At the end of 2023, I reviewed Williams-Sonoma (NYSE:WSM) and thought the company seemed poised to continue to grow in 2024 and beyond. Since that time, WSM’s stock has risen by over 50%, far surpassing the S&P 500 and my own expectations.

WSM had a great Q1, beating estimates and reaffirming sales guidance. Although, I think WSM is still a great long-term play, I’m downgrading the company to a “Hold” as I think the stock is getting more expensive and there is a risk consumer spending will decline.

Let’s dig into the Q1 2024 financial results and recent company news as I explain why I’m not adding to my WSM position.

Company Updates

During WSM’s Q1 2024 earnings call, the company’s CEO Laura Alber laid out the organization’s key priorities for the upcoming year. The three priorities are, returning to growth, elevating customer service and driving margin.

In terms of returning to growth, management noted several growth drivers which include brand growth, category growth, business-to-business opportunities and global growth.

The following table from the company’s most recent 10Q filing shows the percentage change of brand revenue:

SEC.gov

As you can see, Pottery Barn Kids and Teen performed well for the quarter, but the other brands were down or nearly flat. On the call, Alber noted one collaboration with Deepika Padukone helped drive impressions for the Pottery Barn brand. I think continued collaborations such as this one can help drive future growth, especially if WSM can continue to work with global stars such as Padukone.

Regarding business-to-business, WSM grew this area of the business by 10% in Q1 2024. Alber noted various positive signs in B2B stating:

We’re encouraged by our diverse book of businesses ranging from Sofa’s for UC San Diego dorms to corporate gifting for Pebble Beach Company. We also saw continued growth for our existing large project customers such as Marriott, Dave & Buster’s and Jamestown Properties.”

In terms of global growth, Alber noted positive signs in key markets such as India, Mexico and Canada.

Regarding the second priority, elevating customer service, Alber talked about using artificial intelligence to improve numerous aspects of the business to create a better experience for the customer. Alber stated:

From product discovery and selection to personalization to concept to customer care and to the final mile, our team is constantly thinking about how we can improve our best-in-class e-commerce experience. And one way we do this is through AI.”

AI can also be used by WSM as a design tool and as a way to create supply chain efficiencies, such as finding delivery improvements.

This brings me to the last priority, which is driving margin. AI can certainly help in this area as well with supply chain efficiencies. Cost control and advertising costs play a key role as well, but thus far in 2024 WSM is hitting their targets (which I’ll get into below).

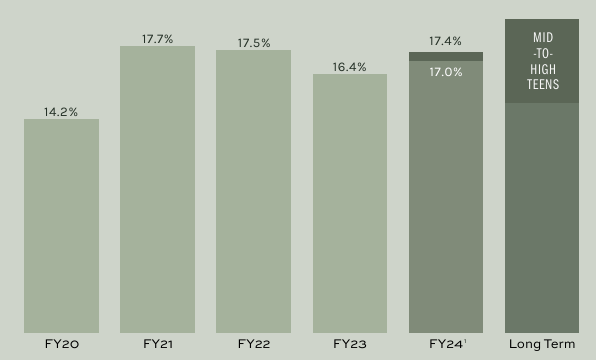

As noted in the graphic below from an investor presentation, the organization’s long-term goal is to have operating margin in the mid to high teens:

Investor Presentation

Let’s dig into these operating margins further and discuss the company’s financials for Q1 2024.

Financials

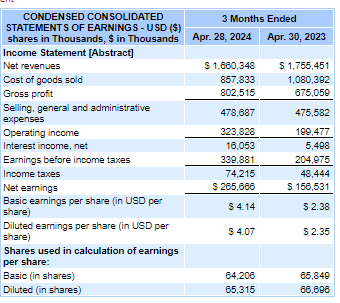

WSM delivered a strong quarter as revenue for Q1 2024 came in at roughly $1.66 billion, which is a 5% decline compared to Q1 2023. Despite the revenue decline, the company was able to improve margins and increase their net income and earnings per share compared to a year ago, as you can see below:

SEC.gov

On the company’s earnings call, management noted they were able to improve gross margins because of lower ocean freight costs, supply chain efficiencies and reduced occupancy costs. Management also noted an out-of-period adjustment of $49 million, which also helped margins. For the quarter, gross margin came in at 48.3%, and without the adjustment, gross margin would have been 45.4%. Operating margin for the quarter was 19.5% and without the adjustment, 16.6%

Management reiterated revenue guidance in the range of -3% to 3% growth, with comps in the range of -4.5% to 4.5% for the 2024 fiscal year. WSM raised their guidance for operating margin, as the company now expects operating margin between 17.6% and 18% for the year.

