Investment Thesis

Diversified Energy Company (OTCQX:DEC) has an intriguing business model and is well-placed to take advantage of a strengthening market for natural gas. As the owner of the most natural gas wells in the country, they also have significant upside potential if commodity prices rise or new technologies allow producers to improve recovery rates. However, after digging in to the company’s business model, financials and recent acquisitions, I’ve decided against making an investment.

Industry Backdrop

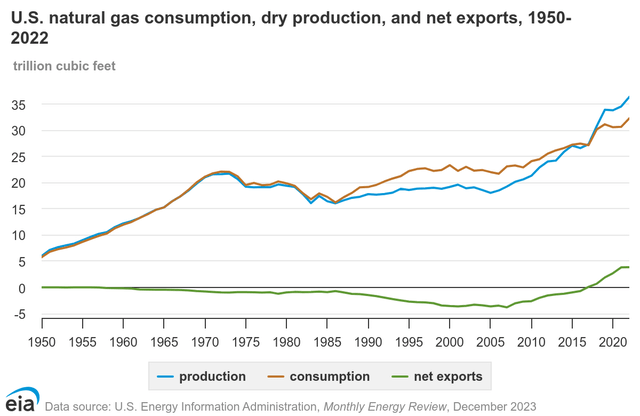

If you believe, as I do, that natural gas has a bright future, there’s a lot to like about Diversified Energy. Natural gas is firmly entrenched as a cheap and widely available source of energy for industrial processes, residential and commercial heating, and dispatchable electricity generation. Growing demand has been a boon to producers, while growing shale gas production has kept prices low for consumers, thereby increasing demand in a virtuous cycle.

EIA

EIA

There are dozens of American companies that produce natural gas, from Appalachian shale producers like EQT Corp (EQT) and Chesapeake Energy (CHK) to oil majors Exxon Mobil (XOM) and Chevron (CVX). These companies have done very well in the past few years and may prove to be great investments going forward, but most investors understand that, and they don’t quite have the discount to fair value that I typically look for. That bargain hunting has led me to Diversified Energy.

Company Overview

Diversified Energy is a relatively small and unique oil & gas production company which primarily produces natural gas from “long-life low-decline” wells in the Appalachian and Permian Basins. Natural gas makes up 86% of production (on a BOE basis), with the remaining 12% and 2% coming from NGL’s and oil, respectively. The company is unique in that they don’t explore and develop new reserves like most producers and instead focus on acquiring older, more mature wells at a good price and optimizing production through the rest of the well’s economic life before capping it.

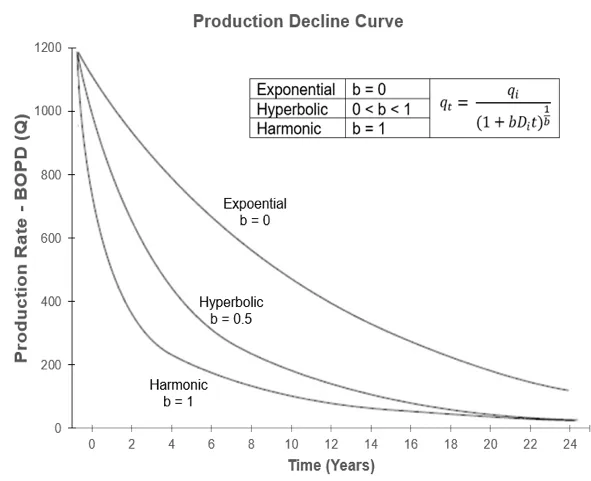

Oil & gas producers in the United States have reaped enormous benefit from the shale boom, which has helped expand American production of natural gas from around 18 trillion cubic feet (TCF) per year in 2005 to around 36 TCF in 2022. The horizontal drilling and “hydraulic fracturing” technologies which have enabled this expansion are effective in fossil fuel production, but they differ from “conventional” wells in an important way.

