One of the great things about a crisis, if you have capital to spare, is that you often end up with companies that don’t deserve to take a tumble experiencing the same or similar downside to what some of the companies that do deserve a hit experience. Earlier this year, when the banking crisis began, starting with the collapse of Silicon Valley Bank, pretty much every player in the space ended up falling as well. At first, the fear was that the contagion would spread, bringing down an unknown number of financial institutions. But not all of these companies deserved to take a beating. One of them that, in my opinion, was treated far too harshly by the market is Cathay General Bancorp (NASDAQ:CATY). Even though shares have been recovering since, the stock is still down 22.4% since the end of February. And when you look at the fundamental health of the company, this does seem to present an interesting buying opportunity.

A small bank worth looking at

According to the management team at Cathay General Bancorp, the company operates as a holding company of Cathay Bank, a California State chartered commercial bank. In total, the firm boasts 65 branches, with 43 of them located in California and another nine in New York. Internationally, it has only one branch location. This happens to be in Hong Kong. But on top of the branches, the company also has three representative offices. These are located in Beijing, Shanghai, and Taipei.

Cathay General Bancorp

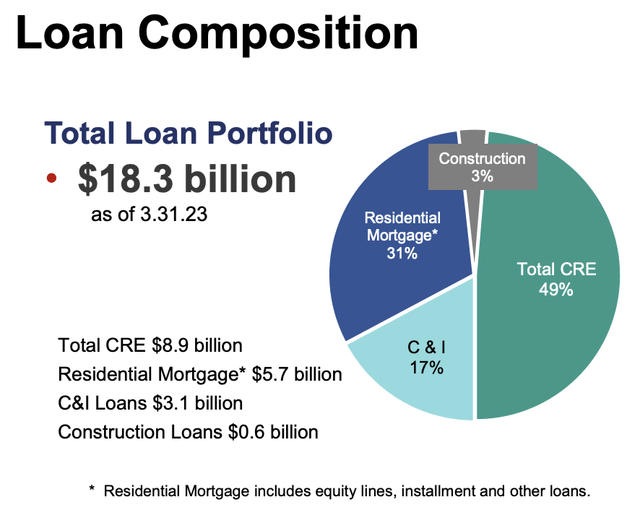

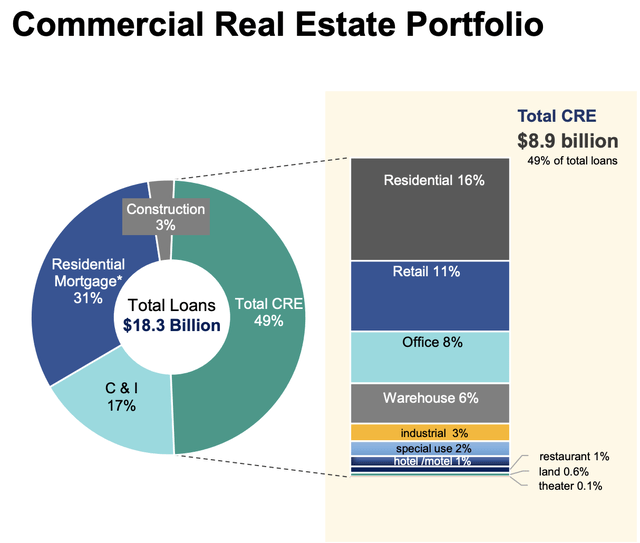

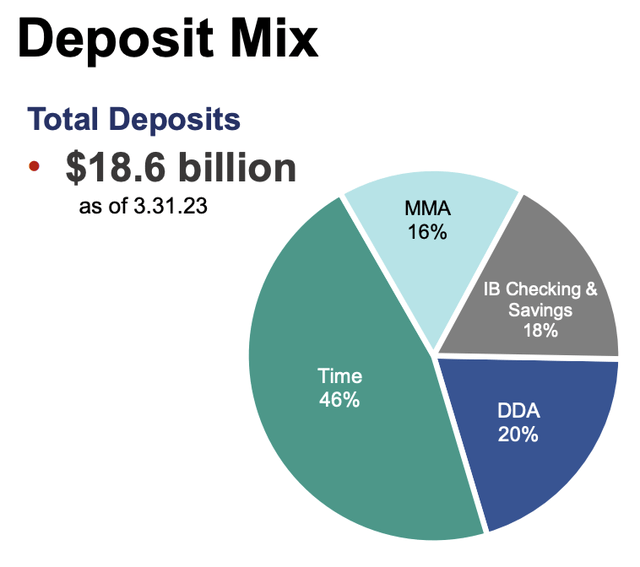

