Investment Thesis

Yum China (NYSE:YUMC) is a good business with a stable competitive advantage in the Chinese dinning market. The majority of its earnings are from KFC and Pizza Hut. Growth has been strong as it has been capturing opportunities across cities in China. Differently right now, the majority of these growth opportunities come from what are considered “lower-tier” cities. The scale of such is significant and large enough to support its current high-growth trajectory.

Out-of-context with respect to the overall market, its intrinsic valuation is attractive with an estimated upside of 18.5%. However, considering the recent poor stock performance, the dominating forces seem to be the broader market risks and due to momentum. This is why now is not the best time to enter as it may forfeit the opportunity for even better price to purchase a fundamentally strong and non-cyclical business.

Stock Overview

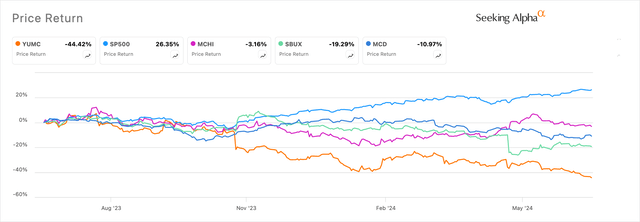

YUMC performance relative to benchmark and peers (Seeking Alpha)

Yum China has suffered from a declining trend since mid-2023, with a 1-year price return of -44% and -25% year-to-date. This is despite its outperformance against consensus EPS in fiscal years 2023 (EPS of $2 vs $1.92) and $0.72 vs $0.65 in FY24 Q1. Its valuation is cheap for what appears to be a high growth business (12.2% YoY revenue growth).

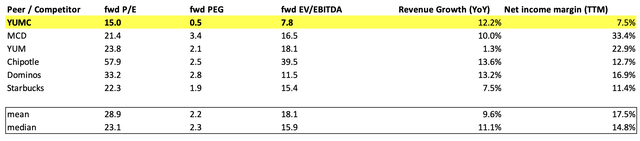

Peer Valuations

Seeking Alpha, Author’s Calculation

Tickers: YUMC, MCD, YUM, CMG, DPZ, SBUX

The peers were selected based on the fact that these are all businesses with “Moats” and comparable growth. They all have strong branding, a proven way of doing business, and track records of expanding consistently. (Check out: brands of YUMC)

More about Yum China itself. Since 2016, YUMC was spun-off from Yum Brands to exclusively focus on the China market. Back then, it operated around 7,500 stores with $6.7 billion in revenue and covering 1,100 cities. By the end of FY 2023, YUM had around 15,000 stores with $11 billion in revenue and covering over 2,000 cities. In that fiscal year, it opened 1,697 new stores with half of them in “lower-tier” cities (below tiers 1 and 2). This brings us to Yum’s current strategy to capture the massive consumption potential in lower-tier cities of China. With 15,000 stores in FY24 Q1, the company plans to bring that number to 20,000 by the end of FY26.

From the growth mandate, the pace of expected growth consensus is in-line with historical trajectory. The current share price of $31 and the well-below-peer forward price multiple is either a opportunistic mis-pricing, skepticism expressed in Yum China’s expansion trajectory, or poor risk sentiment in the overall market. I will discuss my stance on the stock by firstly looking at Yum’s growth capacity, then the implications of valuation, and lastly the opportunities.

Question: How Large Exactly Can YUMC Grow?

