A resourceful fast growing company

Workday (NASDAQ:WDAY) is a cloud native ERP, (Enterprise Resource Planning) platform providing the full gamut of services within two focus segments, HCM (Human Capital Management) and Finance. Started in 2005 by PeopleSoft executives, including its founder Dave Duffield, Workday competes for corporate budgets mainly with Oracle Corporation (ORCL), SAP SE, (SAP), ADP (ADP) and Ceridian HCM. PeopleSoft was acquired by Oracle.

Workday is having an outstanding year beating on both top and bottom lines for the first half of 2023 and expects to grow its top line and adjusted operating profits 16% and 38% respectively for the full year.

I see a bright future ahead with 3 year top line growth of 18% and Adjusted EPS growth of 28% as operating leverage and scale increases profits faster. This is even more impressive in a tough year, clearly Workday’s integrated platform for two crucial operating areas, people and finance have kept them ahead of its competitors.

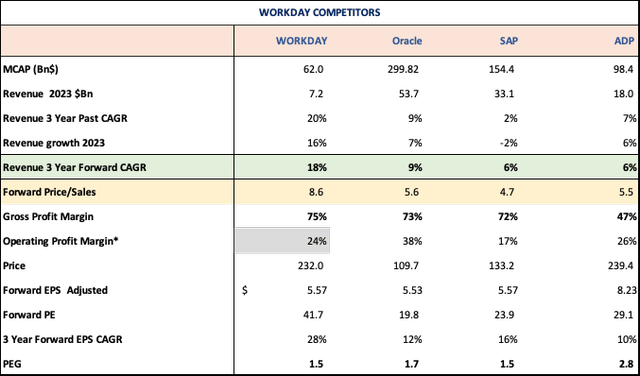

Workday Competitors (Seeking Alpha, Workday, Oracle, SAP, ADP, Fountainhead)

* Workday Adjusted, others GAAP

Revenues: Workday is forecasted to grow quickly at 18%; its closest competitors are not even in double digits. Of course, both SAP and Oracle are 5 to 8 times Workday’s size, and not surprisingly aren’t expected to grow as fast on much larger bases. Besides, Oracle has seven business lines, some legacy on-prem and some of those from acquisitions, where the scope for the same rapid growth is just not the same as organic cloud growth. Oracle’s cloud platforms do grow faster, but the legacy businesses weigh it down. SAP too has several enterprise management segments besides subsidiaries like Ariba (payment management), Concur (expense management), and supply chain management among others. Because of the diverse and legacy businesses, SAP’s growth also gets diluted. ADP’s main strength is HCM, which evolved from payroll and its PEO, (Professional Employer Organization) tends to be cyclical, thus not having the same revenue growth.

Profits: Besides ADP, all three have gross margins in excess of 70%. Oracle, SAP, and ADP are more profitable at the operating level, with 38%, 17% and 26% respectively, with ADP having the best leverage on lower gross contributions. Workday on the other hand was not GAAP profitable at operating levels through FY2023, with its huge share-based compensation (not inconsistent with its Silicon Valley, cloud native, fast growing tech roots). It was GAAP profitable in Q2-FY2024 with $36.3Mn in operating profits and reported GAAP net income of $78.6Mn for Q2 and $78.8Mn for the first half of FY 2024. As shown in the table, I expected it to have non-GAAP operating margins of 24% for FY2024.

EPS: Finally, on adjusted EPS (I took adjusted EPS of all four to be consistent) Workday again dominates with forecasted EPS growth of 28% in the next 3 years, getting a strong bottom line with from the 18% revenue growth, which results in a P/E of 42, but a reasonable PEG of 1.5, which is lower compared to 1.7 for Oracle, 2.8 for ADP and the same as the slower SAP. Its valuation is not stretched over the long term.

Workday looks solid as an investment in a cloud based single architecture environment, clearly outshining its legacy on-premise, hybrid, and cloud competitors.

The Bull Case for Workday

Market leadership, size and growth

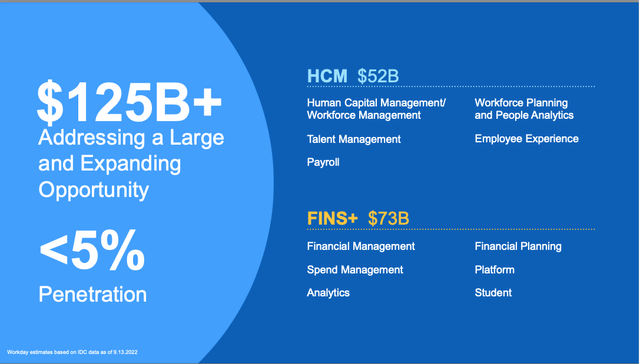

Workday TAM (Workday)

As we can see above this is a large TAM and Workday has the growth to keep gaining share in a market looking for integrated solutions.

