The following segment was excerpted from this fund letter originally posted on 4/16/24.

Xponential Fitness (NYSE:XPOF)

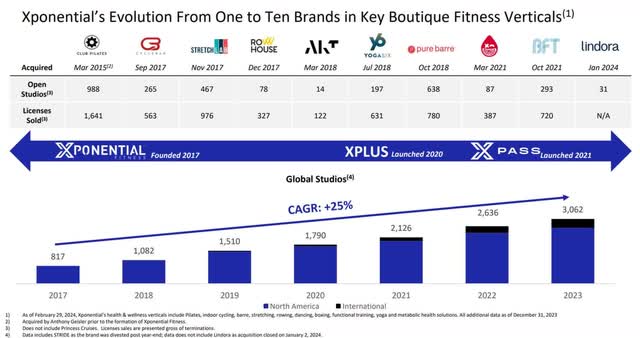

Xponential Fitness is one of the largest franchisors in the boutique fitness sector worldwide, owning ten brands, each offering a unique fitness experience. Its largest brands are Club Pilates, Stretch Lab, and Pure Barre.

Source: Xponential Fitness February 2024 Investor Presentation

The founder and CEO Anthony Geisler* has been successfully navigating the boutique fitness industry since the early 2000s. Geisler’s journey began with the acquisition of LA Boxing, which he transformed from a handful of locations into a network of nearly 100, culminating in its acquisition by UFC Gym for $25 million. Following a couple years with UFC Gym, Geisler’s desire to scale another boutique fitness brand led him to purchase Club Pilates for $2 million, which at the time had less than 20 locations and generated around ~$500k of EBITDA. Over the next 3 years Geisler grew Club Pilates to ~100 locations and ~$6 million of EBITDA, after which he sold the company to the private equity firm TPG for $100 million.

TPG’s acquisition marked the genesis of Xponential Fitness, with Geisler spearheading a multi-brand entity poised to repeat the success of Club Pilates. Today, Geisler owns around 15% of Xponential Fitness, which today is valued at ~$100 million. We believe, and historical performance suggests, Anthony Geisler is an exceptional CEO.

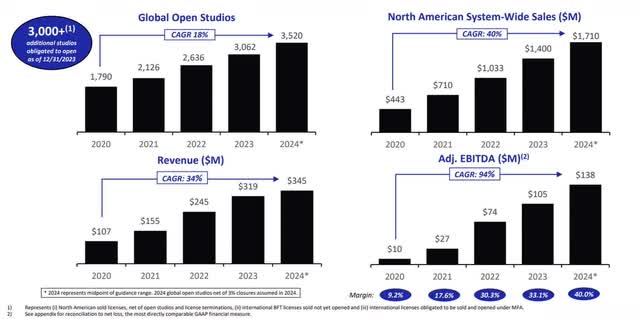

Source: Xponential Fitness February 2024 Investor Presentation

In the middle of 2023, an anonymous short report was released claiming that Anthony Geisler is an unethical, untrustworthy businessperson, and Xponential is an entity that oversells failing fitness concepts. Since this report was released the share price declined over 60% while the financial results continued to be robust. To address some of the concerns mentioned in the short report, the company hosted an investor day and dug into the health of the business and each individual boutique fitness brand. We believe the short report found a few disgruntled franchisee’s, which every franchise system has, and claimed their complaints are shared by the entire franchisee base. From our research we don’t believe this to be true. In aggregate the portfolio of brands is doing well, and franchisees are profitable and growing.

Ultimately after investigating all the claims from the short report and speaking with management on multiple occasions, we believe Xponential Fitness is a high-quality business trading at an extremely attractive price. Even if half the claims from the short report were true (which we don’t believe to be the case) we believe the business would still be worth significantly more than the current market price. Xponential will generate around $100 million of free cash flow in 2024 and is currently a ~$850m market cap company.

We believe Xponential can deliver on their 2026 adjusted EBITDA target of $200m (implying a 24% 3-year compounded annual growth rate) and their valuation will gradually return to ~20x adj. EBITDA (versus today’s valuation of ~7x adj. EBITDA) which is where Xponential was valued before the short report was released. Put together, this implies a target price in the next 2 years of $56, or a 275% return from today price of ~$15. We think the risk/reward is attractive.

|

Footnote *On 5/17/24 Xponential Fitness, Inc. announced that Anthony Geisler has resigned as Chief Executive Officer of Xponential. Brenda Morris will serve as Xponential’s Interim Chief Executive Officer. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here