Investment Thesis

XPEL (NASDAQ:XPEL) has been an outstanding performer over the last decade. The company specializes in a highly specific niche, focusing on products like Paint Protection Film. While they’ve had past success, the rising popularity of these products could cause that car manufacturers, who are presently clients of XPEL, to be enticed to explore additional revenue streams in a segment that is relatively easy to replicate and offers higher profit margins than car sales. And it appears that Tesla (TSLA) has already taken the initial steps in this potential trend, which raises concerns about the future prospects for XPEL.

In this article, we will delve into the recent Tesla news, XPEL’s response, and why I believe that the current valuation does not adequately account for these potential risks. This raises uncertainties about the stock’s potential performance in the medium term and it is the reason why I consider the company to be a ‘sell‘.

Business Overview

XPEL specializes in automotive paint protection films (PPF) and other automotive aftermarket products. Their primary product is a clear polyurethane film that is applied to the exterior of vehicles to protect them from various forms of damage, including stone chips, scratches, and environmental elements. The products are designed to protect different areas of a vehicle, including the front bumper, hood, fenders, mirrors, and more.

Below we will delve into the two segments into which the company separates revenues: Products and Services.

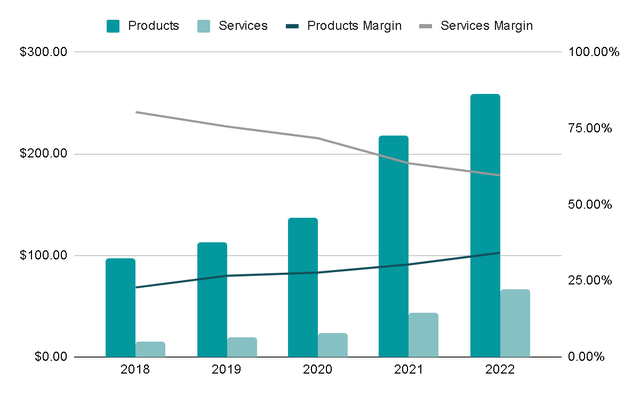

During FY2018, Products represented 87% and currently it is around 80%, while revenues from Services are increasingly gaining weight. In theory this should be positive, and it is, because Services have higher gross margins than Products. Specifically, gross margins for Products are currently 35% compared to 60% for Services. This implies that as Services increase in the Revenue Mix, margins should also increase.

The problem is that year after year the gross margins of the services have decreased, as can be seen in the following image:

Author’s Representation

Services

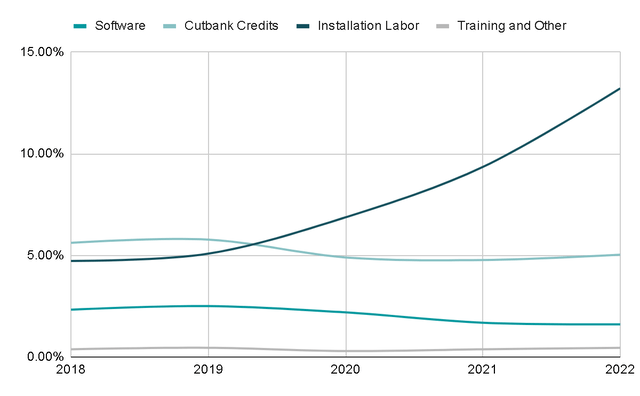

Revenue derived from services includes fees for DAP software access, cutbank credit, installations conducted at corporate-owned installation facilities and revenue generated from the provision of training services to clients.

The most interesting segment is the DAP software, which is a SaaS with a large database of cuts that help to cut automotive protection film into specific vehicle panel shapes. While this segment might be the most intriguing, as SaaS typically boasts very high profit margins, it only constitutes 1.6% of revenues, compared to 2.3% five years ago. This may lead us to think that clients cannot find significant added value in it and therefore they decide not to pay the subscription.

Cutbank is a per-cut charge is incurred for obtaining access to XPEL’s database of patterns. These are utilized as needed when the installer is prepared to apply the film to a vehicle. Revenue from this segment has remained stable, representing 5% of total sales.

