Dear Partners,

While individual returns may differ based on their inception dates, consolidated performance of all accounts for the period ending June 30, 2024 is as follows:

|

Q2 2024 |

1H 2024 |

2023 |

2022 |

ITD* |

|

|

White Falcon (net of fees) |

-5.9% |

2.4% |

36.0% |

-9.26% |

24.4% |

|

S&P 500 TR (CAD) |

5.3% |

18.8% |

23.2% |

-12.6% |

32.1% |

|

MSCI All Country TR (CAD) |

3.7% |

14.6% |

18.5% |

-11.9% |

21.5% |

|

S&P TSX TR |

-0.5% |

6.1% |

11.8% |

-5.8% |

11.2% |

|

*Inception date is Nov 8, 2021 |

This was a difficult quarter. The negative performance of Endava (DAVA), EPAM and Converge (OTCQX:CTSDF) could not be offset by strength in Amazon.com (AMZN), Nu Holdings (NU) and precious metal royalty companies. The portfolio was affected by middling earnings and guidance downgrades from our IT services and software positions as corporates prioritize Artificial Intelligence (‘AI’) related IT spending. The market itself had an excellent first half but we must point out that a lot of these gains were led by a few select stocks with the equal weighted S&P 500 (SP500, SPX) up about 5.1% in the first half of the year. Towards the conclusion of this letter, we elaborate on why we perceive the current environment to be similar to the 1970s rather than the late 1990s.

We have always emphasized that our performance will always look very different when compared to the popular indices as our portfolio looks very different when compared to the popular indices. These differences are especially enhanced over shorter periods of time. There are numerous factors – sentiment, narratives, flows, factor rotations, among others – that affect the price of a stock over the very short term. However, in the long term, fundamentals rule. We believe we own some wonderful businesses and have full confidence in the portfolio. In fact, we believe that this temporary dip enhances the look-forward Internal Rate of Return (‘IRR’) of the portfolio as it has allowed us to lower our average cost base and concentrate on our best ideas.

Investment ideas are fragile. In order to achieve market beating returns, one has to have a variant view. Most of White Falcon’s positions are in companies where:

- We believe the growth, margins, or free cash flow will exceed market expectations.

- The market undervalues the business’s quality or the management’s capital allocation skills.

- The business is temporarily out of favor, and we anticipate the stock price will recover as these issues subside. Our longer-term perspective aids in this.

- We purchase securities from distressed investors who are selling for reasons unrelated to fundamentals.

“The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values.”-Warren Buffett

When we make an investment, the situation is often complex and convoluted, otherwise, it wouldn’t offer high risk adjusted IRRs. For example, there can be issues such as a poor quarterly performance, supply chain issues, or a longer than anticipated turnaround in business performance. Investors often acknowledge a business’s quality but prefer to invest after challenging quarters have passed. On the other hand, we often try to invest at the point of maximum pessimism in the stock as that is when we can buy a good quality business at a reasonable valuation. If our analysis is correct, we are likely to profit in the long term; however, we have limited control over the situation in the interim.

In a typical quarter, we often see one or two investments – like Aritzia (OTCPK:ATZAF) or Converge experiencing a drawdown. Due to our portfolio’s diversification, this drawdown does not significantly impact the portfolio’s overall performance. However, during Q2, a higher-than-usual number of portfolio companies experienced drawdowns, marking a departure from the norm. I will delve into some of the reasons below, and explain why I have confidence in our portfolio.

Our portfolio is heavily tilted towards technology companies. Technology, whether in the form of railroads, electricity, radio, motor vehicles, or the internet, has consistently had the potential to disrupt existing industries and create entirely new ones. We have learned through experience that investing becomes marginally easier, and far more profitable, when done in secularly growing and good quality businesses – as long as one pays attention to valuations.

