Introduction

I’m starting this article by admitting I was wrong – or was I early?

While it depends on one’s timeframe, being early is often the same as being wrong.

On November 11, 2022, I wrote an article titled FMC Confirms The Agriculture Bull Case. In that article, I discussed favorable agriculture fundamentals that were expected to benefit the FMC Corporation (NYSE:FMC). While most fundamentals are still strong, the stock price has declined by roughly 45% since then, making it one of the worst performers on my radar.

The good news is that a lot of weakness has been priced in. FMC is ready to make a comeback as pricing is improving, supporting margins.

When adding the company’s successful product improvements and a potential end to inventory de-stocking, FMC gets a highly favorable risk/reward.

So, let’s get to the details!

What’s FMC?

With an $8.2 billion market cap, Philadelphia-based FMC is one of the world’s largest agriculture input players.

The company focuses on providing innovative crop protection solutions that address challenges faced by growers without compromising safety or the environment. Their portfolio includes insecticides, herbicides, fungicides, and biological technologies.

In other words, the company covers all major threats: Weeds, insects, and fungi.

FMC Corporation

FMC has strategically streamlined its portfolio over the past decade to become a tier-one leader and the fifth-largest global innovator in the agricultural chemicals market. The company believes that its strong competitive position is attributed to technology, innovation, geographic balance, and crop diversity, leading to market share growth in key regions.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

|

Brazil |

1,224 | 24.3 % | 1,621 | 27.9 % |

|

United States |

1,018 | 20.2 % | 1,289 | 22.2 % |

|

Asia |

1,255 | 24.9 % | 1,239 | 21.3 % |

|

Europe, Middle East, & Africa |

1,040 | 20.6 % | 1,040 | 17.9 % |

|

Latin America |

409 | 8.1 % | 467 | 8.1 % |

|

North America |

99 | 2.0 % | 147 | 2.5 % |

The company has a strong agricultural product pipeline with 23 new active ingredients in discovery and 11 in development, with a focus on creating new insecticides, herbicides, and fungicides with improved environmental sustainability.

What’s Going Wrong?

The second quarter saw a significant decline in sales volume across all regions, primarily due to de-stocking actions by growers in response to factors like increased interest rates affecting inventory costs, improved supply chain stability, and price reductions in certain product categories.

As a result, the global crop protection market is now expected to decrease by a high single-digit to a low double-digit percentage.

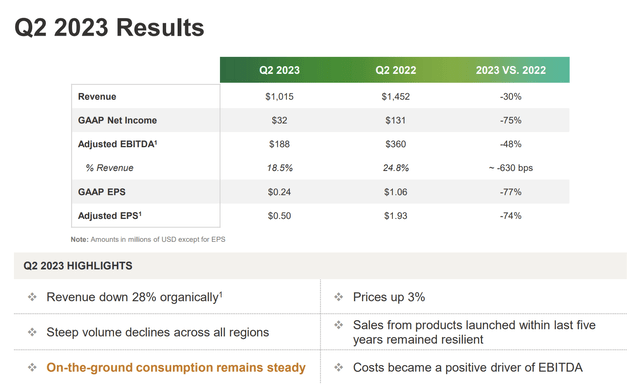

FMC experienced a 30% lower revenue compared to the prior year, with notable declines in North America, EMEA, Latin America, and Asia.

FMC Corporation

EBITDA for the quarter was $188 million, down 48% from the prior year, primarily due to the volume decline and adverse FX impact.

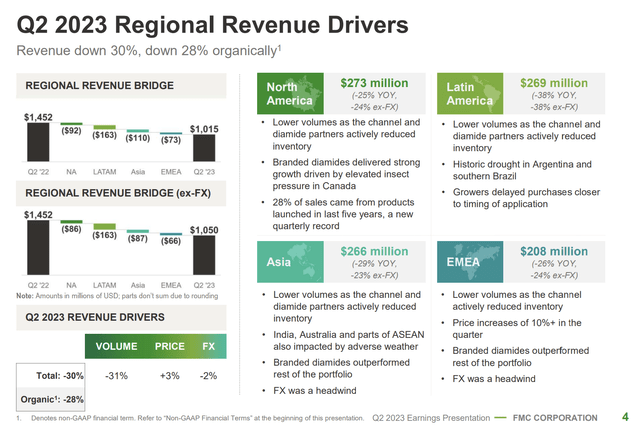

As one can expect, the decline in sales varied across regions.

