Following the latest news on Covestro (OTCPK:CVVTF)(OTCPK:COVTY), it is essential to review our latest investment thesis and comment on the potential acquisition from Abu Dhabi National Oil Company (ADNOC). Before commenting on Covestro, we should say that Germany no longer runs. Indeed, its economy is slowing down and is now in a technical recession; in detail, GDP fell into negative territory in the last two quarters.

In Q1 2023, the fall was 0.3%, after a minus 0.5% in 2022 last quarter. The German slowdown has contributed to sending the whole Eurozone into a recession. However, these are not deep red numbers, but it is not only consumer spending suffering; industrial production is also declining, with new orders decelerating. The grip-tightening German industry, more than others, was the substantial increase in energy costs and raw materials, only partially discharged on sales prices.

In this environment, we shouldn’t be surprised to see potential offers to buy discount companies. Starting with our latest article called: “Darkest Hours Have Passed,” we set a Covestro target price at €48/share (in line with today’s stock trading price); however, looking at our initiation of coverage, one of Mare Evidence Lab’s key points was the company’s asset replacement cost analysis.

Mare past analysis

ADNOC offer

Cross-checking the latest news, it appears that Covestro rejected Abu Dhabi National Oil Co’s first offer. Here at the Lab, we believe the company wants a higher price. Looking at Bloomberg News, the German chemical player communicated to ADNOC CEO Sultan Al Jaber that “the proposed valuation does not allow for further negotiations.” But, we are confident that Covestro may be willing to re-discuss the offer with better terms. In a recent meeting, Al Jaber offered €50 per share, valuing the company at almost €11 billion against a current market capitalization of €9.4 billion, implying a 15% upside.

Turning down the first offer is not unusual, and ADNOC will now evaluate its next moves. The Abu Dhabi National Oil Company wants to transform and diversify its downstream businesses. According to Goldman Sachs, Covestro replacement assets could be valued at around €13.9 billion, even without considering the potential synergies for a strategic buyer. The company’s current product portfolio offers access to diversified end markets, including EV and thermal insulation, with an ability to generate sustainable cash flow.

As a reminder, in 2019, Covestro launched a strategic program that includes a circular economy in all areas, planning to allocate 80% of R&D investments to projects capable of contributing to achieving the 17 sustainable development goals defined by the UN. However, we believe that Covestro will help ADNOC reduce its long-term oil and gas exposure. Still, synergies would be limited as ADNOC is not a large producer of critical raw materials for Covestro. Significant cost savings are unlikely to be realized through manufacturing or logistical overlaps.

Conclusion and Valuation

In our last publication, we increased the company’s EBITDA growth by 6.5% for the next three-year period with a gradual recovery to mid-cycle margin. Our target price was derived from 1) higher capacity utilization rates thanks to competitor shutdown announcements (BASF recently declared a 300kt closure), 2) a decrease in spotted energy price, and 3) a gradual volume recovery in APAC.

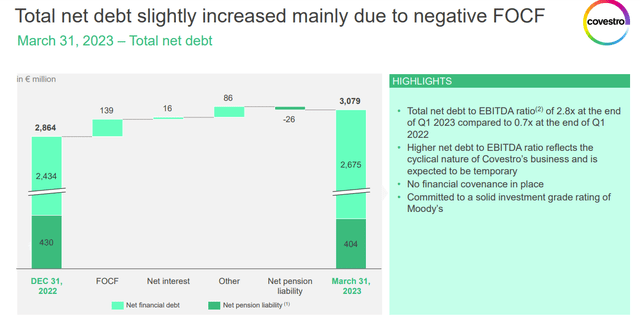

In addition, we were favorable pricing in 1) WC efficiency, 2) a new cost-saving target, and 3) an ongoing buyback. Here at the Lab, we are not speculating on M&A rumors directly linked to Covestro’s stock price development. On a twelve-month forward EV/EBITDA, Covestro is now fully priced in, given the company’s FCF is negligible for 2023, as also anticipated by the company (Fig 1). From a historical perspective, the company has always traded in the 5-6x range at EV/EBITDA, an offer over €60 per share could represent a valuation at an almost double-digit rate, including Covestro’s total debt and pension liabilities at nearly €3 billion (Fig 2).

Therefore, we continue to rate the company with a neutral rating at a target price of €48/share. Despite that, we are confident that Covestro’s structural cash flow generation profile will be improved thanks to management’s decision to lower the CAPEX investment, “No More Dividend,” and halt the share repurchase program. Our downside risks include an economic downturn across the Covestro portfolio, especially in the polycarbonates and polyurethanes division, overcapacity at the industrial level, energy price development, and significant changes in currency evolution.

Covestro FOCF development

Fig 1

Covestro’s total debt and pension liabilities

Fig 2

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here