Those who follow my work know that I run a very concentrated portfolio. At any given time, I own between five and 10 stocks. At the moment, I have nine such holdings. The third largest of these, accounting for about 16.2% of my total portfolio as of this writing, is automotive retailer Group 1 Automotive, Inc. (NYSE:GPI). Although the company has been facing some unfavorable industry conditions, management has continued to grow the business at a rapid pace. On top of this, shares of the company look incredibly cheap, both on an absolute basis and relative to at least some other players. And even though shares of the business have risen nicely over the past several months, I do think further upside is still on the table. Because of this, I’ve decided to keep the “strong buy” rating I had on the stock previously.

Great growth continues despite issues

The last article that I wrote about Group 1 Automotive was published in the middle of November of last year. In that article, I talked about how the company continued to deliver from a sales, profit, and cash flow perspective. I acknowledged even at that time that the future was uncertain. But a combination of acquisitions and share buybacks caused me to be optimistic. I was also encouraged by how cheap shares of the business remained.

Given these factors, I had no problem keeping the company rated the “strong buy” I had assigned it in a prior article. And since then, things have gone quite well. While the S&P 500 (SP500) is up 3.3%, shares of Group 1 Automotive have seen upside of 14.7%.

Author – SEC EDGAR Data

Based on how strong upside performance has been, you might think that now would be a good time to cash in and look elsewhere for opportunities. But I don’t believe that’s the case. In my view, Group 1 Automotive has further upside that it can enjoy. I say this based solely on the fundamental condition of the business.

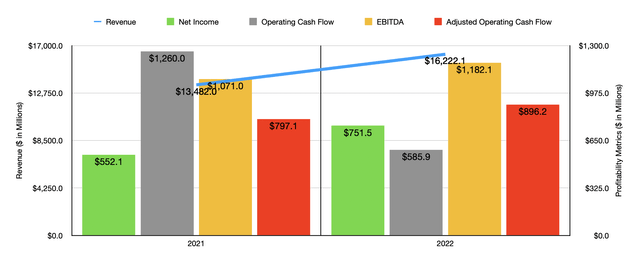

Consider, for starters, how the company performed for 2022 as a whole. Revenue for that time came in at $16.22 billion. That represents an increase of 20.3% over the $13.48 billion the company reported in 2021. During this time, the company enjoyed growth across most of its sales categories. Most impressive was the 27.8% surge in used vehicle retail sales. This move higher, according to management, was driven by a 14.1% rise in retail used vehicles sold, combined with a 12% increase in used vehicle retail prices. New vehicle retail sales also increased nicely, climbing 14.6% because of a 5.9% increase in new vehicles sold and an 8.2% rise in pricing.

It is important to keep in mind that this data does hide a bit of trouble the company is dealing with. You see, a very large portion of its growth is actually coming from acquisition-based activities. If you look at same-store locations, revenue is up only 3.7% year-over-year, with a 10% drop in new retail vehicles sold and a 0.2% decline in used retail vehicles sold negatively affecting the enterprise. From a profitability perspective, the company also showed improvements. Net income grew from $552.1 million to $751.5 million. As you can see in the first chart in this article, the other profitability metrics followed a similar trajectory. The only exception was operating cash flow. But on an adjusted basis, it also improved year-over-year.

