Introduction: the self-storage market and SELF

Global Self Storage (NASDAQ:SELF) is a REIT that focuses on acquiring and managing self-storage properties across the US. In the last 3 years, the self-storage market experienced incredible tailwinds and attracted substantial investments globally. The two most relevant markets in terms of growth and size are the UK and the US. This is to give some perspective of how much the volume changed YoY:

U.S. self-storage transaction volume grew from $6.2 billion in 2020 to $16.8 billion in 2021, an increase of 170%, far outpacing the historical average annual transaction volume of $4.4 billion from 2010-2021, according to Real Capital Analytics and CBRE Investment Management

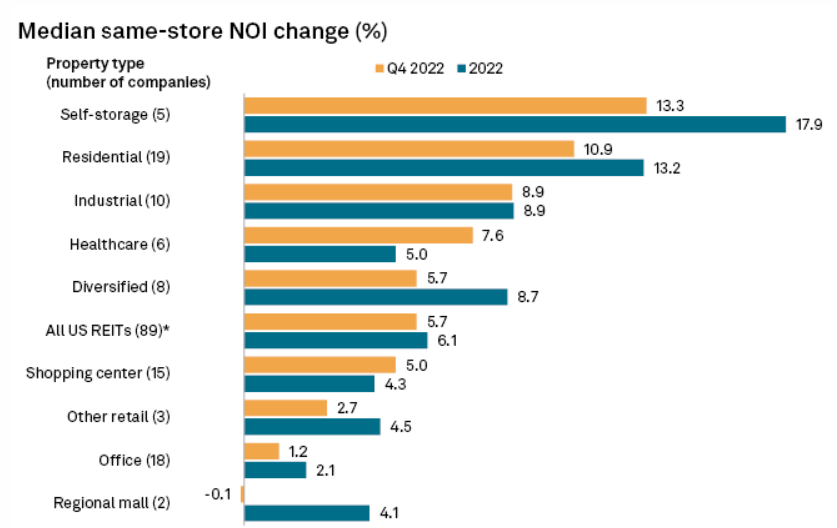

But the most important change did not occur in volume, but rather in NOI. Indeed, self-storage experienced one of the largest changes in operating income across all the other real estate classes. The trend is continued in 2022 and we believe that better-than-average performance should be expected even in a tough environment like 2023’s.

Chance in NOI YoY RE markets (S&P )

So why choose SELF as the vehicle to gain some exposure to this market? Well, we think that the company is well positioned to (1) improve its margins and grow its NOI, and (2) the limited leverage and conservative balance sheet make it resilient enough to go through the uncertain macro environment.

Past performance and future opportunities: how is SELF positioned

As the market boomed in the last years, so did SELF’s operating income. NOI went from $1.4 million in 2019 to $3.6 million in 2022, a 3 times increase in just 3 years. This was driven by margin expansion (i.e., increased efficiency and rent roll-up of the existing facilities), along with top-line growth.

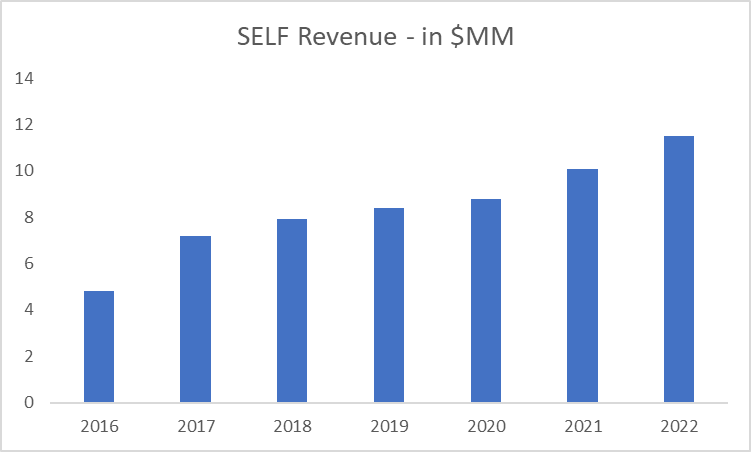

SELF – Revenue (Seeking Alpha)

This is actually how the revenues look like for the last 7 years. An amazing track record if we consider that during the same period, debt went down from $19 million to $17 million. This means that this growth was not funded with additional debt, but it is also true that some meaningful dilution took place at the same time. Weighted average shares outstanding passed from 7.7 million in 2019 to 11 million now. However, dividends per share remained unchanged, so the dilution has had no effects on the income collected by shareholders.

