Co-authored by Treading Softly.

A common mistake people make is failing to plan for the future. There is a classic saying that goes, “failing to plan is planning to fail.” This might seem harsh, but it does resonate in plenty of people’s life experiences. The reason is that, while it is important to enjoy and live in the present, you must have an idea of where you are going. Could you imagine if a cruise ship captain decided to just live in the present and not have a chartered course for his ship? It would be very easy for that ship and that captain to drift off and lose track of where they are going because they are enjoying the moment. Calamity would occur, especially since cruise ships cannot endure constant travel at sea without being resupplied.

While you may not be on this hypothetical cruise ship, your life, and its direction, need the same level of diligence in preparation for the future. There’s a reason why over 50% of Americans are failing to properly save for their retirement. It’s because they tend to focus too much on living in the present instead of planning for the future.

When it comes to the market, I like to see companies that can benefit from current market conditions while also having plans to benefit in the future. I like to be paid a high yield now, but also have the knowledge, understanding, and sector outlook that the income from my investments will continue to be strong going forward. I’m not looking for a flash in the pan to buy and sell within six months and hopefully walk away with a big gain – that’s not my style of investing.

Today, I want to look at a company that offers a mind-blowing double-digit yield, but whose management team is diligently preparing for the future, meaning that my ability to continue collecting income will remain strong going forward.

Let’s dive in!

Building for the Future

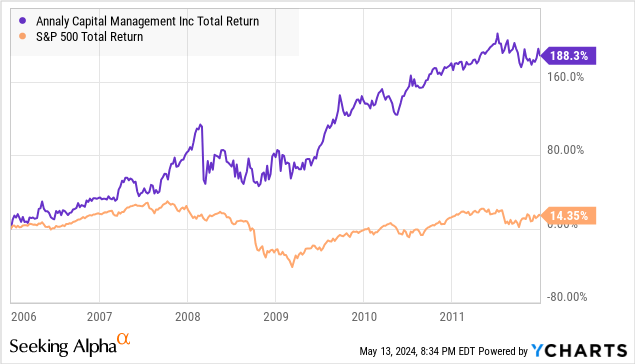

Annaly Capital Management, Inc. (NYSE:NLY), yielding 13.2%, earned solid earnings, with book value climbing to $19.73/share and EAD (Earnings Available for Distribution) at $0.64.

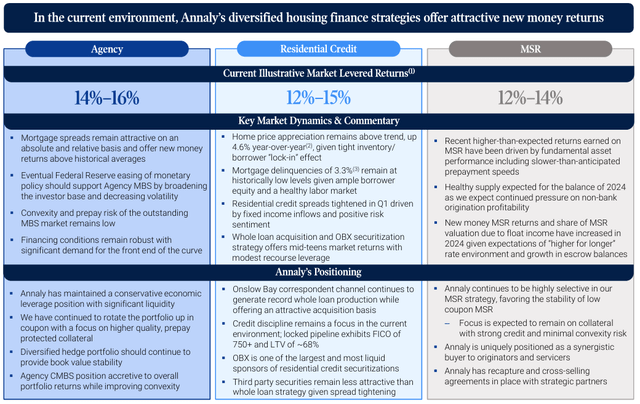

Looking forward, NLY expects to produce returns on equity of 12-16% across its various investment strategies. Agency MBS remains NLY’s largest allocation, accounting for $64.7 billion in assets and $6.7 billion in capital. Source.

NLY Q1 2024 Presentation

NLY’s current distribution is 13.2% of equity, which is very consistent with NLY’s expected earnings power.

Many have asked: “what about when NLY’s interest rate swaps roll off?” NLY has already gone through its lowest interest rate swaps. NLY’s shortest-term swaps have an average maturity of 1.46 years and a pay rate of 3.53%. Source.

NLY Q1 2024 Presentation

So, going forward, we expect that NLY’s earnings will be relatively stable, with an upside when interest rates start to decline. If interest rates stay “higher for longer,” NLY should be able to continue to coast, increasing its average coupon.