Rock River Minerals

Using the chart above as a reference (focus more on the shape of the curves rather than the numbers, as individual well production varies widely), note the difference in production rates over time between the “exponential” and “harmonic” decline curves. Conventional oil and gas wells typically follow an “exponential” decline curve, characterized by a relatively slow rate of production decline. In contrast, shale wells generally follow the “harmonic” decline curve, which results in a more rapid drop in production. While initial production from shale wells can be quite prolific, most of the production comes in the early years, with extraction rates dropping as low as 10% of initial production within 3 years. Oil & gas production companies in the Permian Basin have recently reported higher-than-expected depletion rates as production from shale wells drops more quickly than initially expected. While this presents an obvious challenge for exploration and development companies, it presents an opportunity for a company like Diversified Energy.

The value of depleted wells is a function of both remaining production (an asset) and the asset retirement obligation associated with capping and retiring a well in a way that complies with regulatory requirements (a liability). Most oil & gas production companies understandably avoid throwing good money after bad and prefer to redirect capital towards exploration and development for the next “gusher”. These older, unloved wells are where Diversified Energy sees opportunity.

Diversified Energy seeks to purchase these wells at valuations that are heavily discounted from the projected value of future production. The company then deploys rigorous field management programs and refreshes infrastructure in an effort to improve well performance. They also emphasize operational efficiencies, which help them operate these declining wells at a profit for as long as possible. Diversified Energy claims their efforts resulted in an annual production decline of just 10% across the wells in their portfolio.

When the time comes to finally retire these older wells, the company offsets a portion of the cost of retiring the asset retirement obligation (ARO) liability through their “Next LVL” well retirement business. This business specializes in safely and responsibly retiring oil and gas wells and completed 404 well retirements in 2023 according to their most recent annual report. Over half (222) of these well retirements were completed on their own wells, with the balance made up of 148 “orphan well” retirements done for states (which bear responsibility for abandoned wells), and 34 retirements for third-party producers. This business was started in 2022 and annual revenue has already reached $28 million as of 2023. Diversified Energy doesn’t break out expenses for this business to determine its contribution to the bottom line, but the cash flow statement does show an operating outflow for well retirement of just $6 million in 2023, indicating the business is likely already profitable.

An Uncertain Liability

At this point, it’s prudent to acknowledge an important source of uncertainty around the company. Diversified Energy carries ARO liabilities on their balance sheet at the discounted value of their retirement cost estimate, which they currently peg at about $23k per well. This is on the low end of the industry average cost of $20-$40k per traditional well, but some sources expect costs to run closer to $300k for shale wells. Due to their business model, the company owns around 70,000 traditional and shale wells, which is more than any other oil & gas producer in the country! If the company were theoretically required to retire each of these wells immediately, the cost at $23k per well would be around $1.6 billion ($23k * 70k wells)! I give this extreme, unrealistic scenario to give a sense for the amount of cash the company will eventually have to spend on retirements in the future. The actual liability is carried on their balance sheet at just $500 million at YE 2023 due to the impact of discounting future expenses (covered later). However, if regulators become more aggressive on this front and require quick retirements with higher emission standards, there is a risk that the associated costs run well above that.

To offer my personal take on the regulatory issue, the recent reversal of the “Chevron doctrine” by the Supreme Court should significantly weaken the power of federal regulatory agencies without an explicit mandate from Congress, which is a difficult thing to get at the moment. At the state level, I think regulators are unlikely to force expedited well retirement that would threaten the viability of oil & gas production companies because the liability of well retirement falls to the state if these companies go under. While some states in the Appalachian region may be less politically inclined to help oil & gas companies, they do have an interest in seeing existing wells retired rather than left abandoned and leaking methane indefinitely. Recent acquisitions (covered later in the article) have been in an area the company calls the “Central Region”, which is located in Texas, Louisiana and Oklahoma and should see more favorable regulatory treatment given the political environment in that area.