Workday is the market leader in HCM and one of the fastest growing at 22%. CO-CEO Carl Eschenbach also talked up their market leadership on the Q2-2023 earnings call.

We are the clear market leader for cloud HCM, and finance and our value proposition has never been more relevant or powerful.

Having both platforms together is a good strategy and lets Workday leverage HCM to add their Financial Management solution.

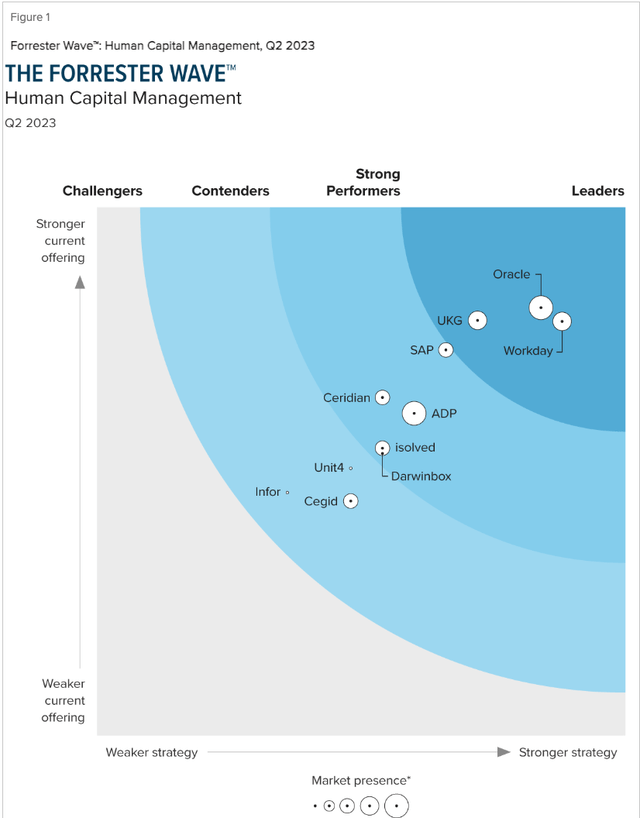

It was also named as a leader by Forrester in HCM with Oracle and SAP close behind.

Forrester Wave HCM (Forrester)

Workday is also making strong strides in their financial planning software getting named as a “Customer’s choice by Gartner, with a 4.85/5 rating, ranking above Oracle and SAP.

Integrated platform as the easy, user-friendly option

I worked for a CPA firm for several years, consulting with several companies in different industries as a Controller/CFO. Several of my colleagues and I found operating, payroll, enterprise resource workflow and accounting/financial software packages lacking in integration and comprehensiveness. Those heavy on industry focus and domain expertise would offer clunkier accounting packages or integration modules, which didn’t really integrate well. Integrating payroll was also not easy and for HCM you would have to order software packages separately for the human resources team. Many accounting packages also did not have FPA (Financial Planning & Analysis) modules. This was a trend especially in the small and medium sized market, and most business would have to spend either on people or buy integrations separately for other operations or workflows for order management, vendor management, supply chain and just use Excel for FP&A. This was across the board, an industry trend, and not just directed at any one of the four competitors mentioned here. For many users, the grass always seemed to be greener on the other side.

The other complaints were directed towards the patchwork of acquired companies, which again were not user friendly because of different architectures, modules didn’t work with each other, and many companies’ IT departments wasted a lot of time just teaching the workforce basic menu and reports navigation, besides spending time on lengthy onboarding. The trend in the last decade or two has also shifted towards self-support as platforms have gotten better and business have shifted to the cloud.

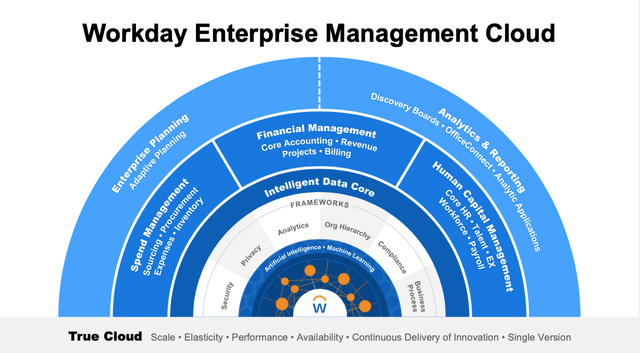

In my opinion, Workday has a competitive advantage because of its cloud based, single data architecture integration of its two main platforms, HCM and Finance, which takes care of four main areas Human Resources, Payroll, Accounting and Finance, which includes FP&A. Workday started much later with a cloud native advantage, thus eliminating so much of costly integration, and crossing over from on premise software. Workday has the breadth of a full-featured ERP tool, with as much capabilities of SAP and Oracle in these two workflows, and also is integrated and user friendly enough to go the self-service route, which is the trend and the most cost efficient method.

