Investment summary

My recommendation for ZoomInfo Technologies (NASDAQ:ZI) is a sell rating, as I have a negative outlook for growth in the near term due to the macro backdrop that is causing weakness in growth. ZI’s relative valuation to other peers that are facing similar growth weaknesses is also expensive, which I don’t think makes sense. As ZI continues to show growth weakness, I believe valuation will rerate further downward to peers’ levels.

Business Overview

ZI is a leading go-to-market platform provider for sales and marketing professionals to better understand customers and prospects. Essentially, businesses use ZI’s platform to search for personal contact information and company profiles so that they can reach out to them. In other words, ZI helps with lead generation and marketing research. Segment-wise, ZI reports subscription revenue (99% of total revenue) and the remaining from usage-based revenue and other revenue. Geography-wise, ZI serves global customers but has the majority of revenue originating from the United States (87% as of FY23).

ZI

1Q24 results update

Giving a brief update on ZI’s recent financials, released on 7th May, ZI reported total 1Q24 revenue of $310.1 million (3.1% growth), a decline from the 5% y/y growth seen in 4Q23. Gross margins expanded by 20bps to 89.9%, which led to non-GAAP operating margins expanding by 90bps to 38.5%. However, lower tax benefits in 1Q24 led to EPS coming flattish vs. 1Q23 at $0.27 vs. $0.25. ZI ended the quarter with a total gross debt of $1.23 billion and cash (including STI) of around $440 million, netting off a net debt position of ~$791 million.

Very negative outlook ahead for ZI

I have a negative outlook for ZI, as the macro backdrop remains unfavorable for the company. At a high level, the lack of hiring strength in the US economy is going to continue weighing on ZI’s ability to reaccelerate growth. There are two key indicators that proved my point: Job openings dropped to a 3-year low in March, and large tech companies (ZI has 30+% exposure as mentioned in the 2Q23 earnings call) have continued to cut jobs in 2024. These are not indicators that point to a recovery ahead.

The prevailing bull case is that the Fed will cut rates, which will spur a macro-recovery, leading to more hiring as the cost of capital comes down for businesses. However, I think the bull case is gradually losing ground over the near-to-midterm.

- Inflation rates proved to be a lot stickier than expected.

- The US housing undersupply situation is unlikely to see a resolution in the near term, which is going to continue putting upward pressure on CPI if rates get cut (i.e., mortgage rates come down, leading to an increase in demand for housing, which then pushes up CPI).

- The US economy appears to remain strong, and this gives little reason for the Fed to cut rates.

The pressure on the ZI customer base is clearly evident when we look at the renewal rate. In the 4Q23 and 1Q24 quarters (typical season for renewals), ZI only managed to retain about 85 (in 1Q24) to 87% (4Q23) of multi-year and SMB renewals (on a net revenue retention basis). This shows that either customers are sizing down in large magnitudes or they are just churning away from ZI’s platform. Neither of them is positive. At the microlevel, conditions certainly have not shown any improvement. In a recent tech conference held just 10 days ago, management noted ongoing noise and volatility in the SMB segment and that hiring is not back universally.

As it relates to net revenue retention, in the quarter, our SMB business continued to be challenged and performed worse than prior periods. 1Q24 earnings call

I simply don’t see any visible catalysts that could turn things around in the near term for this set of customer bases (i.e., the NRR for this customer cohort is likely to just stay at ~85–87%), and this is going to put a lot of pressure on ZI to find new customers to achieve its FY24 guide (1.6% implied revenue growth at the midpoint).

ZI’s relative valuation is expensive

Redfox Capital Ideas Redfox Capital Ideas

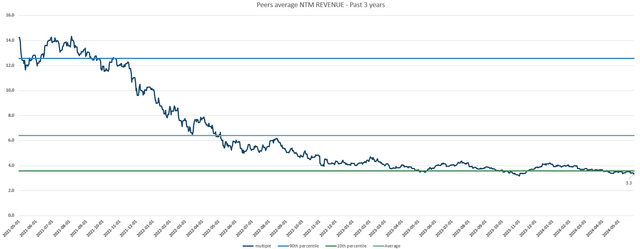

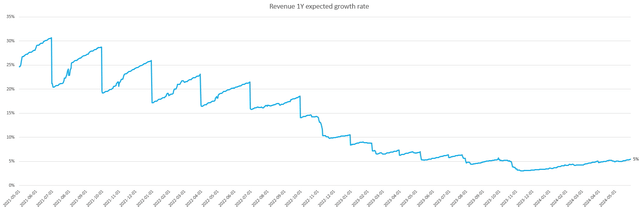

The main reason I am giving a sell rating to ZI is because its valuation relative to other peers (exposed to macro-hiring strength) is expensive. Such peers include: TechTarget, Definitive Healthcare, Dropbox, Five9 Inc., Dun & Bradstreet Holdings, Zoom Video Communication, RingCentral, Twilio, and Robert Half Inc. The reason for using this set of peers is because they are all expected to see growth slowdown (as per the charts below), and they trade at around 3.3x next twelve months [NTM] revenue with expectations for ~5% NTM revenue growth. On the other hand, ZI, which is expected to grow low single-digits (the FY24 guide implies 1.6%), is trading at a 32% premium (4.4x forward revenue) to these peers, and this does not make sense to me.

In my opinion, the market is pricing in a premium because they are expecting a rate cut in the coming months that will reignite growth for ZI, and I don’t think that is going to be the case. As ZI continues to report weak results, I expect valuation to trade down to where peers are trading today (or even lower since expected growth is lower). We have seen the market do this once when ZI announced its 1Q24 results: valuation fell from ~6x to 4.2x, a 30% drop. Suppose ZI were to trade down from the current 4.4x to peers’ level of 3.3x (of FY24 revenue), that implies an enterprise value of ~$4.16 billion, which equates to a market cap of ~$3.4 billion (a share price target of around $9).

Risk

ZI’s CoPilot product could drive more growth than expected. The product is an AI-powered product that leverages GTM data to provide sellers with insights and automate workflows. I believe the product has a pretty strong value proposition, as on average, users reduced time spent on account research and manual tasks by 10 hours per week, and Copilot users created nearly twice as many opportunities compared to nonusers. As such, ZI could see strong upsell traction and also use this to acquire customers that it couldn’t previously.

Conclusion

My view for ZI is a sell rating given the weak growth prospects and relatively expensive valuation. The current macroeconomic climate, particularly the lack of hiring in the US, is going to continue weighing on ZI’s ability to re-accelerate growth. This is evident in declining renewal rates and management’s recent comments. Additionally, ZI’s valuation is expensive compared to peers facing similar headwinds. Considering the risk of further valuation decline, I recommend a sell rating.

Read the full article here