- North American sales were down 25% (24% excluding FX), with new products introduced in the last five years growing by 43%.

- In EMEA, sales declined by 26% YoY (24% excluding FX) due to adverse weather and de-stocking.

- Latin America faced a 38% decline in revenue, attributed to a historic drought.

- In Asia, sales declined by 29%, with India facing volume challenges due to excess rain.

FMC Corporation

Despite the challenging market conditions, sales of newer products and branded diamides showed resilience, underlining the value of FMC’s innovative portfolio. For example, as I just mentioned, new product sales in North America saw 43% growth.

What’s Next?

During this month’s Jefferies 2023 Industrials Conference, the company also commented on inventory de-stocking issues (emphasis added):

I mean certainly, we’ve seen a significant improvement in inventories. I do think there are some differences depending on where in the value chain you are and then numerous reports from some of your peer sales side analysts as well as from some of our customers in public statements where it appears U.S. inventory retail levels are very, very low. Our viewpoint at the distributor wholesaler level, we still think it’s a bit elevated. So system-wide, where is the inventory still leveling out. But we’ve had a full growing season now that’s been exposed to this reset force.

The company also commented on 2024. While acknowledging potential headwinds, the company projects sustained growth, reiterating its historical outperformance and commitment to delivering value to shareholders.

During the Q2 2023 earnings call, the company gave us some positive comments as well.

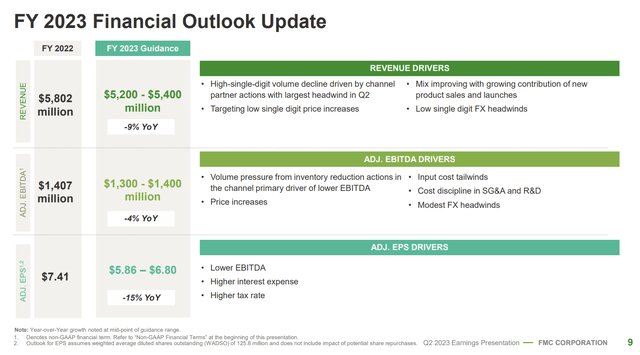

Despite the challenging first half, the company was optimistic about the second half of the year. They expected strong EBITDA margin expansion driven by input cost tailwinds, pricing adjustments, improved product mix, and disciplined operating expenses.

Projections indicated EBITDA margins increasing by approximately 270 basis points in 3Q and 460 basis points in 4Q, with a full-year 2023 forecasted increase of about 120 basis points.

Unfortunately, 2023 is expected to be materially weaker than 2022.

FOMC Corporation

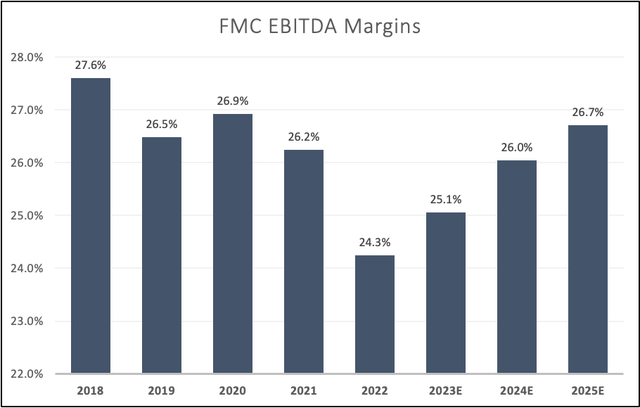

Analysts agree and see a margin recovery beyond 2024.

Leo Nelissen (Based on analyst estimates)

It also helps that FMC has a healthy balance sheet.

In the second quarter, the company issued $1.5 billion in senior unsecured notes with various maturities to retire the 2021 term loan and pay down commercial paper balances.