Due to this, we have positioned ourselves in businesses such as EPAM and Endava which are IT services companies that help other corporations implement new technologies. These are good quality businesses with robust economics and are led by their founder CEOs. Currently, AI is the new technology trend and investor emphasis has been on investing in hardware to support AI capabilities. As the necessary hardware becomes more widespread, the focus will likely shift towards creating and optimizing AI applications. EPAM and Endava will benefit from this cycle as they have built a reputation for executing specialized and complicated IT projects. However, AI is still a new technology, and clients need time to identify the best use cases. This has led to a cautious “wait and see” approach from clients, which is currently suppressing demand for IT services. The timing of demand revival in the sector is uncertain and, as we have discussed before, the market hates uncertainty.

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach”-Peter Lynch

We believe the market has overreacted and EPAM and Endava are now trading at historically low multiples of depressed earnings. Eventually, corporations will need the help of EPAM and Endava in order to design, build, test, and implement AI applications. We have added to both stocks and lowered our cost basis, which we anticipate will enhance the overall internal rate of return (IRR) of the portfolio.

Case Study: Aritzia

Let’s look at Aritzia for a typical case study. We bought a position in Aritzia in 2022 and had an average cost base of around $36 per share. Our thesis was that Aritzia is a high-ROIC business offering essential clothing, driven by a capable management team with strong founder leadership. Importantly, there was predictable growth in the business as Aritzia was just starting to expand in the US and had plans to open ~10 stores in the US every year for the foreseeable future. However, in 2023, the business encountered difficulties due to over-ordering of inventory and rising expenses. The market’s dislike of uncertainty caused the stock to be punished beyond what we considered reasonable. At the bottom, our estimate was that Aritzia was trading at less than 10x our estimate of 2026E earnings.

“You’re looking for a mispriced gamble. That’s what investing is. And you have to know enough to know whether the gamble is mispriced. That’s value investing.”-Charlie Munger

We thoroughly reviewed and verified our work, including speaking with management, former employees, and competitors; and concluded that these issues will resolve themselves over time. We took advantage of the situation and added to our position in the $22-25 price range and brought our cost base down to $28 per share. The situation recently corrected itself when Aritzia reported a good quarter and the stock recently closed at $47.50 per share.

From our perspective, market volatility is a feature, not a bug – Aritzia experienced more than a 50% decline followed by more than a 100% increase – all within just two years!

To be clear, it is not always appropriate to add to a declining stock. This should be done selectively and only when the risk-reward is favorable. In the last two quarters, we sold our positions in Warner Bros Discovery (WBD) and Fortrea (FTRE) – both at a small loss. While both stocks remain inexpensive and could potentially recover, our analysis has reduced our confidence in their prospects. This concern was exacerbated by the high levels of leverage present in both companies.

The top 5 positions in the portfolio are: Precious Metals royalty basket, Endava, Amazon.com, Nu Holdings, and Rentokil Initial Plc. We have been communicating our strategy of shifting the portfolio increasingly towards small and mid-cap stocks where we have found valuations to be much more reasonable. In the last quarter, we noticed that several of these stocks did not gain or sustain their gains despite improvements in their fundamentals. However, following the quarter’s end, we witnessed early signs of optimism as lower inflation readings and expectations of rate cuts rejuvenated small and mid-cap positions in the portfolio – including EPAM and Endava.

It is our job to position the portfolio for the future – sometimes the future is just a little bit delayed!

Rentokil Initial Plc (RTO) is a global business services company specializing in pest control and hygiene services. These revenue streams are relatively stable and resilient, even during economic downturns. Rentokil’s moat comes from its scale, network density, technology and established brand name. Rentokil typically trades for ~25x earnings but is currently available for 19x 2024E earnings and 12x our estimate of 2026E earnings.

As we have described above, something must be going ‘wrong’ if a good business is available for a low multiple. Rentokil acquired Terminix, the largest pest services provider in the US, and has encountered some integration challenges. Our due diligence on Rentokil has led us to believe that they can successfully integrate Terminix and meet their targets. Importantly, the valuation discounts many of these issues, creating a ‘heads I win, tails I do not lose much’ scenario. In the appendix to this letter, we re-produce an article that we wrote for the Globe &Mail on Rentokil. While it’s not our typical long-form report, we hope you’ll still find it enjoyable.