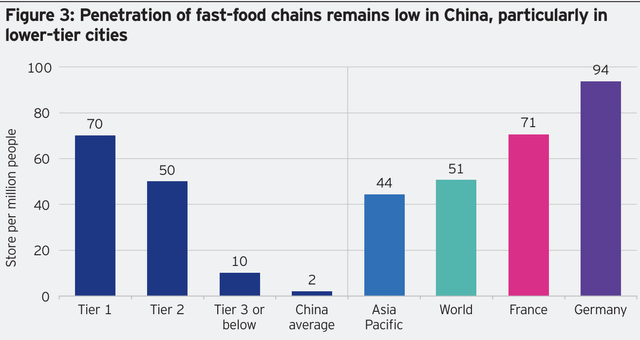

As we’ve seen, YUMC has been growing at an extraordinary pace since 2016 and way before that since it entered China. The first store of KFC was back in 1987, Beijing. Back then, China had a GDP per capita of less than $1,000 USD PPP vs. $22,500 in 2022. The reason I’m bring this up is because when Yum entered China back in the days, China’s extent of development and spending level were very low. As the living standard and consumption evolved positively overtime, Yum was able to capture the opportunity in this massive market. As of today, Yum’s growth mandate continues. But instead of capturing growth from tier-1 cities such as Beijing and Shanghai, their strategic mandate (FY23 10k; see RGM section) is to focus on lower tier cities where growth opportunities are strong and much untapped.

Morgan Stanley, 2017

These are cities that represent 70% of the Chinese population, and where the current penetration rates of fast food chains are low. In a study done back in 2018, lower-tier city consumption was expected to rise from $2.3 trillion to $6.9 trillion in 2030, 9% CAGR growth. This coincides with the growth the Chinese middle-class, a continuing driver to unlock the potential of the 70% population.

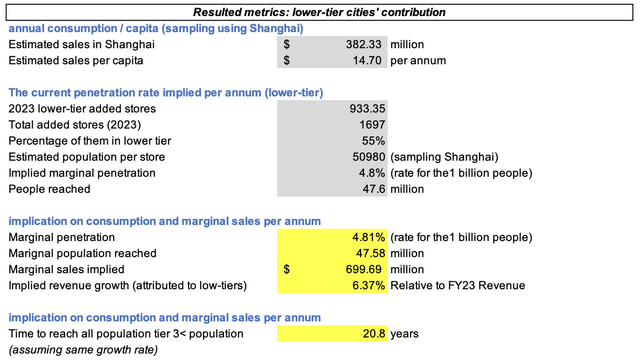

Lets look more closely into the implications of growth. As mentioned, in 2023, more than half of the additional 1,700 stores come from “lower-tier” cities. Suppose we assume the same mix of additional stores and estimate the per-capita consumption using existing stores/cities, the following is my rough estimate of growth and the growth potential under the current pace of expansion.

Estimate of potential sales growth (UBS, Yum China, author’s Calculation)

As we see from the estimate, the sole contribution from expanding into the lower-tier cities for Yum can be significant and sustainable. With the current market consensus, YUMC’s revenue and EPS growth will be around the 10% level for the years ahead. It can well sustained by the scale of the Chinese market and the unexploited opportunities that it currently offers in addition to the higher tier cities that it operates in. Please note that my calculations are meant to be a reference, not implying YUMC’s growth trajectory. The actual result will depend on factors ranging from the effectiveness of management’s strategic execution to the variability from sales given demand and foreign exchange effects. However, I do hope that it gives you more context on the current consensus. Overall, I don’t think skepticism of growth is material based the solid performance of FY23 where lower-tier expansion is a major growth driver. Also, YUM’s historical record of growing in the underdeveloped China serves a similar narrative in expanding its footstep in the developing cities. Next, I will move on to valuation.

Valuation Analysis: Dividend Discount Approach

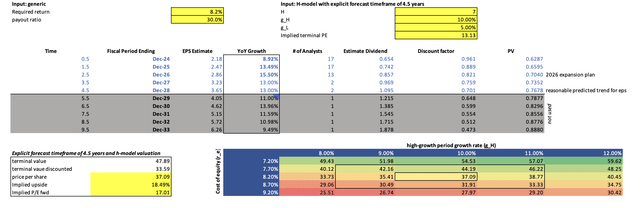

Before getting down to the numbers, I want to explain the discrepancies between consensus EPS and revenue growth where EPS growth generally seems higher. Along with Yum’s expansion plan comes a $3 billion repurchase/dividend plan within 2024-2026. In FY24 Q1, it paid $0.16/share dividend, a 23% hike from last year’s $0.13/share dividend. Common stock repurchases also reached $680 million vs. $60 million in FY23 Q1. In total, around $750 million were returned to shareholders as of now in the fiscal year of 2024. The commitment potentially implicates 1) management is bullish on performance and taking advantage of the current cheap valuation 2) consistent dividend policy which better justifies the use case for my dividend discount model. I am conservative with the model given that with YUMC, we are dealing with long-term speculation of growth, which is a very difficult to forecast. Here are some of the highlights of assumptions:

- A cost of equity of 8.2% is used. Beta (~0.87) is estimated in the recent 1-year period where covariance of return between YUMC and SP500 is fairly stable, and so is the broader market volatility. 4.2% risk-free rate is used based on 10-year treasuries. 4.8% US market risk-premium as per the estimate by Professor Damodaran.

- I used earnings consensus in the next 4.5 years and a payout ratio of 30%, which is fairly representative of the amount of dividend given the return-cash-to-shareholder program.

- To compute the terminal value, I used the h-model with the following parameters (half-time = 7 years (14 years of declining growth), high growth rate = 10%, terminal low growth rate = 5%). I believe this is reflective of the nature of Yum’s growth trajectory expanding its market coverage at a slowing pace as it consolidates.

Results and Limitations

Seeking Alpha, Yum China, author’s calculation

Overall, my target price based on the DDM model is $37.1 per share. It implies an upside of 18.5% and a forward P/E ratio of 17 vs. the current ~15. The valuation is based on short-term market estimates supported by the strategic narrative of Yum’s management, and the estimate of long-term growth potential. Based on historical data, the consensuses are generally conservative with the exception of negative earnings surprise in FY21 and FY22 due to Covid-19 in China. In the next section, I will discuss some of the key risks. To me, the implications of some of these risks are quite profound.

Investment Risks

Foreign Exchange: The Chinese Yuan is currently on a devaluating (CNY:USD) trend against the USD given its easing environment. Please note the significance this. Looking at FY24 Q1, a source of revenue underperformance is the effect of FX where revenue growth YoY is 1%, but excluding FX effect is 7%.

Growth: Although so far with the robust results of lower-tier expansion based FY23 performance, new target cities are heterogenous and how popular the product will be is uncertain.

China’s Macro factors: This has more to do with foreign exchange risks given the pace of easing. From a product demand side, Yum’s product should be fairly resilient against macro factors given its affordable and unique nature. I think most people would consume fried chicken at a fairly consistent frequency regardless of say what the home prices are tomorrow.

China’s Micro factors: Market competition in the Chinese restaurant market is strong. Although brands such as KFC and Pizza Hut have strong track records with significant competitive advantages, some of the emerging brands such as Lavazza in Yum China’s portfolio are still being tested with negative earnings. Although they represent less than 8% of revenue (FY 23), their success does have an implication on future growth. A future that can potentially bring lots of success.

Overall Momentum and market factors : YUM China’s Stock is performing poorly as mentioned. Based on the S&P breadth level, the downward trend is not only for YUMC but also for entire market (could be macro or political factors). I encourage you to monitor this strongly. I also think this factor prevails against all others.

Seeking Alpha

Conclusion

Overall, Yum China is a good business. It has a proven model and trajectory in the Chinese market. Its future growth potential on an industry level is significant. This is why it is expected by myself and the wider consensus that the elevated growth rate will continue.

My current price target is $37.1 with an upside of 18.5%. Although this is decent valuation, I do not recommend purchasing this stock. I suggest we use this as a reference and come back when the broader market risks stabilize. The sources of these risks could be from what’s going on within the US and China. Firstly, the Yuan devaluation is likely to prevail as the rate cut pace in the US is uncertain and unsettling for some. We also see the current falling breadth of the S&P which may be a result of election/policy and macroeconomic uncertainties within the US.

In the shorter-term, the market sentiment and risk appetite is certainly what prevails especially for a stock where all its exposure is in China, a seemingly uncertain environment. It is beneficial to monitor the decline to potentially capture a better price for what I believe is a great business.

Read the full article here