Introduction

Whirlpool (NYSE:WHR) has been in the rumor news recently that it may be acquired by another company. I wanted to revisit the company as it has come down to my fair value target set back in January, give my thoughts on the company’s performance over the year, and whether I like the company now. Nothing major changed that would keep me cautious going forward, and I think the company is a buy at the current levels, even after the rumor spike in share price recently. If you believe the company can turn around, as I do, even if the acquisition remains just a rumor, it is a good time to start a position and wait it out.

Briefly on Financial Performance

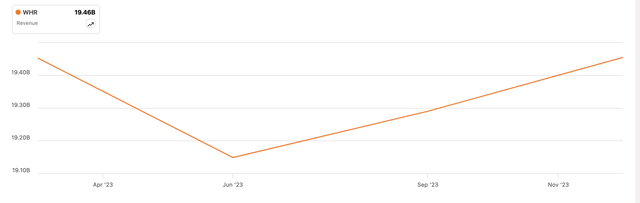

Looking at the company’s revenues for the year, we can see a slight rebound from the bottom at the end of June ’23. Sales started to pick back up after the first half seeing sales decline upwards of 6% y/y. What is the cause of such underperformance? The management is putting the blame on the “still unfavorable housing cycle in 2023”, which is true. The mortgage rate increase was very sudden, which put a damper on existing home sales, in turn affecting the sales of the company’s appliances. With the mortgage rates still hovering at the highest levels since 2008, I have no problem believing that people are holding off making such big money decisions right now.

Seeking Alpha

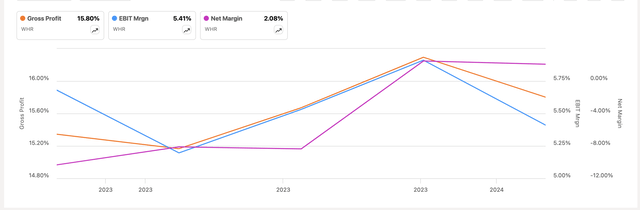

As for margins, we can see a similar pattern as with the rebound in revenues since Jun ’23. These have seen an improvement across the board, however, as these are TTM margin numbers, they don’t show the impact on the bottom line that the divestiture had, which was a loss of $222m. Nevertheless, with the EMEA closure’s finalization, I expect the bottom line to improve. The question is, how much? I will discuss this in a later section.

Seeking Alpha

Now, let’s look at the company’s financial position as it currently stands. As of Q1 ’24, which was filed on April 25th ’24, WHR had around $1.2B in cash and equivalents, against $6.6B on long-term debt, which could put off a lot of investors. The debt outstanding is more than the company’s current market cap, and many investors are cautious of companies that overindulge in leverage. Is it worrisome, though? At the end of ’23, the company’s EBIT covered the annual interest expense on debt a little over 3 times. By this statistic, many analysts would consider that sufficient, however, I would like to see the company being able to cover interest expenses with operating income at least 5x. This way, the company’s operations have some room for downturns, like we are in currently. WHR operations have been underperforming, to say the least. So far in Q1, the company’s EBIT came out negative, which means it was not able to cover its interest expense on debt, but given the company’s healthy cash situation, it is not a problem in my opinion. Furthermore, I don’t like judging a company’s liquidity based on one quarter of the year, so I would like to see how well the other quarters fare when divestitures are not included any longer.

Overall, I can see a company has been underperforming for a while, but given the current macroeconomic backdrop, I think it could have performed much worse. The company’s cash position is decent, although I would like to see it reduce that debt pile, which should attract more investors if the prospects turn around for the company in the future. Most of the company’s debt is fixed, except around $2B, which is variable and currently sitting at around 6% interest. Interest rates may stay higher for longer, but may not rise anymore, so I think the worst is behind.

Comments on the Outlook

Operations Should Improve

With all the divestitures the company has been doing recently, there is certainly a lot of room for margin expansion if everything is executed well. Cutting out the underperforming businesses should yield better margins overall and an improvement in the company’s cash flow. A more focused, streamlined business is always a good decision, although, in the short run, these decisions may impact the company’s performance as we saw in the last couple of years.

Another big factor that will continue to affect the company’s profitability is sticky inflation, which continues to affect input and transportation costs. However, inflation has come considerably down since its peak; therefore, I would expect this environment to improve in the long term, unless something unforeseen happens, and we are right back in that high inflation environment. Despite such an environment, the company managed to improve its cost structure in Q1 ’24, and if everything goes well going forward, I am expecting further cost improvements, but that remains to be seen. The management mentioned that they expect the company’s “manufacturing and supply chain cost actions to continue to ramp up throughout the year.”

I would also like to see how the company goes about its small domestic appliances segment, which is its KitchenAid brand, as this segment seems to have performed rather well overall, with high margins; therefore, I would like to see some focus put on it, which should drive up its profitability. The segment only accounts for about 4% of total sales, so the improvements won’t be very visible, but I would like to see this segment expand.

In terms of revenues, the company is still operating in an environment that is very unfavorable for WHR and its customers. The North American operations have been soft due to high interest rates, the company looked at value-creating promotions which meant a lower top line. However, the company expects to increase the promotional prices across the board by around 5%, which should improve its top-line performance, all things equal.