Anxiety around the company’s business model was evident in a letter sent last year to the CEO, Rusty Hutson, by Democrats in the House Committee on Energy & Commerce. The Committee mainly takes issue with Diversified Energy’s plan to continue operating marginal wells for long periods of time, along with the resulting financial impact of pushing the cost of those retirements further into the future. As an example given, the committee sites the company’s 2018 asset acquisition from CNX, where CNX accounted for the ARO liability of the acquired assets at $197 million and Diversified Energy recorded the same liability at $14 million. While politics tend to distort facts to favor one’s own argument, it’s certainly worth inquiring about what created this vast discrepancy. Essentially, it all boils down to the present value of retirement costs. If CNX had planned on retiring a particular well in 10 years and made a conservative estimate of $50k for retirement costs, that ARO would cost around $20k in present value terms at a discount rate of 10%. If Diversified Energy acquires these wells and pushes the retirement date out 50 years, even if the cost to retire the well increases at an inflation rate of 3% to about $100k at the time of retirement, the present value of the ARO would be just $850, or about 23 times less! The equivalent factor given by the House Committee above is about 14 for comparison, and is a function of the weighted average age of the wells, nominal retirement cost estimates, and the discount rate.

What to make of all this? The answer comes down to your faith in the company’s ability to exercise sound judgement on acquisitions and profitably produce gas from their plethora of marginal wells for a long period of time. This requires management that intuitively understands sound capital allocation and also possesses the operational expertise to keep expenses low while operating low-volume wells as long as possible. To evaluate their performance along these lines, I’ll give a brief summary of how the company got here and do a deeper dive on the two acquisitions announced so far this year.

History of Acquisitions

Diversified Energy hasn’t been a public company for long, and they’ve grown largely through acquisitions. The company was founded by current CEO Rusty Hudson in 2001, when he purchased a package of gas wells in West Virginia. He continued growing the business by purchasing gas wells and eventually listed the firm on the LSE’s AIM market in 2017. They recently made a second listing on the NYSE in December 2023.

Diversified Energy has expanded rapidly since 2018 by purchasing tens of thousands of wells along with the associated midstream assets, the sum of which amount to a net $2.5 billion including divestitures. To fund these purchases, the company has issued over 40 million shares of stock and grown long-term debt from $71 million at the beginning of 2018 to over $1 billion today. They’ve also teamed up with a private equity company called “Oaktree Capital Management” on several acquisitions recently, with Diversified Energy typically taking a controlling 52% stake after the transaction.

I think there’s promise in the company’s business model of purchasing unloved assets and then focusing on efficiently operating them for as long as possible, but it’s essential that management understands and focuses on financial returns and prudent capital management rather than growth at all costs. One thing working in shareholders’ favor here is the fact that this business is still run by the founder, Rusty Hutson, who has a roughly $20 million stake in the company. In a recent interview, Rusty spoke about the importance of making sure acquisitions were accretive to shareholders. As the largest individual owner of company shares, a sizable amount of his net worth aligns him with external shareholders. However, that fact alone doesn’t automatically guarantee good decision-making. Instead, let’s evaluate the two acquisitions announced so far in 2024 as a litmus test.

|

Acquiree |

Oaktree |

Crescent Pass Energy |

|

Purchase Price ($1,000) |

$410,000 |

$106,000 |

|

Production (MMcfe/day) |

122 |

38 |

|

Production (MMBtu/Year) |

38,610 |

12,026 |

|

Natural Gas Price Estimate ($/MMBtu) |

$3.50 |

$3.50 |

|

Revenue ($1,000) |

$135,134 |

$42,091 |

|

Expenses ($/MMcfe) |

$1.57 |

$1.57 |

|

EBITDA ($1,000) |

$74,517 |

$23,210 |

|

Interest ($1,000) |

$9,000 |

$0 |

|

25% Corporate Income Tax ($1,000) |

$16,379 |

$5,802 |

|

Earnings before Depreciation and Amortization ($1,000) |

$49,138 |

$17,408 |

|

Maintenance Capex (assumed $0.25/MMcfe) ($1,000) |

$9,652 |

$3,007 |

|

Annual Owner Earnings ($1,000) |

$39,485 |

$14,401 |

|

Dilution from Share Issuance ($1,000) |

$28,475 |

|

|

ROI |

9.63% |

10.71% |

The company announced on March 19 that it planned to acquire Oaktree’s interest in certain assets in the Central region, and later announced on July 10th that they would be acquiring upstream assets from Crescent Pass Energy. Management claims to be acquiring the Oaktree assets at a PV17 valuation (meaning it equates to fair value at a 17% discount rate) with a purchase price multiple of 3X on adjusted EBITDA. The Crescent Pass acquisition is being done at a PV20 valuation and 3.8X purchase multiple.