Author – SEC EDGAR Data

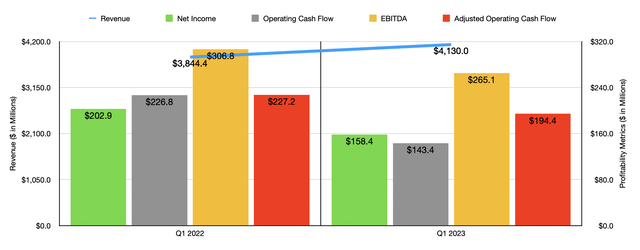

So far this year, things continue to look promising. Revenue of $4.13 billion represents a 7.4% increase over the $3.84 billion reported one year earlier. But in this case, the company did face some troubles. For instance, used vehicle retail sales were actually down 0.8% year-over-year, even as the number of units sold grew by 3.7%. This pain was driven by a 4.4% drop in pricing. Fortunately for investors, the company did see strength in the new vehicle retail category, with sales up 12.1% because of higher units sold and higher pricing. Unfortunately, inflationary pressures and supply chain issues have led to margins contracting for the enterprise. As a result, the gross profit per vehicle sold fell by 14% in the first quarter of the 2023 fiscal year relative to the same quarter one year earlier when it came to new vehicle retail sales. And for used vehicle retail sales, the decline was 15.8%. The company also suffered from an increase in its selling, general, and administrative costs of 10.6%. These factors were instrumental in pushing that income for the first quarter of the 2023 fiscal year down to $158.4 million compared to the $202.9 million reported one year earlier. Operating cash flow, adjusted operating cash flow, and EBITDA all declined as well.

Given these pressures, I can understand why some investors may be discouraged from investing in the business. But in my mind, there are three reasons to still be very bullish. For starters, management continues to make acquisitions aimed at growing the enterprise. On May 8th of this year, for instance, the company expanded its Texas footprint by acquiring 3 dealerships with expected annual revenue of $760 million. That brought total revenue acquired so far this year up to $910 million. The second reason why I remain optimistic is because management continues to buy back stock. During the first quarter alone, management acquired $34.7 million worth of shares, leaving $128.5 million of capacity under their share buyback program. And finally, there is the issue of how cheap GPI stock is.

Author – SEC EDGAR Data

Because of how much focus management has placed on growth, we don’t really know what to expect when it comes to the 2023 fiscal year. Management has also not provided much in the way of guidance. But if we annualize results experienced so far for the year, we would anticipate net income of $586.7 million, adjusted operating cash flow of $766.8 million, and EBITDA of $1.02 billion.

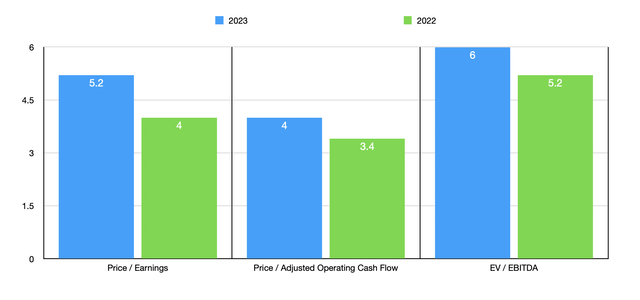

In the chart above, you can see how shares are priced on both a forward basis and using data from 2022. It’s always great to see company trading at low-to-mid single-digit multiples. As part of my analysis, I also, in the table below, compared the company to five similar firms. On a price to earnings basis, only one of the companies was cheaper than our prospect, while another was tied with it. Using the price to operating cash flow approach, our target was the cheapest of the group. And finally, using the EV to EBITDA approach, I found that only two of the five companies were cheaper than Group 1 Automotive.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Group 1 Automotive | 5.2 | 4.0 | 6.0 |

| Sonic Automotive (SAH) | 61.7 | 12.7 | 11.3 |

| Asbury Automotive Group (ABG) | 4.7 | 9.7 | 5.0 |

| AutoNation (AN) | 5.4 | 4.6 | 5.8 |

| Lithia Motors (LAD) | 5.2 | 24.4 | 6.9 |

| Penske Automotive Group (PAG) | 7.7 | 7.2 | 6.9 |

Takeaway

Operationally speaking, I believe that Group 1 Automotive, Inc. is a great company. I do recognize that margins in the space are going to come down. Because of inflationary pressures and high interest rates, I wouldn’t be surprised if overall financial performance for the company worsens to some degree in the near term.

But the good news is, even if the results seen in the first quarter of the year are reflective of what the rest of the year will look like, shares of Group 1 Automotive, Inc. are still very cheap on an absolute basis and are near the cheap end of the spectrum relative to similar firms. Given these factors, combined with continued acquisitions and share buybacks, I have no problem rating Group 1 Automotive, Inc. a “strong buy” even in spite of recent share price appreciation.

Read the full article here