In terms of customer focus, Cathay General Bancorp tries to provide services to low income and moderate income groups in the areas in which it operates. In addition to servicing individuals, the firm also provides services for small and medium sized businesses. Of the roughly $18.3 billion worth of loans that the company has in its portfolio, 49% are classified as commercial real estate. Of these, 16% consist of residential properties, 11% involves retail properties, and office properties account for 8%. Outside of the commercial real estate space, the firm also has a significant amount of exposure to residential mortgages. 31% of its loan portfolio falls under this designation. That leaves 17% for commercial and industrial loans, and the final 3% for construction loans.

Cathay General Bancorp

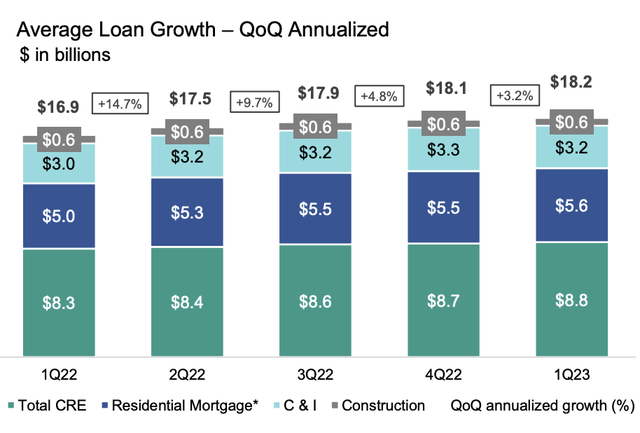

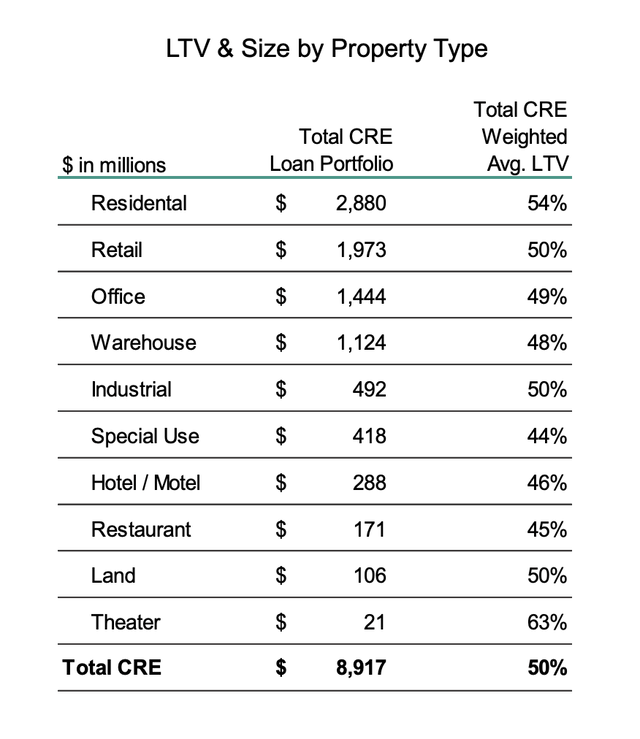

Management has done well in recent quarters to grow its loan portfolio. Back in the first quarter of 2022, for instance, the value of its loans came out to $16.9 billion. Even during these difficult times, the company seems to be doing alright. The carnage in the banking industry began in early March. So we will not see a full quarters worth of pain until the company reports second quarter earnings figures. But from the final quarter of 2022 to the first quarter of 2023, the value of its loan portfolio grew by roughly $0.1 billion. Like many investors, I am concerned about exposure to office properties. But as of the end of the most recent quarter, the office properties that it has exposure to boast a loan to value ratio of 49%.