As a result, gross debt on June 30 was $4.7 billion, up $470 million from the previous quarter. Gross debt to trailing 12-month EBITDA was 3.8x, while the net debt-to-EBITDA ratio was 3.0x.

Next year, net debt is expected to fall to 1.9x EBITDA.

This is caused by higher EBITDA, as analysts expect 2024 to see a 10% surge in EBITDA, followed by a smaller rise in 2025.

Leo Nelissen (Based on analyst estimates)

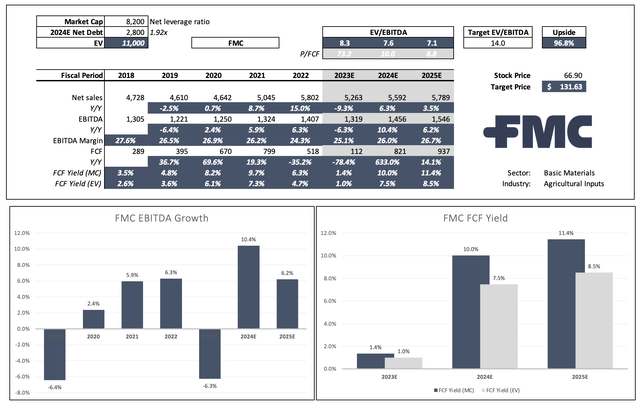

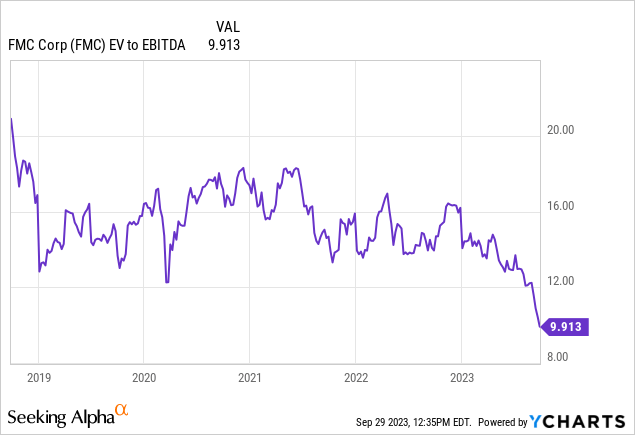

Valuation-wise, the stock is trading at 10x LTM EBITDA as investors have become much less bullish on agriculture.

I believe a higher valuation will be applied once FMC proves it is indeed seeing an acceleration in orders after 2023. However, it needs more than that. I believe that once economic growth bottoms and money flows into cyclical investments, the stock will see a 14x EBITDA valuation – or higher. I also expect EBITDA estimates to be hiked in the next two years.

When adding a 14x multiple to current estimates, the stock has a fair value of $131 per share, roughly 97% above its current price.

The current consensus price target is $114.

At this point, one may ask why I don’t own FMC shares. That’s due to my trading portfolio being overweight agriculture and energy. I own fertilizer stocks, and I have a (relatively speaking) large position in Deere & Company (DE) in my dividend portfolio.

I’m not yet sure how I can incorporate FMC into my strategy, despite its attractive long-term valuation.

I will maintain a Buy rating. However, investors need to be aware of the cyclical risks that remain. We could see another move lower if economic demand further deteriorates. This could hurt crop prices and farmer margins, delaying potential mass orders for FMC’s products.

So, yes, I do expect FMC to double over the next 2-3 years. But no, it won’t likely be an easy ride.

Takeaway

FMC, a leader in the agriculture input sector, has faced challenges like inventory de-stocking and adverse market conditions. However, they’re well-positioned with a robust product pipeline and a commitment to innovation.

The company’s positive outlook for the future, with improved margins and growth projections, combined with a healthy balance sheet, suggests a brighter horizon. As economic conditions stabilize and cyclical investments gain momentum, FMC’s stock could see significant valuation upside.

While I currently don’t hold FMC Corporation shares due to my portfolio allocation, I maintain a Buy rating for it. Nevertheless, investors should be aware of potential cyclical risks. The journey ahead may not be without its bumps.

Read the full article here