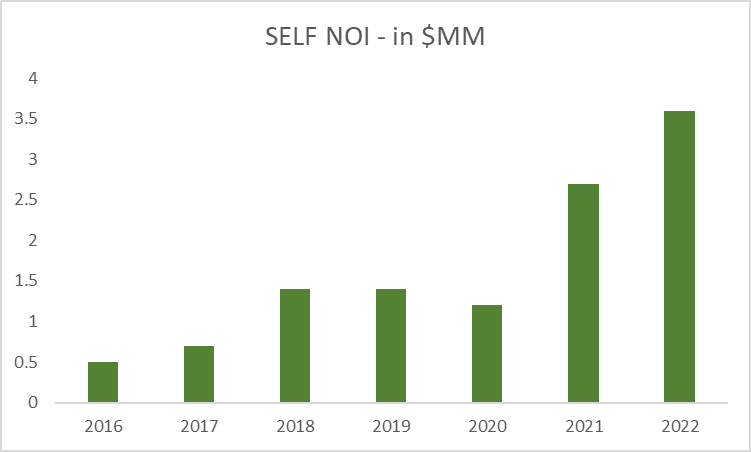

SELF – NOI (Seeking Alpha)

And this is NOI development which went ballistic from less than $0.5 million to $3.6 million. So again, sound and solid results that highlight strong execution skills as the portfolio changed little in size – PP&E went from $56 million to $66 million, roughly a 20% increase.

If we give a closer look at the balance sheet and leverage position, we can understand the other strong point in favor of SELF. The debt-to-equity ratio is only 35% and is among the most conservative in the industry (median level for the sector is 96%). The current cash sits at around $7 million, and with $17 million of outstanding debt, this means that the company has plenty of flexibility in paying dividends or deciding to pay down debt further. However, these last options wouldn’t make much sense because the current notes have a fixed interest of just 4.2% and mature in 2036. Basically SELF got one of the best credit positioning and liabilities management possible.

Management, compensation, ownership, and dividends. Everything points in the right direction

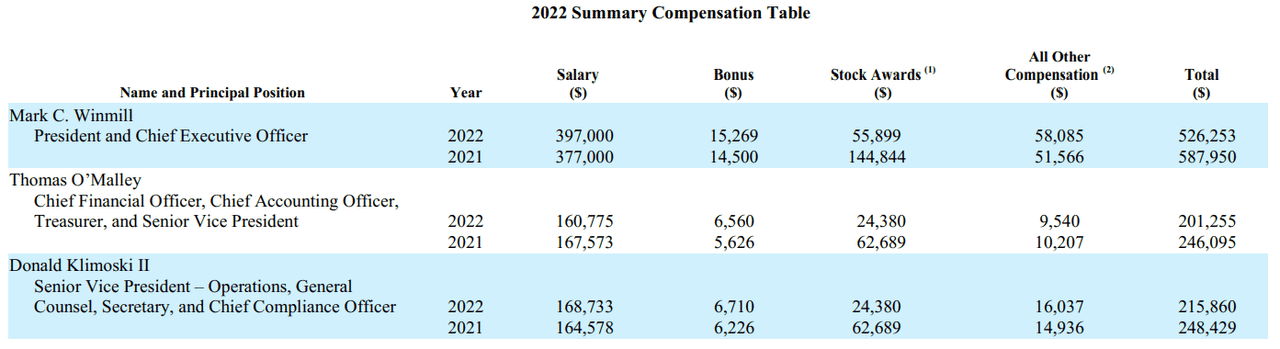

We like to focus on the financial position and prospects of the companies we analyze, but we also think that every time we take a long position we are putting ourselves in the hands of a management team. One of the things that we look at the most is the proxy filings and the data on compensation. In the case of REITs, it is very common to see management teams extracting value at the expense of shareholders for their own benefits, and even in smaller-sized companies directors are earning millions in total comp.

The case with SELF is very much compelling on this side. The CEO owns almost 2% of the company and is bringing home roughly $500k in total compensation per year. This seems reasonable given the company size of $50 million market cap and more than $10 million in revenues. The other directors are quite cheaper with compensation below $250k. Most importantly they are covering many roles (3 roles each) which makes the board and leadership team leaner and more efficient.

SELF – Management compensation (Proxy Filing – DEF14)

We like to also point out dividend safety and consistency. We think that management did a great job in risk management (look at the liabilities side), and also consistently paid out a reasonable amount of cash while also re-investing in the business.

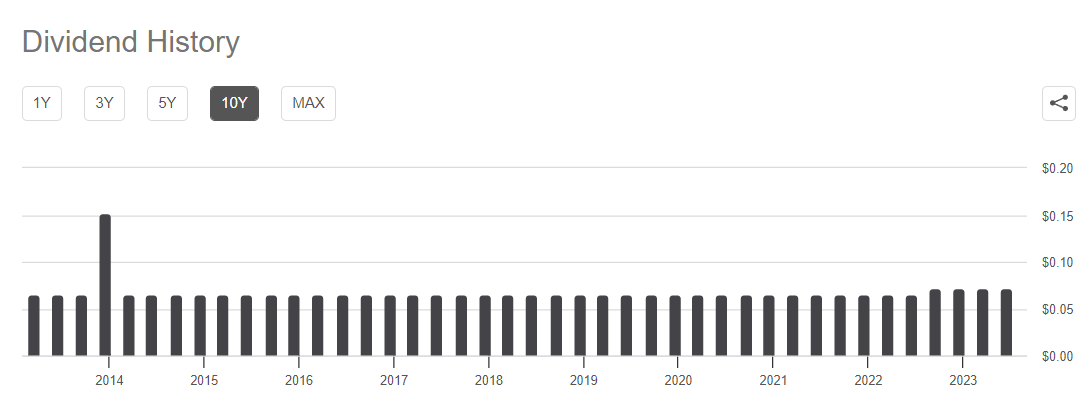

Dividend history (Seeking Alpha)