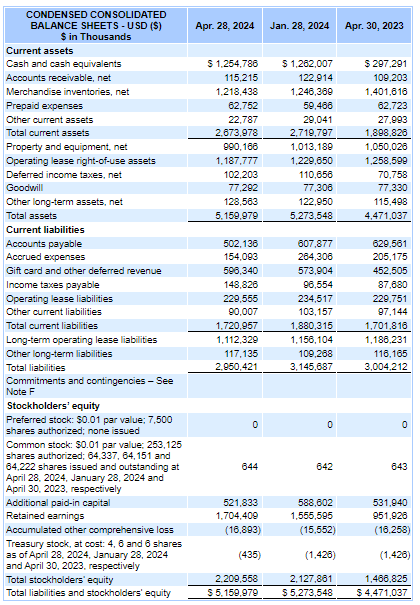

The company has maintained an excellent balance sheet, as you can see below:

SEC.gov

WSM has a sizeable cash balance of roughly $1.3 billion in cash and more than enough current assets to cover all the organization’s current liabilities.

In regard to shareholder returns, the company delivered $107 million in returns, $63 million in dividends and $44 in stock repurchases.

Valuation

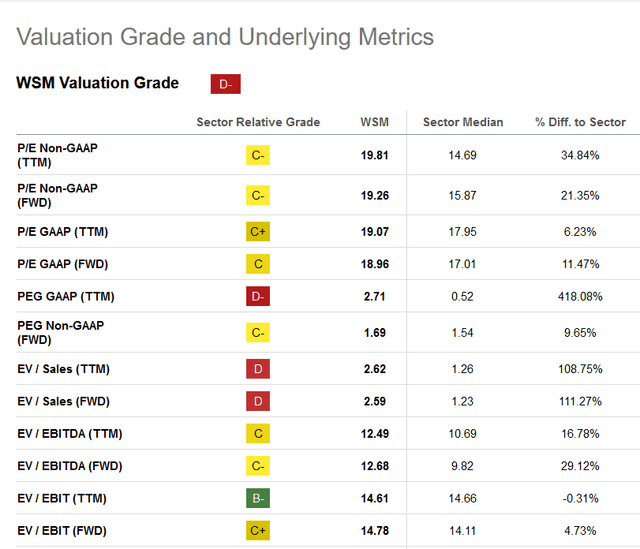

As you can see from the below valuation metrics, Seeking Alpha’s overall value grade for WSM is a “D-.”

Seeking Alpha

In my prior analysis, the company’s price to earnings ratio was roughly 14. As you can see, it has increased to nearly 20.

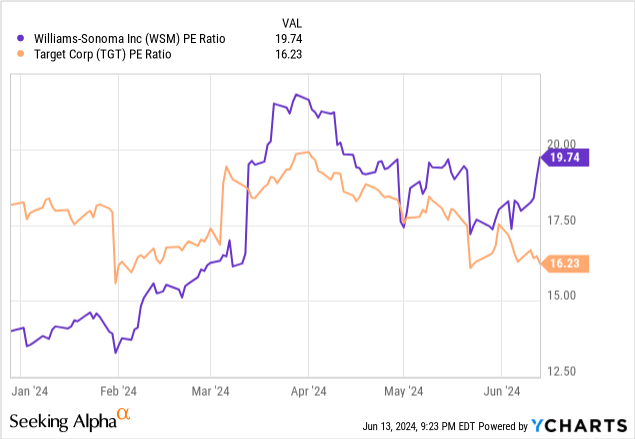

To compare WSM to Target, you can see their PE ratio has declined, and their price stock hasn’t performed nearly as well as WSM. I know it’s not an apples to apples comparison in terms of the businesses, but these are both established retail companies. I wouldn’t consider adding shares of WSM until their P/E ratio at least was closer to Target’s P/E ratio of 16.

Risks

I think one clear near-term risk, is a decline in consumer discretionary spending. The majority of WSM’s brands have a higher price point aimed at the middle to upper class. Many analysts on the call asked about the macro and Alber’s thoughts on consumer spending and high-ticket items. Alber stated WSM has mostly been immune to weakness in consumer spending as she said, “We haven’t seen a trend in high-ticket softness, we’ve seen more of a furniture softness trend that appears to be better.”

Alber went on to say having high-quality, innovative products is what WSM customers have come to expect from the company.

Other companies such as Target (TGT) and Home Depot (HD) have noted softness in consumer discretionary spending.

I do think WSM targets a higher income class, yet these consumers might begin to feel more impacted as interest rates continue to remain high for the rest of the year (as many estimate the Fed will only cut rates once, if at all, in 2024). These consumers may opt for cheaper alternatives such as Wayfair (W) or even a Target or Walmart (WMT).

Conclusion

WSM delivered excellent Q1 2024 results as the company is making strides on each of their 2024 priorities, especially driving operating margins.

I think WSM is a great business, yet the current valuation seems higher after the stock has run-up faster than I expected thus far in 2024.

Furthermore, I think there is a good chance consumer spending declines as consumers focus more on essentials and less on high-ticket items.

I plan to hold my current shares and not add further until the company’s stock price gets to a more reasonable level.

Read the full article here