Workday’s Cloud Platform (Workday)

Solid team having a great year

A key factor has been continued leadership by the founders. Co-Founder Aneel Bhusri has been the Co-CEO of the company since inception and paved the way for Co-CEO Carl Eschenbach to take over as sole CEO from 2024, while retaining chairmanship of the board. Carl Eschenbach has a seasoned pedigree, with strong stints scaling businesses at Sequoia Capital and VMWare. Eschenbach has also been on Workday’s board since 2018, besides running Workday as a Co-CEO, and the transition couldn’t have been better planned. Second quarter results have been good and guidance also solid with a 24-month RPO rate of 23% and long term RPO growth of 32%, vindicating the choice to leave the reins in his hands.

The 24 month backlog grew at 23% to a pretty sizable $10.27Bn, with a gross retention over 95% and a Net Retention Rate over 100%, with longer contracts from new customers and renewal.

The R&D spend has been incredible with more than $11Bn spent in the last decade, growing 32% and averaging 40% of revenues. With higher revenues it’s at 37% this year, showing the commitment to building a great platform — Management clearly focusing on product development instead of GAAP profits. Commendably, dilution has come down to 3.9% in the last 4 years from an average of 4.5% prior, even with the large SBC.

Challenges

While I own and recommend Workday as a buy, I would like to point out that while Oracle’s overall growth is much slower, its cloud growth of 25% is very competitive. Secondly, for all the focus on machine learning and AI applications discussed on Workday’s earnings call, neither Oracle, nor SAP are falling behind in adding AI and machine learning to their products and services.

We also saw in the Forrester and Gartner reports, that the competition is close and going to get fiercer – both Oracle and SAP are larger, well capitalized and have strong financials. Besides, both Oracle and SAP compete in many more segments, which often are easier to sell as a bundle even if they are different platforms or solutions; the cost savings for a budget conscious customer is always a big factor.

Workday has other downside risks and challenges as well. Like other ERP solutions it comes with a hefty price tag, shutting out a lot of smaller businesses. Implementation is expensive and takes time and there are the inevitable switching costs from previous solutions. ERP solutions also have long sales cycles, especially in a difficult economic environment, which inevitably cost more in terms of sales and marketing expenses, eventually hurting its margins. The stock is also vulnerable to any reduction in growth expectations, which will hurt its price and multiple.

Valuation

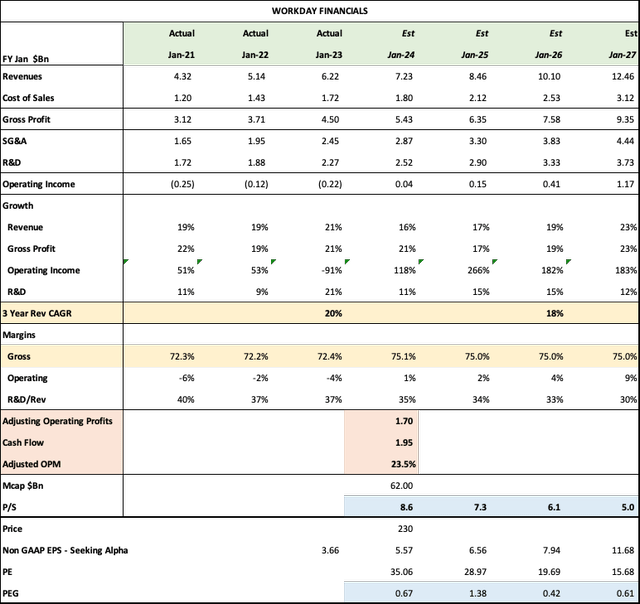

Workday Financials (Workday, Seeking Alpha, Fountainhead)

Sure, compared to its competitors Workday has almost twice the P/S ratio of 8.6, but it has twice the growth at 18% to 9% for Oracle and 6% for SAP, as shown in the competitor chart. Workday’s forward PEG ratio is only 1.38, which is reasonable for an 18% grower. This is a great price for a long term buy and hold.

Adjusted operating profits are also good at 23.5% of revenues, while cash flow, which grew 27% YoY is an excellent 27% of sales.

Importantly it has executed extremely well, and its integrated cloud platform should remain a big competitive advantage, with the relatively new CEO taking it to greater heights.

Read the full article here