Back in December, I upgraded ZimVie Inc. (NASDAQ:ZIMV) to a buy after news of the company selling off its spine implants business to focus solely on dental implants. With the sale, ZIMV was able to significantly reduce outstanding debt and the resulting company appeared to be attractively valued compared to dental implant-focused peers.

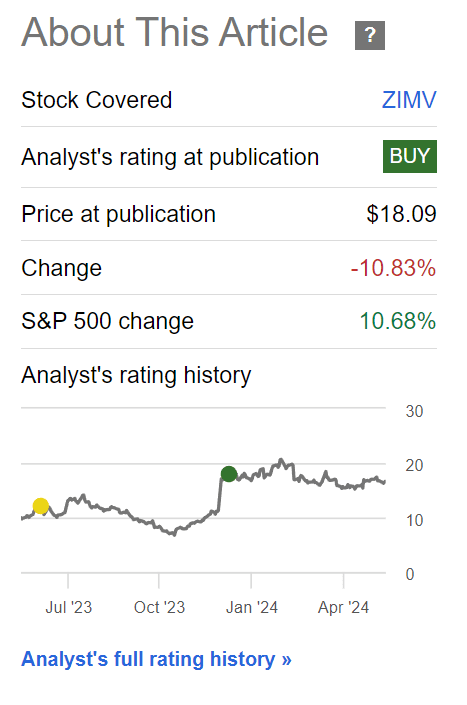

So far, my buy recommendation is not panning out, as ZimVie’s stock has declined by 11% since my last article (Figure 1).

Figure 1 – ZIMV stock has declined 11% since December (Seeking Alpha)

With the company recently reporting its fiscal first-quarter results, let us take another look at the company to see if my prior recommendation was correct.

Upon closer analysis, I believe my prior valuation work was done too hastily and incorrectly showed ZIMV as significantly undervalued. The company’s 2024 guidance implies a Fwd EV/adj. EBITDA valuation of ~10x, which is actually in line with ZIMV’s dental implant peers.

I remain concerned about ZIMV’s shrinking topline, and I am downgrading the stock to a hold. Until I see a sustained turnaround in dental implant sales, I believe the stock will remain range-bound.

Brief Company Overview

ZimVie Inc. is a small-cap dental implant pure-play that was spun out of Zimmer Biomet (ZBH) in 2022. Originally, when ZIMV was spun out in 2022, it comprised the non-core low-growth Dental and Spine businesses of ZBH. The spinout also saddled ZIMV with more than $450 million in net debt. Low-growth and high debt were a lethal combination, and ZIMV struggled to gain traction with investors as an independent company.

However, the company’s fortunes were improved in December 2023, when ZIMV announced the sale of its spine business to private equity firm, HIG Capital, for $315 million cash plus a $60 million promissory note.

From the company’s financial statements at the time, it appeared ZIMV sold the spine business for a good valuation, as the segment generated LTM revenues of $421 million and operating profits of $38 million.

With pro-forma net debt of ~$200 million and 2022 operating profits of $93.6 million in the surviving dental business, I estimated that ZIMV was attractively valued, trading at ~6x EV/operating profits (Figure 2).

Figure 2 – ZIMV segment operating income, 2022 (Company reports)

2023 Performance Continued To Show Declines

In hindsight, I was too hasty to rely on ZIMV’s 2022 financials.

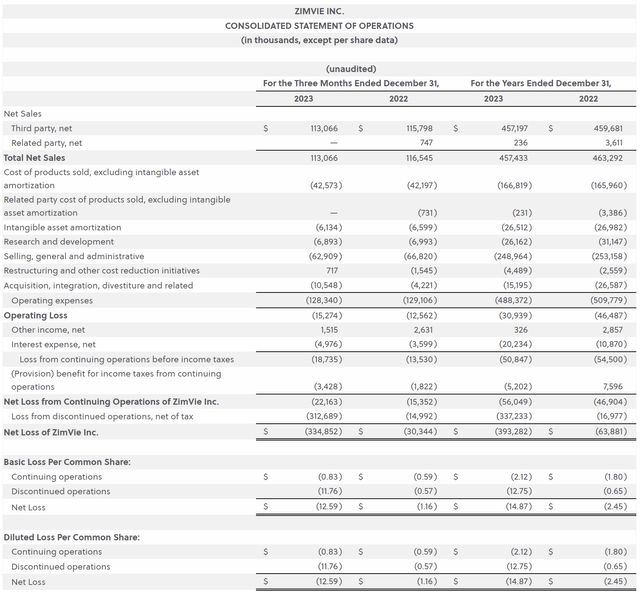

Recall, the main reason Zimmer Biomet decided to spin out ZimVie was because the spine and dental businesses were low-growth, mature businesses that did not appeal to ZBH’s management. Unfortunately, the dental business continued to shrink in the quarters since the spin-out, with full-year 2023 revenues of $457.4 million, a decline of 1.3% YoY (Figure 3).

