Co-produced by Austin Rogers

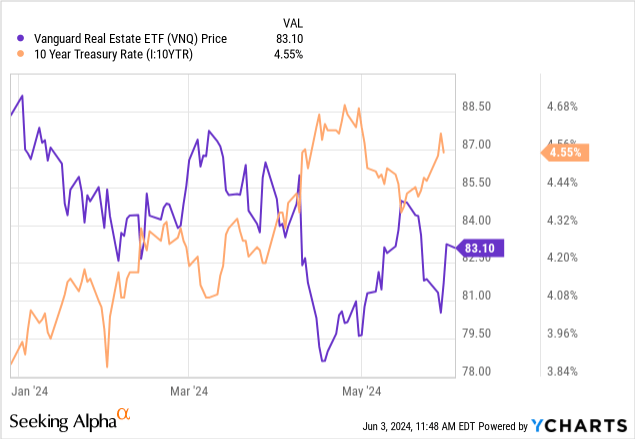

I have pointed out multiple times how frustratingly mechanical the relationship has recently been between the public real estate sector (VNQ) and bonds, specifically the 10-year Treasury.

The index as a whole has traded in a mirror opposite pattern:

10-year up, REITs down. 10-year down, REITs up.

The correlation has been extremely strong over the short run as if nothing else matters.

That’s annoying because, other than certain thematic sectors like data centers (DLR, IRM) and top-tier senior housing (WELL, CTRE), REITs simply aren’t being rewarded for strong fundamentals at the moment. The weak ones are certainly being punished, but most of the strong ones aren’t being rewarded.

Therefore, many investors are concluding that REITs are just a bet on lower interest rates, and it has certainly felt that way lately.

But the positive side of this mispricing is that it provides an opportunity to buy high-quality REITs at a big discount to their historical valuations.

Not all REITs are at the mercy of the Fed. Most of them use little leverage and continue to enjoy strong growth prospects, and yet, they are now heavily discounted.

Generally speaking, I think that the higher the REIT’s growth prospects, the more likely it is that the market will eventually reward it with stock price appreciation, even if interest rates remain range bound for a while.

That’s why I am so focused on high-quality, low-leveraged REITs with strong growth prospects. Here are three REITs that we expect to win, no matter what happens to interest rates:

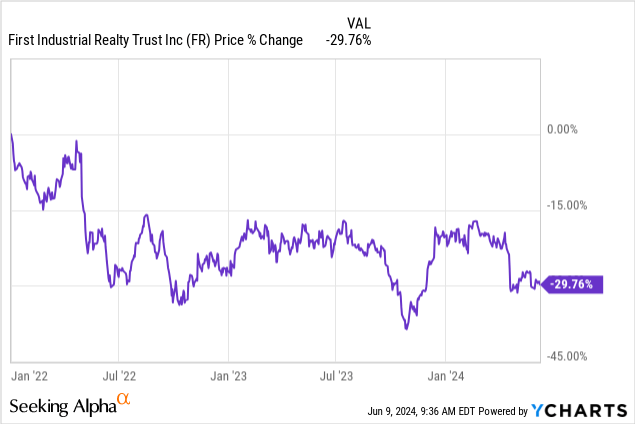

First Industrial Realty Trust (FR)

FR is probably my favorite US Industrial REIT right now.

First Industrial Realty Trust

It owns some of the best properties in its group, focusing on Tier 1 properties in supply-constrained markets. Today, its rents are deeply below market, which provides it a “bank of growth”, it has little debt with a low 23% LTV, and it has strong long-term growth prospects.

Despite that, it is down 30% since 2022 even as its cash flow grew by 20% and as a result, its FFO multiple has now been cut in half:

It is quite literally priced at its lowest valuation since the great financial crisis.

18x FFO may not seem that low, but this is a REIT that typically trades at closer to 30x FFO because of its strong growth prospects:

- Its rents are deeply below market and as its leases gradually expire, FR is able to hike its rents by 50%+.

- It owns a massive land bank, and it is in the process of developing a lot of properties, which is costing it a lot of money, but not earning any rental income yet. Historically, it has managed to earn strong 7%+ initial yields on its development projects.

First Industrial Realty Trust

If you adjust for those two things, the 18x based on today’s cash flows is actually very low. Within 3-4 years from now, it will be in the low 10s unless its cash share price rises to higher levels. Its implied cap rate will then also be in the low 8s, which makes no sense whatsoever for such a high-quality industrial REIT.

Therefore, I think that it is much more likely that its share price will adjust higher, even if interest rates remain at today’s levels.

Big Yellow Group (OTCPK:BYLOF / BYG)

BYG is one of my biggest European REIT investments, and I like it so much because:

- It is heavily discounted.

- It uses little debt.

- It owns amazing assets and has a big growth pipeline.

- It has managed to grow its FFO per share by 10%+ annually for the past 20 years.

- And I think that it can keep it up for the next decade to come.

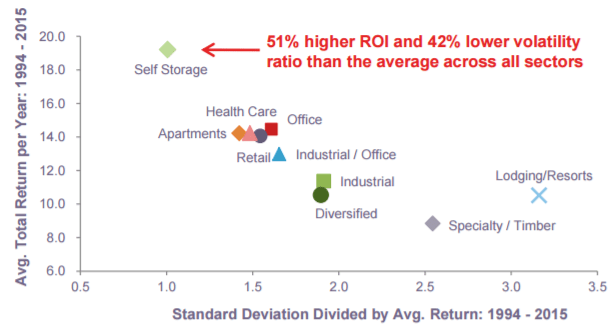

The secret to its rapid growth is that it focuses on an undersupplied market that’s growing in demand, and that is self storage in Europe.