In terms of housing, I don’t expect things to improve within the next year. However, these sorts of sectors are very cyclical and never stay negative, so I agree with the management’s medium-to-long-term outlook that we will see an improvement eventually. Mortgage rates will have to come down once again, but I don’t expect them to be below 3% or 4% in the long run as that I believe was too low due to the pandemic panic.

Acquisition Rumors

There has been a lot of activity last week regarding a potential acquisition of WHR by Bosch. On such rumors, the company’s share price spiked over 12%. Nothing is concrete yet, and both parties are not going to respond to such stories that may not be true, and the source, who doesn’t want to be named, is not certain that the deal would be made. So, we have here a “buy the rumor, sell the news” situation.

This rumor can benefit both companies. For investors of WHR, this means a company most likely be bought out at a premium to its current share price, and even now, if someone wants to get out, a one-day pop of 12% in share price may be good enough if they expect nothing better. If the deal does happen, what kind of premium is the company going to offer is all speculation, but I wouldn’t think it would be below $120 a share. For Bosch, it is a good time to shop around, considering how beaten down WHR is. By acquiring WHR, Bosch would strengthen its position in the global appliance market, especially in the US. Furthermore, they will also get some decent exposure in markets like India, where WHR still owns about half of its operations there after the sale of a 24% stake.

As I said, these are all rumors and nothing has been penned officially; therefore, it is worth looking at the company as it stands currently without the prospect of it being acquired, and I think there is a lot of potential for a turnaround over the next couple of years.

If the deal is not on the table, the company has been paying dividends for almost 70 years now, and I don’t expect it to be cut any time soon. This gives a decent cushion for current investors of the company who still believe there will be a turnaround. The dividend yield is around 7% now, so it is pretty decent now that the share price tumbled 30% in the last year. I don’t think the company would risk its status of consistently paying dividends, but if the future continues to be bleak and cash flows do not improve as expected, I wouldn’t be surprised if we do see a cut at some point. AT&T (T) used to be a dividend aristocrat, but after a few bad acquisitions and a mountain of debt, it decided to cut it in half and focus on repaying its debt. WHR’s debt levels are nowhere near as high as T’s, and if the economy recovers, the dividend should be safe as the company’s operations improve.

Valuation

So, it has been exactly 6 months since I did a valuation of the company and some things changed operationally. The cost-cutting measures seem to be taking shape and saving the company some money already, and I expect further improvements, while revenue growth is not much better in my opinion. Let’s go through some assumptions.

For revenues, as I said, I don’t think we will see much growth here; therefore, I went with around 1% growth for the next decade.

Author

For margins, I decided to improve these very slightly over the next decade because I would like to keep it conservative. Over the next decade, gross margins will see only 70bps improvement, which I think is manageable with the cost-cutting measures it has already in place.

Author

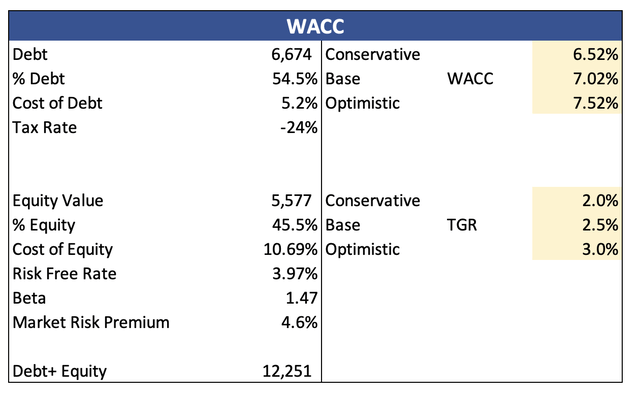

For the DCF, I went with the company’s WACC of around 7%, and a 2.5% terminal growth rate because I would like to see the company at least match the growth of the US long-term inflation goal.

Author

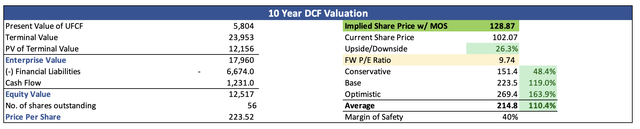

I am also adding another discount to the final intrinsic value calculation to be even more conservative and give me some more room for error in my calculations. I chose quite a large discount just like last time of 40% due to uncertainties of acquisition, high debt, and further economic downturn. With that said, WHR’s conservative intrinsic value is around $129 a share, which means it is still trading at a discount to its fair value.

Author

Should you add WHR to your portfolio?

I went through a DCF model in my previous article on the company, and I came up with a fair value of around $100 a share. This price was triggered at the end of April, and it continued to go down further. Unfortunately, it completely skipped my mind over the next couple of months and I missed out on getting in on the company in the mid-$80s. Now, with the rumor of the acquisition it has gotten much more expensive in just one day; however, I believe anything around this price is a good deal even if the company is not going to be acquired; therefore, I am upgrading the company to a buy. Do heed caution, though. The acquisition may not come through and we most likely see the share price plummet back to where it was, so if you do believe in the company’s turnaround, I recommend only opening a small position right now, to at least capture some of that hope of acquisition. Keep it small for now in case it doesn’t go through and add when it drops once again, as I do believe this is a good price to dip your toes in.

If you managed to get in when the price was in the mid-$80s, and still believe in the long-term bullish outlook, you got nothing to worry about. Enjoy your dividend and see how the company’s efforts of a turnaround develop over the next while. That is what I am going to do.

Read the full article here