Bargains may seem hard to come by in the pharmaceutical segment, as a number of names like Amgen (AMGN) has become pricey. Yet, there are always bargains to be found, and they don’t have to be obscure names that are not yet profitable.

This brings me to Gilead Sciences (NASDAQ:GILD), which I last covered here with a ‘Buy’ rating back in August of last year, noting its superior profitability and growth opportunities in the oncology segment. It appears that the market has agreed, as the stock has given investors a 19% total return (thanks in part to dividends) since then, far surpassing the 2% rise in the S&P 500 (SPY) over the same time.

Despite trading at a higher price compared to last year, GILD continues to trade at a low PE ratio, especially after the stock traded back down over the past 10 months, as shown below. In this piece, I highlight the company’s recent developments and discuss why GILD is a good healthcare pick for income and potential gains, so let’s dive in!

GILD Stock (Seeking Alpha)

Why GILD?

Gilead is a leading biopharmaceutical company with innovative and moat-worthy treatments for life threatening diseases such as HIV, viral hepatitis and cancer. Like most pharmaceutical companies, GILD has seen its share of ups and downs, as blockbuster drugs coming online and other drugs coming off patents.

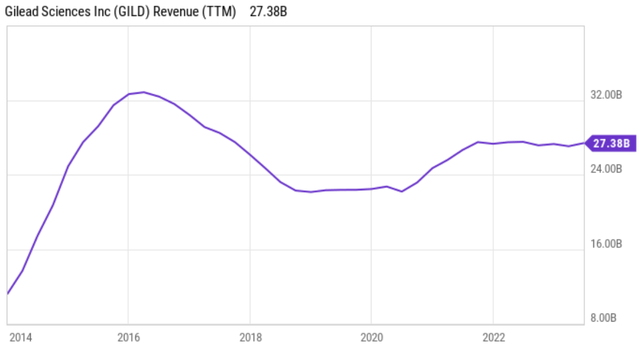

GILD saw a significant ramp up in revenue in the 2014-2016 time period, as blockbuster drugs the HCV space like Sovaldi and Harvoni came online. However, it’s struggled to continue that momentum in the years since, with revenue flatlining since recovering from a trough in the 2018-2020 timeframe, as shown below.

YCharts

GILD, however, appears ready to turn the corner with its strong pipeline of drugs, particularly in the oncology space. This is reflected by sales growing by 11% YoY (excluding Veklury aka Remdesivir, the COVID-19 treatment) to $6.3 billion. This was driven in large part to favorable pricing in GILD’s HIV drug Biktarvy growing by 17% YoY to $3.0 billion in sales, reaching $10 billion in lifetime sales, and the Oncology segment, which saw robust 38% sales growth to $728 million.

GILD’s Veklury has seen a significant slowdown due to COVID vaccines that have prevented many cases of severe disease; however, the market seems to not be giving GILD enough credit on strong execution in its HIV franchise (as noted above) and on its emerging portfolio in hematology and oncology.

This is supported by the recent announcement last month that GILD’s Trodelvy and Merck’s (MRK) cut tumor size in previously untreated non-small cell lung cancer, which is the most common form of lung cancer. The study showed that the drug combo from the antibody drug Trodelvy and immunotherapy drug Keytruda led to an encouraging 56% response rate and an 82% disease control rate. Management highlighted the fast growth rate in the oncology business and the potential around new therapeutic areas in its pipeline during last month’s global healthcare industry conference:

Last year we had around $2 billion in business on our oncology business. Through the first half of this year, we’re now on a $3 billion run rate. Our cell therapy business is growing at 27%. Trodelvy is growing at 63%. So we’ve got great confidence around the commercial execution in our programs. And that’s supplemented on the transformation side by the depth of that portfolio. Those 21 Phase III trials are playing out across our therapeutic areas.

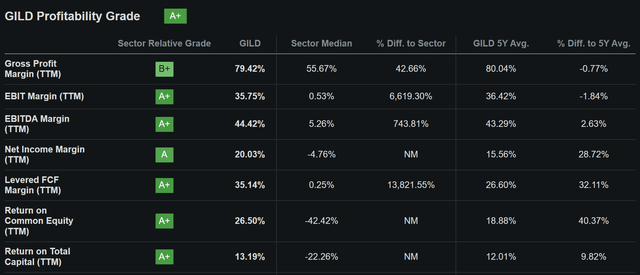

At the same time, GILD remains a cash rich enterprise, generating $9.5 billion in operating cash and $7.13 in free cash flow per share over the past 12 months. This enabled GILD to return $5.2 billion in cash to shareholders over the past 12 months, comprised of $3.8 billion in dividends, and $1.5 billion in share repurchases. GILD’s pricing power is reflected by its A+ Profitability Grade, with sector leading EBITDA and FCF margins, and Return on Equity, as shown below.

Seeking Alpha

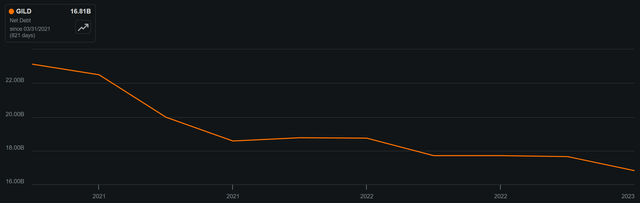

Importantly, in this high interest rate environment, GILD carries a BBB+ investment grade credit rating and has a low net debt to EBITDA ratio of 1.38x, sitting well below the 3.0x level generally considered to be safe by ratings agencies. As shown below, GILD has made steady progress in reducing its net debt balance since the start of 2021, from $23.1 billion to $16.8 billion as of the last reported quarter.

GILD Net Debt (Seeking Alpha)

This lends support to the 4.1% dividend yield, which comes with a safe 47% payout ratio and comes with a 5-year CAGR of 6% and 7 years of consecutive growth.

Risks to GILD include patent cliffs for drugs, such as the 2033 patent expiration for its blockbuster Biktarvy drug. Considering the high efficacy of this drug, GILD may have limited opportunities to improve on this drug with new research and patents. Plus, GILD’s HCV market is in decline, due to the efficacy of the drug in curing patients, and drugs in pipeline may not meet expectations through the progression of clinical trials.

Considering all the above, I view GILD as being good value at the current price of $73.27 with forward PE of 11.3. At this valuation, the market’s expectations may be too low, considering GILD’s high profitability, strong balance sheet and promising applications for new drugs and analysts forecast a respectable 9.6% EPS growth next year.

Investor Takeaway

Gilead is a solid healthcare pick for both income and potential capital gains. Its strong franchises in HIV and HCV provide hefty cash flows with which it can build up its oncology pipeline, and new indications for Trodelvy show promise. With a strong balance sheet, a well-covered and growing dividend, healthy profitability, and low valuation, GILD may just be a sound healthcare pick for investors looking for income and a place to shelter capital amidst economic volatility.

Read the full article here