Charlie Munger may have described EBITDA best when he referred to the metric as “bullshit earnings”, and it’s in that spirit that I’ve endeavored to determine the true economic value of these acquisitions. Based on assumptions in the chart above, I estimate the annual earnings available to shareholders on these acquisitions is roughly $40 million for the Oaktree acquisition and $15 million for Crescent Pass. These estimates assume a $3.50/MMBtu sale price for natural gas, $1.75/MMcfe production expenses and roughly $0.25/MMcfe in maintenance capex based on the company’s own historical results. These assumptions point to owner earnings, which equate to a roughly 10% initial return on capital next year. However, keep in mind production from these acquired assets will continue falling by around 10% per year into the future. The acquisition looks better if you assume increasing demand takes the price of gas higher in the future, but my projected natural gas sale price of $3.50/MMBtu feels generous, with spot prices currently closer to $2. Estimating a price beyond that level feels speculative to me. If you calculate the return on capital as a multiple of EBITDA you arrive at a number closer to 20%, but that doesn’t reflect the value to shareholders after very real interest expense, taxes and maintenance capex. Additionally, issuing shares to fund the Crescent Pass acquisition when the price has roughly halved in the past 2 years seems ill-advised unless you truly are getting a bargain on asset purchases.

Oil & gas production is a capital intensive business, and equity placements are often a large part of how companies in the industry expand without taking on too much debt. However, issuing equity because it will be accretive on a cash basis seems short-sighted. A significant amount of oil & gas operating costs are fixed and will remain the same or increase on a nominal basis due to inflation even as production from these marginal wells decline. These assertions may be subjective, and it’s possible that I’m not seeing the full picture, but if that were the case I would expect insiders to be purchasing the shares hand over fist given all the recent acquisition activity and the seemingly cheap valuation, but that’s simply not the case with just £65,000 purchased by 6 insiders over the past year.

Summary

Despite all the skepticism I’ve expressed, Diversified Energy has a lot going for it. The natural gas production industry should have significant tailwinds as LNG exports and natural gas fired electricity generation ramp up towards the end of this decade. If growing demand outweighs supply and the price of natural gas rises, Diversified Energy’s economically viable production capacity should rise as well. As owner of the most natural gas producing wells in the country, the company is also well-placed to take advantage of the development of new technologies that may allow producers to increase recovery rates. I also like the well retirement business (Next LVL) that the company is building and think this may become a major organic growth area for them.

However, I’m not impressed by recent capital allocation decisions and certain aspects of the business model concern me. While natural gas prices are currently very low by historical standards, most of the industry expects prices to rise again in the next few years as a multitude of developing LNG export facilities come online, and gas production assets seem to be priced accordingly. If industry developments play out to the downside of consensus expectations (as they often do) Diversified Energy may have a much harder time operating their wells profitably. The company aggressively hedges production, which is appropriate given their capital structure, but that also limits the upside for shareholders.

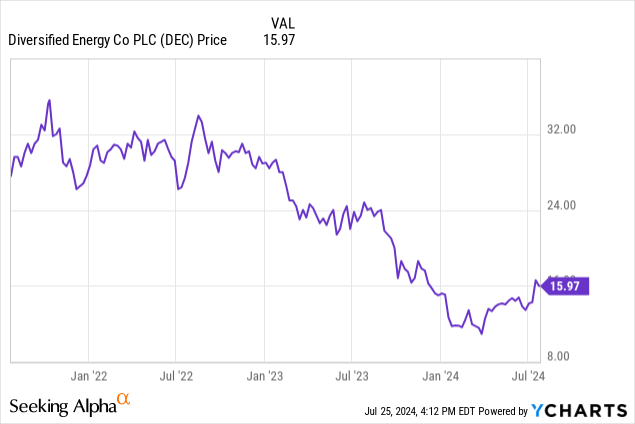

For those reasons, I remain intrigued by the company but will stay on the sidelines for now. If the share price declines closer to the $10-$11 range and insiders start purchasing a significant number of shares, I may revisit my conclusion.

Read the full article here