The dividend history as provided by Seeking Alpha data shows how every quarter in the last 10 years (with one exception and a small raise recently), SELF paid a $0.07 dividend. So no matter what, if you buy SELF you should expect to get your 7 cents dividend every three months. This means a lot to income-focused investors, and the risk-averse balance sheet that the company has definitely helps achieve this result.

Risks: some threats to the future of SELF

As we are discussing all the upsides, it is also important to mention what could go wrong. We are talking about real estate, so there are systemic risks related to this sector and some idiosyncratic risks related to SELF.

For the “generic” risks we mention an overall slowdown of the self-storage RE market, which grew substantially and could be hit by slower or negative growth. This is because when RE assets are developed at this speed, it is quite likely that an excess of supply generates, weighing on prices and margins.

As per the idiosyncratic risks that SELF itself may run into, we definitely have execution risk. We may provide many examples in 2021-2022 of REITs that incurred excess leverage (because of very low rates), did not hedge their exposure, entered into acquisitions too big for them, and many other managerial (deadly) mistakes. While the track record speaks highly for SELF leadership team, we can never be totally de-risked that wrong decisions that impair growth of profitability are taken.

Valuation: an exciting future and some projections to understand it

We employ a good degree of financial modeling and projection in our analyses. In the case of SELF, given the straightforward managerial approach, past results, capital structure, and the business itself we believe to have a great amount of visibility into next years’ cash flows. And as the payout policy has been consistent, so should be dividends in relationship with income.

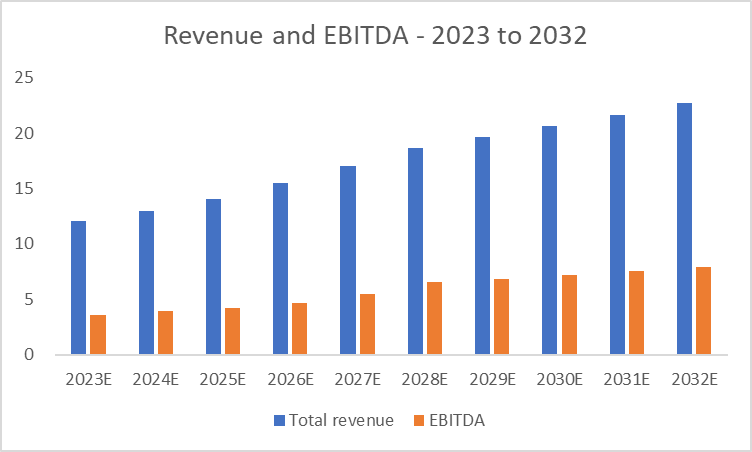

Forecasted Revenue and EBITDA (Author’s estimates)

This is what our forecasts look like. We have input some assumptions that reflect our view, but are also reasonably anchored to the past reality. We think the company should be able to continue to conservatively grow revenues at around 5% a year and accelerate such growth from 2026 to 10% for a couple of years. We believe this could be the result of a normalization of the macro and credit environment.

Then we used a 30% NOI margin (consistent with the past one) which we expect to expand up to 35% by the end of the forecasting period. This is due to gains in efficiency that we already saw across the portfolio in the last period, and can be emulated going forward.

Capex assumptions are divided in growth and maintenance capex, which is necessary to keep the existing facility functioning and attractive for tenants at the right rates. We estimate growth capex at 5% of revenues and maintenance capex at around 0.8% and growing to 1% after 2024.

For the period after 2032, we decided to use an exit approach. As well-managed and solid REITs are often interesting takeover targets, we think that SELF could easily become one after almost a forecasted decade of growth. In this scenario, we use an EV/EBITDA exit multiple of 17, which is the sector’s median number. After subtracting net debt, we arrive at a fair equity value per share of around $6.60, for a potential upside of around 30% from the current price.

Conclusion

We believe that Global Self Storage is probably the best player to get exposure to a growing and healthy real estate market: self-storage. The past results highlight a sound and resilient business with a strong balance sheet and a history of consistent dividend payments. Our models with inputs assumptions on growth and margins highlight a good undervaluation and an upside potential of around 30% to a $6.60 fair value per share.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here