Business Development Companies (BIZD) like Ares Capital Corp (NASDAQ:ARCC) and BlackRock Capital Investment Corporation (NASDAQ:BKCC) generate stable, defensive, cashflows thanks to owning well-diversified and conservatively underwritten portfolios of senior-secured loans. When combined with the 90%+ of taxable income payout requirement for BDCs, ARCC and BKCC offer investors very attractive 10%+ dividend yields that also appear to be quite sustainable at the moment.

In this article, we will compare ARCC and BKCC side by side and share three reasons why BKCC may outperform ARCC moving forward.

Reason #1: More Conservative Investment Portfolio

While both ARCC and BKCC have pretty conservatively positioned portfolios with good underwriting performance, BKCC’s portfolio is better positioned to weather an economic downturn.

Overall portfolio debt exposure for ARCC is 81.5% whereas BKCC’s is a whopping 98.1%. 64.4% of ARCC’s portfolio is invested in senior secured (first and second lien) loans, and 94.2% of BKCC’s is invested in the same. 41.1% of ARCC’s portfolio is invested in first lien loans and 23.3% is invested in second lien. 81.5% of BKCC’s portfolio is invested in first lien loans and 12.8% is invested in second lien loans, making its portfolio much more conservatively positioned. Outside of ARCC’s senior secured debt positions, it has only 7.9% in unsecured/subordinated debt and the remaining 27.4% of the portfolio is invested in preferred and common equity investments. In contrast, BKCC has 3.5% of its portfolio invested in unsecured/subordinated debt, 0.9% held in cash, and only 1.3% invested in preferred and common equity. Both portfolios adopt similar sector allocation, with their largest two sectors being software and financial services.

What this means is that ARCC is much better positioned to thrive during economic expansions, whereas BKCC is positioned to outperform during economic contractions.

Despite ARCC’s more aggressive disposition, however, its non-accruals are at a very low 1.3% of fair value while BKCC’s non-accruals are at a very reasonable – though higher – 2.7%. However, it is important to keep in mind that BKCC’s non-accruals are declining rapidly, falling from 4.4% to 2.7% year-over-year as management continues to make efforts to improve their portfolio’s construction.

Both businesses benefit from the fact that they are managed by very large asset managers. BKCC’s manager – BlackRock (BLK) – is the world’s largest asset manager, giving them definite economic data and scale advantages. However, BLK primarily works with publicly traded funds, so it is not quite as much of a specialist in direct lending and private credit. In contrast, ARCC benefits from a relationship with a leading alternative asset manager – Ares Management (ARES) – that has a large and deeply experienced credit platform.

As a result, we do feel that ARCC has a bit more of a competitive advantage in terms of underwriting skill and direct lending experience. However, in the current macroeconomic environment, BKCC’s far more conservatively positioned portfolio gives it the edge. Moreover, both funds have very similar expense ratios, so that is not a major factor in this comparison.

Reason #2: Significantly Lower Leverage

Both businesses have strong balance sheets with moderate to low leverage ratios. However, BKCC’s leverage ratio is much lower than ARCC’s. ARCC’s leverage ratio as of the end of Q1 was 1.09x, whereas BKCC’s was just 0.81x. What this means is that BKCC is better positioned than ARCC is to deal with deteriorating economic conditions and underwriting performance since its portfolio has less debt attached to it. Moreover, it gives BKCC much greater flexibility to invest opportunistically to create shareholder value and drive per share earnings growth since it can take on additional leverage to buy back stock at a deep discount to NAV and/or invest in additional loans in an environment where underwriting terms are generally extremely attractive for BDCs.

When combining the low leverage ratio with its extremely high allocation to senior secured (particularly 1st lien) loans, BKCC is one of the most conservatively positioned publicly traded BDCs at the moment..

Reason #3: Much Stronger Total Return Potential

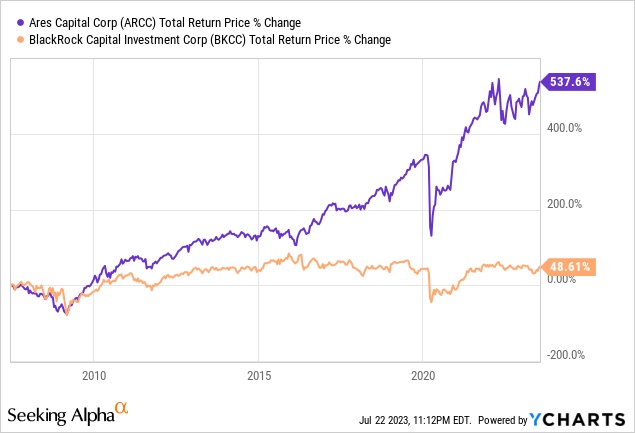

Last, but not least, BKCC has much stronger total return potential than ARCC does. Yes, ARCC has a much more impressive track record:

However, BKCC has changed a lot in recent years and is poised to continue doing so moving forward in ways that should produce a much stronger total return performance for shareholders.

While ARCC’s dividend was covered 1.24x by net investment income in its most recent quarter, BKCC’s dividend was covered by a nearly equally healthy 1.22x ratio of net investment income to dividends in its latest quarter. However, given that BKCC has much lower leverage than ARCC and plans to raise its leverage ratio to grow its net investment income per share moving forward by repurchasing shares at a steep discount to NAV and growing the loan portfolio, its effective dividend coverage ratio is actually considerably higher than ARCC’s. This makes its dividend arguably safer and/or more likely to increase.

In addition to a more attractive outlook for its dividend, BKCC also trades at a much cheaper valuation than ARCC does. While ARCC trades at a 5.8% premium to NAV, BKCC trades at a 21.54% discount to NAV. This is an enormous difference that gives BKCC a meaningfully higher dividend yield (11.56% vs. 9.84%) despite having a much lower leverage ratio. Moreover, it gives BKCC an easy way to create value for shareholders by simply buying back its stock at an incredibly steep discount to NAV.

Yes, ARCC can issue shares at a premium to NAV right now and reinvest the proceeds alongside debt in new loans. However, on a dollar-for-dollar basis, BKCC can buy back its stock on much more accretive terms than ARCC can with issuing new equity. On top of that, BKCC’s leverage ratio is low enough that it does not need to issue new equity right now to fund loan portfolio growth. BKCC can merely increase its leverage ratio to fully fund new loans.

ARCC Stock Vs. BKCC Stock: Investor Takeaway

Both ARCC and BKCC offer investors very sustainable double-digit yields at the moment. ARCC has a vastly superior track record to BKCC and is a better underwriter of loans. However, BKCC has taken dramatic steps to improve its portfolio: increasing the number of its portfolio holdings from 27 to 121 over the course of a few years, 1st lien senior secured loans now make up 82% of the portfolio, up from 50% at year-end 2020, and 13% of its portfolio is invested in 2nd lien senior secured loans, leaving just ~5% of the portfolio invested in unsecured debt, preferreds, common equity, and options/warrants, down from 23% exposure at the end of 2020. As a result, its investment portfolio and underleveraged balance sheet position BKCC better than ARCC for the current macroeconomic headwinds we see before us. When combined with its steep discount to NAV and higher current dividend yield, it is very possible that BKCC may outperform ARCC moving forward.

That said, ARCC’s impressive track record and highly skilled management team likely make it a lower risk pick over the long-term than BKCC, which still has to prove itself and is therefore more speculative.

Read the full article here