Overall market comments

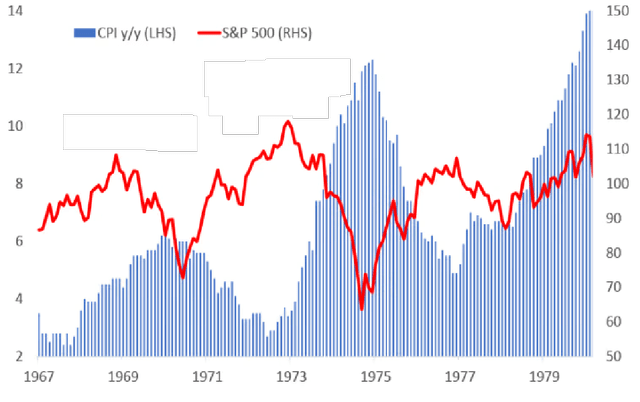

A few of you have inquired about the general market environment. While many commentators draw comparisons between the current surge in AI stocks, particularly Nvidia, and the late 1990s internet boom, we find the nifty-fifty craze of the early 1970s to be a more fitting analogy.

On a macro level, fiscally induced inflation, populist policies, increasing regulation, geopolitical risks, and increasing negotiating power of labor are some of the common themes between the two time periods. On a micro level, similar to the 1970’s, a few select stocks are now considered ‘one decision stocks’ and investors of all stripes are having a hard time coming up with a bear case.

The above chart from Marketwatch shows that, in the 1970s, after the initial wave of inflation, there was a subsequent and more pronounced surge in inflation. This spike in inflation triggered the bear market of 1974-75, which resulted in the S&P 500 seeing no positive returns for almost 10 years.

Two additional points further reinforce and support this hypothesis:

First, the total return from the market is typically ~10% per year on average. This is because, in the long term, stock prices generally move in line with earnings growth, which is driven by nominal GDP and profit margins (which are already at the highest levels ever!). Over the past 15 years, since the Global Financial Crisis, S&P 500 has increased by a compound annual growth rate (‘CAGR’) of 15.03%. To return to the historical average of 10%, forward returns will need to be significantly lower – perhaps somewhere between 1-5% – over the next 10 years.

Second, Warren Buffett is the only investor we know who actively invested capital during the 1970s. Observing his actions today, we see that he has been purchasing oil and gas companies like Occidental Petroleum and Chevron, as well as gaining exposure to commodities through holdings in Japanese trading companies. Looking back at the 1970s, the best-performing sectors were REITs, oil and gas companies, and various commodities including gold and silver – any and all real assets. Warren’s recent purchases reflect a belief that these types of investments will again prove profitable just like they did in the 1970s.

This will not be an easy environment for making money, and those crowding into US passive ETFs are likely to see minimal real returns on their investments. While we do own some of these popular stocks, we believe that, as active managers, we can be much more agile in our approach compared to a passive index. Unlike our contrarian approach, indexes act like momentum investors, buying more of what is going up. If these mega-cap stocks begin to underperform, they will likely drag the index down with them for an extended period, as reducing their weight in the indices will take time.

Traditional active managers might outperform, but charging a fee of 1%+ on assets under management (‘AUM’) for a potential 1-5% annual return means that the fee represents 20% to 100% of potential returns, significantly reducing the net gains realized by investors.

White Falcon’s structure and alignment offer numerous advantages in such an environment.

In closing, I want to express my enduring gratitude to each and every partner of White Falcon. I’ll be in Vancouver from July 29th to August 9th and in Calgary from August 12th to 24th. I’d love to meet up while I’m there, so please reach out to arrange a time.

Also, please feel free to get in touch with me at any time for any questions or feedback you may have.

With gratitude,

Balkar Sivia, CFA

Founder and Portfolio Manager, White Falcon Capital Management Ltd.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here