Figure 3 – ZIMV 2023 financial performance (company reports)

Net income was an eye-watering loss of $14.87/share in 2023, as the company had to take a large write-down in the spine business that was classified as discontinued operations.

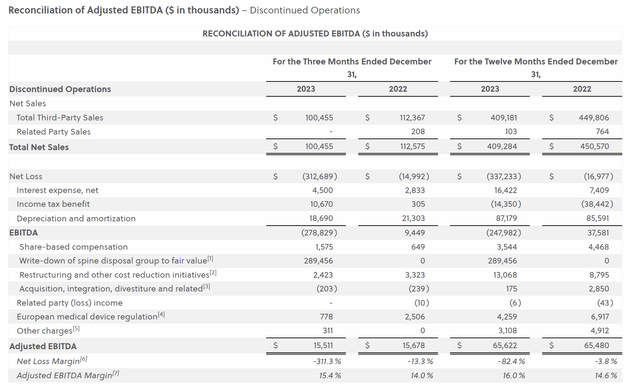

2023 adjusted EBITDA for continuing operations was flat YoY at $65.6 million (Figure 4).

Figure 4 – ZIMV 2023 adj. EBITDA (company reports)

2024 More Of The Same

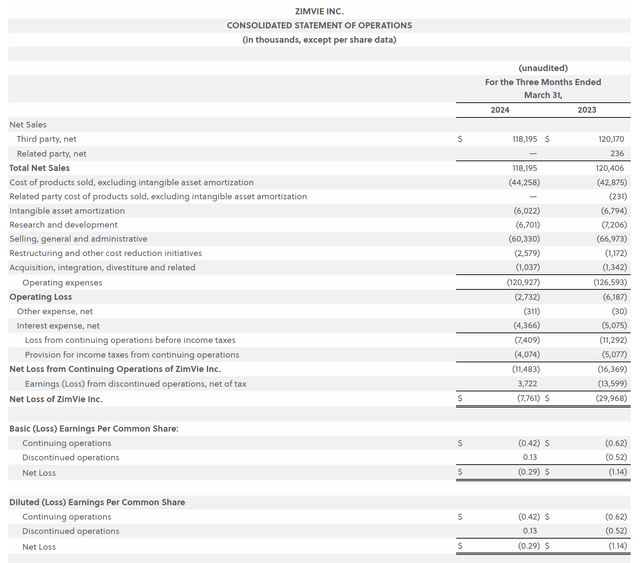

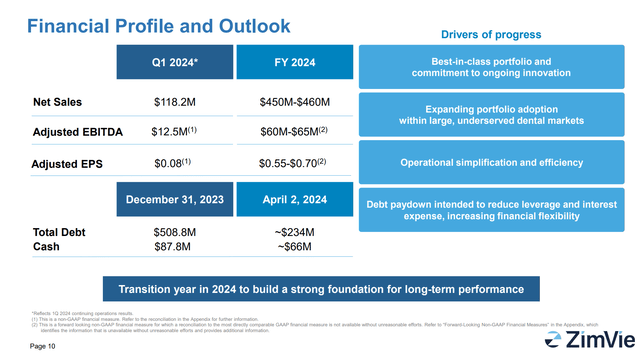

Unfortunately, so far in 2024, ZimVie’s financial performance has not improved despite management’s claim of sharpening their focus, as the company showed a further 1.8% YoY decline in revenues to $118.2 million in Q1/24 (Figure 5).

Figure 5 – ZIMV Q1/24 financial performance (company reports)

Net income remained negative at -$0.29/share. Worryingly, continuing operations showed a -$0.42/share loss, while the discontinued spine business actually recorded a $0.13/share profit.

But Adjusted EBITDA Shows Improvement

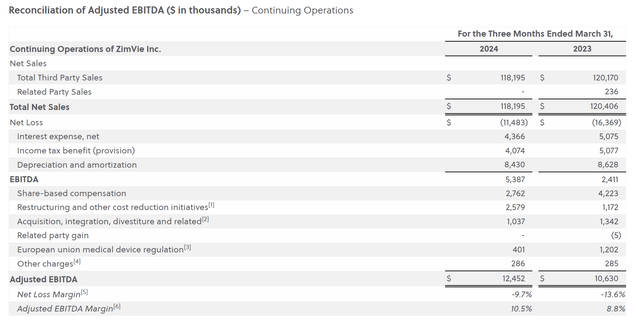

On the positive side, adjusted EBITDA for Q1/24 showed an 18% YoY improvement to $12.5 million (Figure 6).