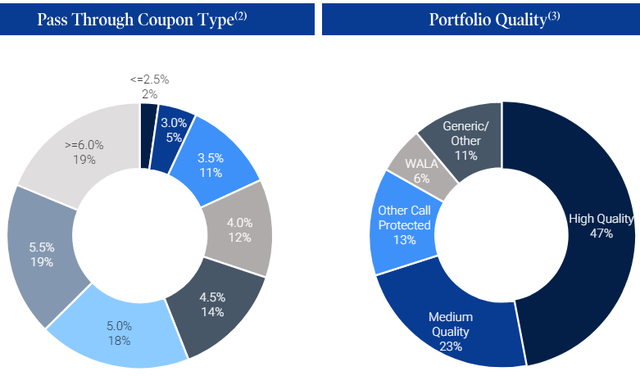

NLY’s strategy is to rotate into higher coupons and higher “quality.” Here is NLY’s agency MBS portfolio as of Q1 2024:

NLY Q1 2024 Presentation

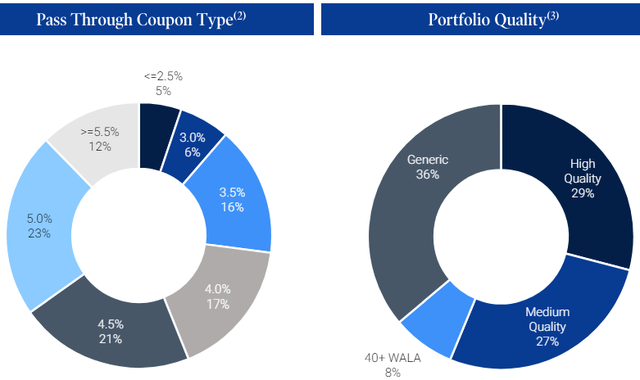

We can compare this to NLY’s agency portfolio at the end of Q1 2023:

NLY Q1 2023 Presentation

Note that coupons over 5.5% have increased from 12% of the portfolio to 38% of the portfolio. Additionally, the portion that is “high” quality has transitioned from 29% of the portfolio to 47%, while the lowest quality, “generic,” declined from 36% to 11%.

When we discuss “quality” for agency MBS, we are not talking about default risk. After all, if a borrower defaults, the agency buys the mortgage back at par value. What NLY is referring to is prepayment risk. “High quality” agency MBS are mortgages that have certain features that make prepayment less likely. The benefit of buying a bunch of 6%+ coupon mortgages is greatly reduced if interest rates decline to 3% and all the borrowers refinance at lower interest rates.

By buying “high quality” pools of MBS, NLY expects to benefit from the higher coupons for a longer period of time. Currently, the cost of NLY’s repurchase agreements is around 5.5%.

NLY Q1 2024 Presentation

As a result, the spreads being realized even on 5.5-6.5% coupon MBS before hedging are not fantastic. If the cost of borrowing declines to 2% or less, having 5%+ coupons leveraged with debt at 3% or lower are producing incredible returns. By focusing on the “higher quality” pools, NLY expects that the period where it can borrow at very low rates will last longer before the high coupons are prepaid.

Much of the past two years for agency mREITs can be understood as them building up their upside. It is like a spring – NLY is increasing the tension with higher coupons and higher quality MBS. The longer it has, the more tension that is created and when the Fed pulls the trigger and cuts rates, the effort that NLY is putting in today is released and it will rocket up. If the Fed had cut rates last year, it would have had 1/3rd of the 5.5%+ coupon MBS it has today. If the Fed waits for another 6 months, NLY will have more 5.5%+ coupon MBS than it has today.

The more higher coupon MBS that NLY holds when the Fed cuts, the better. We know NLY is capable of explosive upside when the Fed cuts rates, especially when there is a recession. NLY during the “dot-com” bust:

NLY during the Great Financial Crisis:

We believe that the upcoming cycle could have an even stronger upside than either of these events, as agency mREITs have had a longer period of time to fill their portfolios with high-coupon MBS.

While we wait, we get to collect a very generous yield.

Conclusion

With NLY, by pairing it with previously covered mREITs—AGNC Investment (AGNC) and Dynex Capital (DX)—we’re able to take a three-prong approach to attack the MBS sector to enjoy not only the present with high yields but also the future steps that these different companies are taking to try and benefit from the sector’s recovery.

It should come as no surprise that I love a sector that is due for a strong recovery, but also pays high yields now. It’s precisely the type of investing that I enjoy because I enjoy collecting big dollars today with the plan that I can enjoy big dollars tomorrow as well. I’m happy to get paid to wait because patience is the friend of an income investor — Time is my ally. Unlike other types of investing that require quick trades or could involve a high degree of speculation, income investing allows you to be a net buyer of quality securities – sit back, enjoy the market, collect your income, and live a wonderful life.

To you and everyone else who’s reading this, I want you to have the most wonderful retirement possible. Whatever your dream retirement is, I want you to be able to achieve it. Income investing can be a tool that you use to achieve that goal because, at the end of the day, if you fail to plan, the only person who directly gets hurt is you and anyone who’s relying on you. I want you to be a person that others can look up to and be thankful for the planning and execution regarding retirement finances.

That’s the beauty of my income method. That’s the beauty of income investing.

Read the full article here