City Office REIT (NYSE:CIO) is a pure-play Sun Belt office equity REIT owning 60 office buildings with a total of approximately 5.9 million square feet of net rentable area. Tampa, Phoenix, and Denver account for roughly 50% of the net rentable area. The remaining half of the area is split among 7 states (e.g., Dallas, Orlando, Portland, Raleigh, San Diego, and Seattle).

As with most office REITs, CIO has also suffered from the surging interest rates, work-from-home dynamics and the corresponding imbalance between the supply and demand.

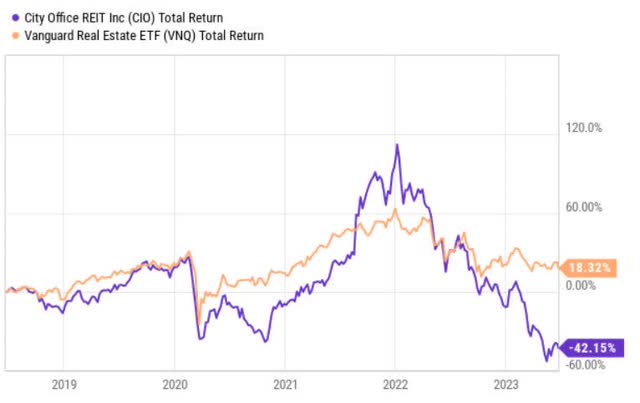

YCharts

The chart above captures the typical office story perfectly:

- Before the outbreak of COVID-19, office REITs performed more or less in line with the overall REIT market. Obviously, there were some clear winners and laggards as well, but on average the entire office U.S. equity REIT segment moved in tandem with other REITs.

- In early 2022, when the consequences of the pandemic started to kick in, office REITs fell sharply suffering greater losses than their peers placed in different segments of the commercial real estate market.

- In mid-2021, when the COVID-19 abated and employees could finally return to ‘business as usual’, there was a massive rebound exhibited by most office REITs.

- Approximately, half year later, the Fed began to take drastic measures to contain inflation by significantly increasing the Fed Funds rate. As a result, almost all office REITs nosedived again because of the clear challenges to maintain FFO levels and occupancy rates from structurally declining demand for office space.

CIO is no exception here and currently is facing the same issues as many of its peers.

Now, I am certainly not predicting that conditions in office markets will normalize any time soon or that CIO will rebound as it did back in mid-2021 due to the suddenly reversed trajectory of future Fed Funds rates. In fact, I am concerned about CIO’s ability to avoid unfavourable equity issuance to comply with its debt covenants.

However, my thesis lies in the preferred stock of City Office REIT (NYSE:CIO.PA), which currently yields 9.7% and, in my humble opinion, embodies risk-reward characteristics.

Why CIO equity might not be a wise choice

Whenever a stock price collapses in a similar magnitude as CIO has experienced in the past year (i.e., dropping by ~60%), it is clear that the market is pricing in something very bad.

Besides the aforementioned and the obvious structural headwinds, CIO’s case carries some additional risks, which are of a high probability and severe impact.

1. Aggressively leveraged balance sheet

CIO has rather high debt ratio compared to its sector peers. As of now, the debt ratio of CIO stands at 77%, which is 11% above the sector average. On a stand-alone basis, anything above 70% seems already aggressive from the financial risk perspective. The annualized (based on Q1, 2023 figures) net debt to EBITDA stands at 6.5x, which again is higher than in the sector and indicates risky conditions in the context of the prevailing headwinds.

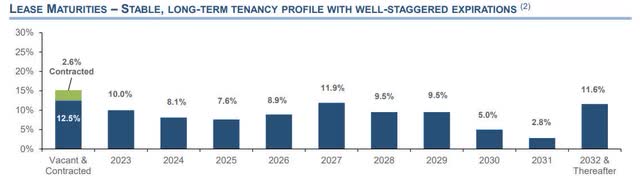

2. Unfavourable structure of lease maturities

In times like these when supply dwarfs demand and the bargaining power sitting at the tenants’ hands, it is a must to have well-laddered lease maturities stretched far in the future.

CIO Investor Relations

In the CIO’s case, there is a notable chunk of lease maturities coming due in 2023 and 2024. It will be a massive challenge for CIO to not only keep the current rent/lease levels, but also to motivate existing tenants to stay (or attract new ones).

Unfortunately, looking at the most recent history, 4 of 5 quarterly results were characterized by negative like-for-like performance and steadily decreasing occupancy rate. This just shows how hard it is to renegotiate expiring leases, and how unfortunate it is to have meaningful portions maturing in the foreseeable future.

3. Negative effects from further convergence in the cost of financing

Looking at the most recent debt financing activities of CIO, we can see that there is some traction in the lending provided where the cost of debt is around 6.5 – 7%.

Now, if we contextualize this with the two followings facts:

- The current weighted average cost of financing for CIO is 4.5%, implying that there is still some 200 – 250 basis points of pain.