Self storage was by far the most rewarding property sector in the US in the past 30 years because it was rapidly growing in demand and REITs were able to build new facilities at high spreads over their cost of capital:

National Storage Affiliates

Big Yellow Group

But US self storage is now overbuilt and most opportunities have been exhausted.

But the UK self storage market is still 20 years behind and BYG is capitalizing on this opportunity by building new storage facilities, earning a high initial yield of ~8-10%, resulting in a big spread over its cost of capital that then expands its FFO and dividend per share.

The long-term outlook is very bright, but the shares of the company have dropped by 30% since the beginning of 2022 even as it grew its cash flow by another 20% during the same time period. As such, it is now 2x cheaper than it was just two years ago.

Corporacion Immobiliaria Vesta (VTMX):

VTMX is a new investment for us.

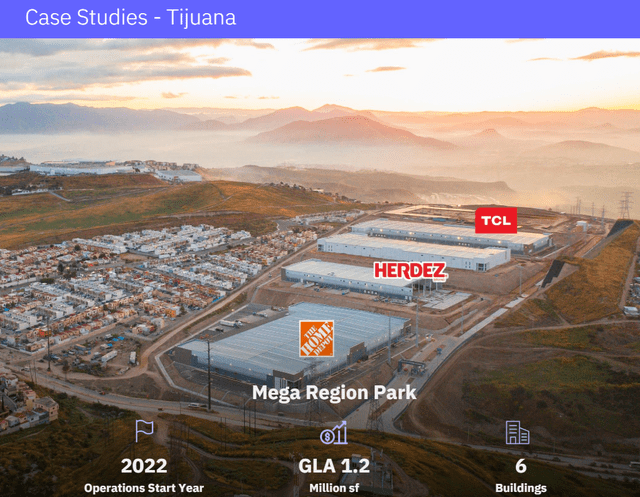

It is the only Mexican REIT that’s listed on the New Year Stock Exchange. It specializes in industrial properties, and it has its hands full right now.

Mexico is rapidly replacing China for the manufacturing of goods due to the growing trend of near-shoring. It just makes a lot more sense for American, Canadian, and European companies to produce in Mexico these days because:

- It is far closer to their end consumers, reducing transportation cost and time.

- Labor is a lot cheaper in Mexico than in China these days, reducing production cost.

- And perhaps most importantly, China is a dictatorship that’s supporting Russia’s genocidal war on Ukraine, working closely with North Korea, and threatening to invade Taiwan in the near term.

Not surprisingly, this is pushing global companies to reconfigure their supply chains, and Mexico is the big winner here.

It is leading to rapidly growing demand for industrial space in Mexico, and VTMX is here to fill this void.

Vesta REIT

Its US listing gives it a competitive advantage in raising capital at a low cost that it then reinvests at high spreads in new industrial development projects in Mexico.

Last year, it raised substantial capital at the time of its IPO, and today it is still in the process of putting all of this capital to work.

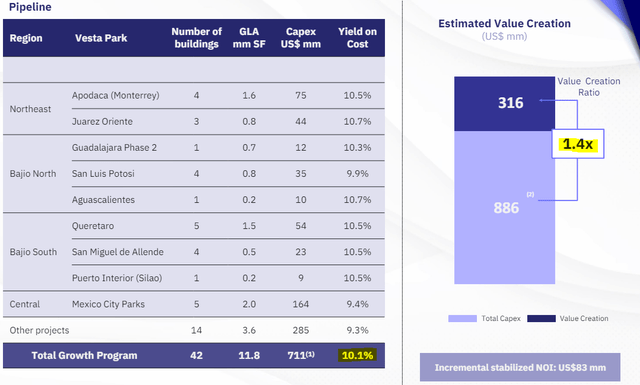

This explains why its share count increased by 27% over the past year, and why the company is also still sitting on $445 million of cash. This cash is now gradually getting invested in the following development projects, which have an expected 10.1% average initial yield:

Vesta REIT

This should create significant value for shareholders because these properties would trade at much lower cap rates if they decided to sell them in the private market. It also represents a substantial spread over their cost of capital and therefore, it should grow their FFO per share.

This year, they expect to grow their NAV per share by $3 and their FFO per share by $0.20, which is quite significant given that the company’s NAV per share is currently about $40 and its FFO per share is about $2 per share:

Vesta REIT

So fundamentally, it is doing quite a bit better than most REITs. The REIT also has little debt with a low 23% LTV, so it is not heavily impacted by the surge in interest rates.

It has a very long runway of rapid growth prospects and yet, it is today priced at just 15.5x FFO and an estimated 20% discount to its net asset value.

That may not seem that low to you, but keep in mind that just like in the case of FR, its rents are deeply below market, it owns a huge land bank that earns no cash flow today, and it has a massive pipeline of new development projects that will significantly expand its FFO and NAV per share in the coming years.

Therefore, unless its share price rises higher, its FFO multiple will be a lot lower already in a couple of years from now, and its discount to NAV will grow to a lot larger as well.

I think that a more likely outcome is that its share price will rise to reflect the significant value creation.

Closing Note:

10-year up, REITs down. 10-year down, REITs up.

The correlation has been extremely strong over the short run, as if nothing else matters. It is especially surprising given that other stock sectors known for their above-average dividend yields like utilities (XLU), consumer staples (XLP), and even regional banks (KRE) have been far less correlated with the 10-year Treasury yield.

But it has resulted in some amazing buying opportunities, and we are taking advantage of them.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here