another in a given macro environment; HSAs tend to be more inelastic than general savings, while interLINK is a fast-growing service covering for the decline across other deposit sourcing.

Webster Q2’23 Presentation

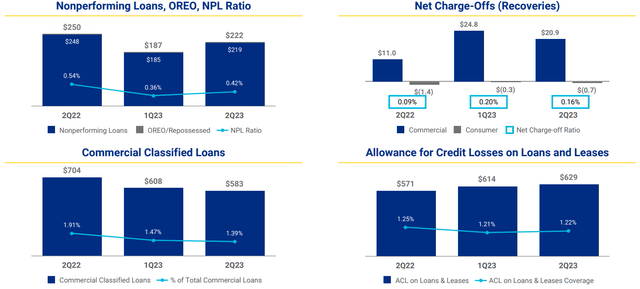

This has culminated in Webster’s overall bank ratios being significantly superior to commercial bank averages; an NPL ratio of only 0.42% means that only that percentage of loans are in default, with the NPL to total asset ratio averaging around 4% for banks. Furthermore, with a net charge-off of only 0.16%, while higher than the previous year due to higher rates, Webster is much less likely to have unrecoverable loans than the rest of the industry, which has a seasonally adjusted net charge-off ratio of 0.52 across all leases and loans.

Webster Q2’23 Presentation

Wall Street Consensus

Analysts echo my positive view of Webster, estimating an average 1Y price target of $50.38, a 27.23% increase.

TradingView

Even at the minimum projected price target of $42.00, analysts see a price increase of 6.06%, even larger net when considering Webster’s 4.04% dividend.

Risks & Challenges

Counterparty Risk is Particularly Prevalent in the Current Macro Environment

As demonstrated by the failures of First Republic Bank and Silicon Valley Bank earlier in the year, a higher interest rate environment is conducive to greater corporate failures and thus delinquency and default risk. This is particularly acute for commercial banks, which are less protected than equivalent retail banks from consumer default. Although Webster is better positioned to deal with such risks than competitors, as outlined previously, liquidity and lending demand are still determined by counterparties.

Increased Compliance Costs & Risks

Again pertaining to the failure of other medium-sized banks and the near collapse of banks such as PacWest (PACW), Webster, as a regionally-oriented bank, is subject to potential regulatory shifts from state or federal legislators or banking regulators. This may reduce Webster’s operational flexibility, constrain growth, and ultimately reduce long run profits and ability to return capital to shareholders.

Conclusion

Going forward, Webster remains a well-capitalized, safe company sorely underpriced by the market and due for a reversion in the coming months or year.

Read the full article here