The part of the revenue that represents the largest percentage of the Services segment, and each year has greater weight, is film installation. These are the installation services of various products directly to retail and wholesale customers through owned installation facilities. It is evident that XPEL is interested in increasing revenue from this segment, since in recent years the company has acquired businesses focused on the installation of protection films, such as Protex Center in 2020, PermaPlate in 2021 and an Australian supplier in 2022.

This does not seem entirely optimal to me, because the installation of film protection is not recurring and is much more cyclical than software, for example.

Author’s Representation

Tesla News and The Biggest Risk

As we have observed, XPEL products are somewhat cyclical, and a recession can have a significant impact on them. To compound this, on October 11th, news was released that led to a 15% drop in XPEL’s shares in a single day.

The news revolved around Tesla’s announcement that it would offer the option to include vinyl wraps, which they would install themselves, for the Models 3 and Models Y. In response to this, XPEL issued a statement, indicating that Tesla vehicles, in terms of both products and services, contributed only 5% to their overall revenues. In my view, while this 5% figure may represent the current contribution from Tesla, the concern lies in potential future revenue losses of Tesla’s electric vehicles clients, which have greater growth than traditional automakers.

Tesla’s decision to bypass intermediaries, such as XPEL, and offer these products directly raises questions about XPEL’s long-term prospects. It underscores XPEL’s ongoing efforts to secure contracts and partnerships with Original Equipment Manufacturers (OEMs) to establish installation programs for their brand of protection films. Furthermore, it raises a crucial question: How replaceable is XPEL? It appears that Tesla swiftly developed its own technology and began installing it independently. The growing trend of installing protection films among consumers may lead car manufacturers to view this as a potential source of additional revenue, offering higher margins than those derived from car sales.

After all, the product is more of a commodity with little differentiation, beyond the technology required to install the protection film properly. And considering that only 7% of revenues are linked to software services and database patterns, the company is quite vulnerable to losing revenue considerably in the future if OEMs begin to offer the product directly to their consumers.

Valuation

As a company offering a product with limited differentiation and operating in the consumer discretionary sector, the recent news about Tesla would typically lead one to expect the stock to trade at a reasonable valuation. However, this is not the case at first sight, as the Forward Price-to-Earnings Ratio stands at 30x, and the Fwd EV/EBITDA is at 20x.

To gain insights into the implicit growth assumptions embedded in the market’s valuation, I would like to perform a Reverse DCF analysis. We will provide information that we already know and we reverse engineer it to know the assumptions that exist in the current price of the stock, this TTM information is as follows:

- Free Cash Flow: $22.1M

- Shares Outstanding: 27.6M

- Cash: $14.3M

- Debt: $29.2M

- Expected Return on Investment: 15% CAGR

- Terminal Growth Rate:3.00%

- Share Reduction: 0.00%

When we factor in growth for the valuation, it appears less exuberant. Given the previously mentioned data, Free Cash Flow would need to grow at an annual rate of 37% over the next 10 years to achieve a return of 15% Compound Annual Growth Rate (CAGR).

My unconservative assumption is that Free Cash Flow will increase by 25% annually over the next decade. This means that, based on the current price, we could anticipate a 10% CAGR return. Considering the risks of the business and its cyclicality, I would feel more comfortable waiting for a higher return, of 15% or more to have a margin of safety in case things do not go as expected.

Author’s Representation Author’s Representation

Final Thoughts

Based on my analysis, I currently see no compelling reason to invest in XPEL. The product exhibits cyclical characteristics, lacks significant differentiation, and doesn’t appear particularly complex to replicate. Moreover, the current valuation doesn’t seem to fully account for these factors. While growth prospects may appear promising, there are questions about the sustainability of this growth, particularly given the consistent decline in revenues from services not directly related to the installation of the protective film, which, in the end, is closely tied to the sale of the product.

Considering these factors, I would assign a ‘sell’ rating to XPEL until the valuation aligns with the concerns mentioned.

Read the full article here