Cathay General Bancorp Cathay General Bancorp

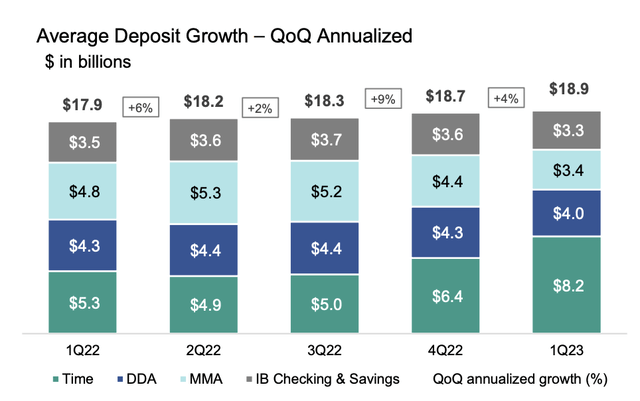

On the deposit side of things, the picture is also interesting. From the first quarter of 2022 to the final quarter of 2022, overall deposits expanded from $17.9 billion to $18.7 billion. There was considerable concern in the banking sector that banks would experience a run, fueled by concerns that high amounts of uninsured deposits would cause consumers to worry about a potential institutional collapse. In some cases, this became a self-fulfilling prophecy. However, Cathay General Bancorp actually defied these odds. Overall deposits in the first quarter of 2023 came in at $18.9 billion. That was up roughly 1% compared to the $18.7 billion that the company had at the end of 2022.

Cathay General Bancorp Cathay General Bancorp

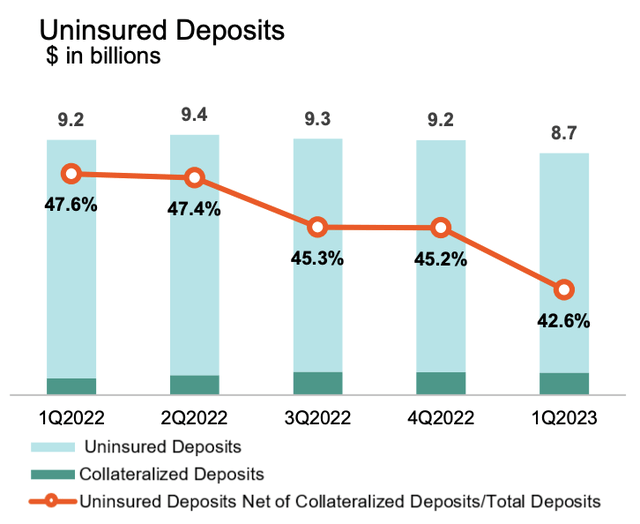

Naturally, we do need to dig a bit deeper than this. While the company did see some deposit growth during that time, it is still important to note that $8.74 billion of its deposits are classified as uninsured. This is down from the $9.2 billion reported one quarter earlier. And it translates to 42.6% of overall deposits being uninsured. This is a number that’s higher than I would like. But it definitely could be worse. The great thing about this, however, is that the company does have a great deal of liquidity to work with. Cash and cash equivalents totaled $1.13 billion at the end of the first quarter. Available for sale securities accounted for another $1.54 billion. In addition to this, unused FHLB (Federal Home Loan Bank) comes out to $6.55 billion, while unpledged securities amount to another $1.40 billion. Speaking of borrowings, total debt for the company at the end of the most recent quarter was only $501.6 million. This was actually down slightly from the $626.7 million the company had at the end of last year.