Figure 6 – ZIMV Q1/24 adj. EBITDA (company reports)

2024 Guidance Underwhelming

However, despite a better YoY adj. EBITDA figure in Q1/24, the company’s full-year guidance for 2024 calls for a decline in adj. EBITDA to $60-65 million (Figure 7).

I believe the main reason ZIMV’s stock has been lackluster since releasing first-quarter results is because of the company’s guidance. With the first-quarter results, ZIMV released full-year 2024 guidance of $450-460 million in revenues and $60-65 million in adjusted EBITDA, or ~13.7% adj. EBITDA margin (Figure 7).

Figure 7 – ZIMV 2024 guidance (company reports)

Furthermore, while the revenue guidance is in line with figures ZIMV released in February when ZIMV released 2023 financial results, the adj. EBITDA margin guidance appears significantly lower at just 13.7% compared to 15%+ run-rate guided to previously (Figure 8).

Figure 8 – ZIMV prior run-rate guidance (company reports)

Valuation No Longer Attractive

In my previous article, my initial thought after the HIG transaction announced was that ZIMV was attractively valued, trading at a pro-forma 6x Fwd EV/operating income, with the key assumption that ZIMV’s run-rate operating income would be similar to 2022’s $94million.

However, with the release of the company’s 2023 financial results and 2024 guidance, my thoughts on ZIMV’s valuation have changed, as the company’s adj. EBITDA guidance is only $60-65 million.

With the HIG transaction closed on April 1st, ZIMV’s pro-forma Enterprise value is ~$620 million, as the company would have received $315 million in cash from HIG. $620 million in pro-forma Enterprise Value, compared to the company’s guidance of $62.5 million in adj. EBITDA implies a 9.9x Fwd EV/EBITDA.

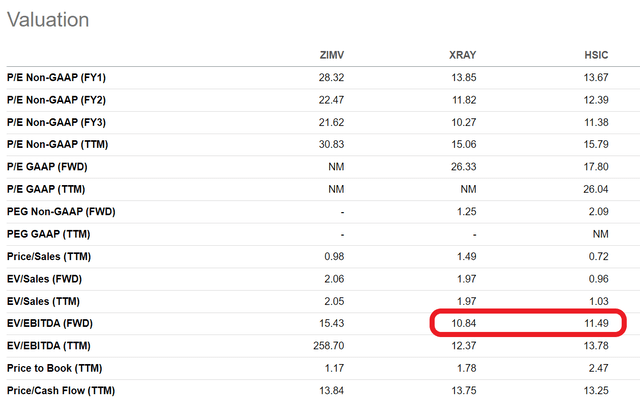

Based on pro-forma results, ZIMV no longer screens as significantly undervalued compared to the company’s closest peers, DENTSPLY (XRAY) and Henry Schein (HSIC), which trade at 10.8x and 11.5x Fwd EV/EBITDA respectively (Figure 9).

Figure 9 – ZIMV peer valuations (Seeking Alpha)

I believe ZIMV’s valuation discount, 9.9x compared to 10.8x and 11.5x, is warranted given the low quality of ZIMV’s earnings (significant adjustments for restructuring expenses to arrive at the adj. EBITDA figure).

Risks To ZIMV

In my opinion, the biggest risk with the ZIMV story is a lack of growth. While the company has talked up big plans to return the dental business to growth by expanding market opportunities in new geographies and increasing innovation (Figure 10), so far, the dental business’ top line has seen low-single-digit (“LSD”) annual declines.

Figure 10 – ZIMV has lofty goals to return dental business to growth (ZIMV investor presentation)

Furthermore, although ZIMV has bought itself some time by selling the spine business, the remaining debt burden is not immaterial. With pro-forma net debt of $168 million, the company still has a net debt/adj. EBITDA ratio of 2.7x (Figure 11).

Figure 11 – ZIMV has pro-forma $168 million in net debt (ZIMV investor presentation)

Conclusion

It appears I was too hasty in upgrading ZIMV to a buy in December. After analyzing the company’s recent Q1/24 financial results, I have turned more cautious on ZIMV’s valuation, as the company appears fairly valued at ~10x Fwd EV/adj. EBITDA. I am particularly worried by the continued decline in sales in the dental business.

Although ZIMV has bought itself some breathing room with the sale of the spine business, the margin of error in turning around the dental business remains small, as the remaining debt load remains substantial. I am downgrading ZIMV to a hold until I see more signs of a turnaround in topline sales.

Read the full article here