- The weighted average maturity is 3 years, which means that the convergence will be relatively quick as major refinancing activities are really around the corner.

Any uptick in the weighted average cost of financing will impose further pressure on the CIO’s ability to protect the current FFO generation, especially considering the relatively indebted balance sheet and major challenges from deteriorating business performance metrics (e.g., occupancy rates, operating margins, rent levels).

All this in combination with the systematic impediments associated with ‘higher-for-longer’ environment and ‘work-from-home’ dynamics make it very difficult to hold or recommend CIO’s equity.

Why CIO’s preferred shares offer value

Looking at the aforementioned aspects, it might seem that CIO is set to experience massive pain going forward, and thus no exposure shall be opened against the Company.

While I agree that such conclusion is well-substantiated for the CIO’s equity, but I do not think that the CIO’s preferred shares are exposed to the same level of risk. Put differently, the currently offered yield of CIO’s preferred shares (~9.7%) is sufficient to compensate for the underlying risks. Moreover, in my opinion, these preferred stocks provide even some solid upside potential from the capital appreciation front.

For any preferred stock investor, it is of utmost importance to make sure that the Company does not halt preferred distributions and more importantly does not initiate a restructuring process in which usually preferred stock owners get massively diluted.

So, here are the most important considerations, which make me comfortable in safely clipping the 9.7% coupon going forward.

1. Ample liquidity

As of March 31, 2023, the company had $52 million of cash and about $100 million of undrawn availability on the revolving line of credit. This liquidity is sufficient to refinance all the maturing debt until 2024 (including).

The credit facility itself has a maturity in 2025, but if an extension fee is provided, it can be extended by one year until November 2026.

Ultimately, this means that CIO has the luxury to not worry about any refinancing risk until late 2026. In practice, CIO will utilize part of its undistributed FFO to bring down debt, thereby reducing the reliance on the external liquidity.

2. Strong cash retention

Early in May 2023, CIO slashed its dividend by 50% to protect its capital structure and de-lever.

As a result, CIO now is able to retain ~$11 million of cash in its business on a quarterly basis. This is more than enough to pay down all of the maturing debt in 2023 and a notable chunk of 2024 debt, thus reducing the need to rely on the revolving facility.

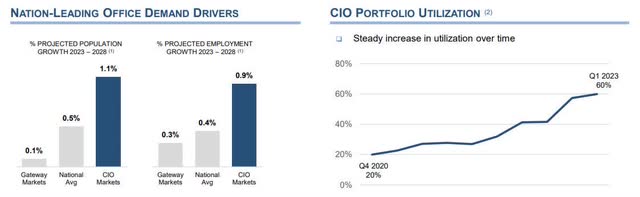

3. Q1, 2023 showing some signs of resiliency

The most recent quarterly performance by CIO finally broke the negative trend in negative rate of change in the like-for-like rate figures. In Q1, CIO was able to find new tenants and partially negotiate with the existing ones, which ultimately lead to improved NOI of 3% and by ~1.5% higher occupancy rate.

CIO Investor Relations

Overall, CIO is more resilient relative to an average office REIT given the following:

- The lion’s share of the portfolio is Class A, which is critical against the backdrop of unfavourable supply and demand circumstances.

- All the CIO offices are located in the Sun Belt markets, which are capitalizing on labor force migration and corporate relocations.

- CIO enjoyed 99%+ rental collections throughout the pandemic.

The Q1, 2023 figures and rapidly recovering CIO utilization levels from Q4, 2020 confirm the underlying resiliency.

In closing

The market is pricing in a $1.39 FFO per share of 2023, which is at the very lower end of the CIO’s guidance. It also implies that the ensuing quarters will be characterized by negative like-for-like performance or if positive then completely offset by the surging interest costs and other inflationary factors.

Moreover, FFO per share consensus estimate for 2024 indicates a further decline of ~5%. All this goes hand in hand with the unfavourable lease maturities and rising interest rate costs. Hence, I do not see CIO’s equity as a solid and predictable spot to allocate capital in.

Nevertheless, it is a completely different story for CIO’s preferred shares. Looking at CIO’s fundamentals, we can see that there is ample liquidity and cash generation to refinance and survive the office crisis. Even if CIO delivered materially weaker FFO figures, there would still be room for CIO to refinance and avoid restructuring. In worsening situation, CIO has still the option to reduce distributions, thus saving additional ~$20 million per annum. This would destroy the equity but not the preferred shares.

Finally, the preferred share investors could not only count on 9.7% coupons, but also on gains from the capital appreciation. The fact that CIO carries class A properties in combination with sufficient cash generation, which certainly allows to avoid restructuring and preferred dividend cuts, awards preferred share investors with an exposure to major capital gains. The key catalysts for this could be decreasing Fed Funds rate (as preferred instruments embody notable duration) and normalization in the office space.

Read the full article here