Cathay General Bancorp

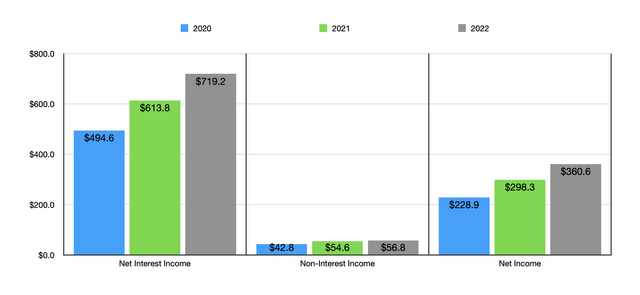

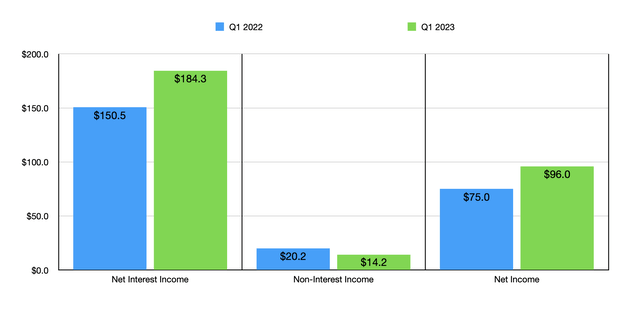

Financially speaking, the picture for shareholders has been looking up in recent years. From 2020 through 2022, net interest income for the business expanded from $494.6 million to $719.2 million. Non-interest income grew from $42.8 million to $56.8 million. All of this allowed net profits for the company to expand from $228.9 million to $360.6 million. For the first quarter of 2023, the overall picture for the company is also looking up. While non-interest income managed to dip from $20.2 million to $14.2 million, this was more than made-up for by net interest income expanding from $150.5 million to $184.3 million. This allowed net profits for the company to grow from $75 million to $96 million.

Author – SEC EDGAR Data Author – SEC EDGAR Data

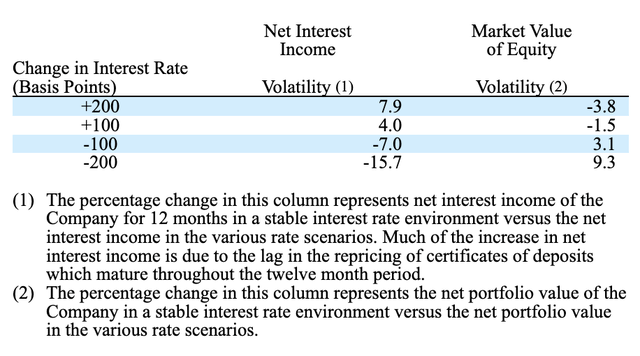

Naturally, the larger amounts of deposits and loans were partially responsible, perhaps even largely responsible, for this growth. But there’s no denying that higher interest rates are also proving to be helpful. According to a sensitivity analysis that management reported, a 1% increase in interest rates would push net interest income for the company up by roughly 4%. Unfortunately, the asset values of the company would decline by roughly 1.5% in this case. But that is a small price to pay for higher revenue that would be, by definition, high margin. Unfortunately, the opposite here is also true. For those who think interest rates are going to be dropping soon, Cathay General Bancorp may not be the best prospect to consider. A 1% decline in interest rates would push net interest income down by 7%, while a 2% decline would impact it negatively by 15.7%.

Cathay General Bancorp

Takeaway

All things considered, Cathay General Bancorp looks to be a stable company that has a bright future. The firm has demonstrated continued growth, even during these difficult times. I don’t like how much of its deposit base is uninsured. But so far, depositors have not seemed to care. Debt is low and the overall trajectory of the company has been positive. On top of this, shares are currently trading at 6.5 times last year’s earnings. And with this year looking to be even better, the stock truly does look cheap. For all of these reasons, I have no problem rating the company a ‘buy’ at this time.

Read the full article here