Introduction

Headwater Exploration Inc. (OTCPK:CDDRF, HWX:CA) is a Canadian Oil and Gas Driller specializing in the Clearwater play in Northern Alberta province. We’ve written HWX up a couple of times previously, and if the company interests you, you might go back and give those older articles a read. (I go into a fair amount of description as to what makes the Clearwater formation special, and investors considering the company will be interested in these details.)

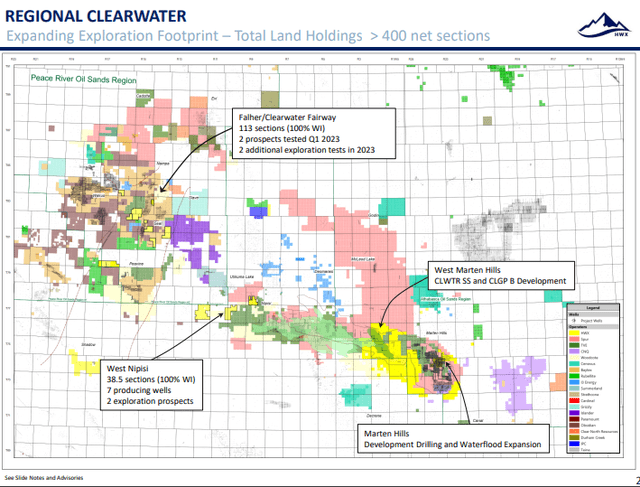

HWX footprint in the Clearwater (HWX)

HWX stock has underperformed since the last article, staying in a fairly tight band between $4-$5.00 per share. The selloff in commodities, combined with the large WCS discount, and the general concerns about the economy account for much of this shortfall.

In this article we will catch up with current events relating to the company and see if we can renew our buy thesis for them.

Why Headwater?

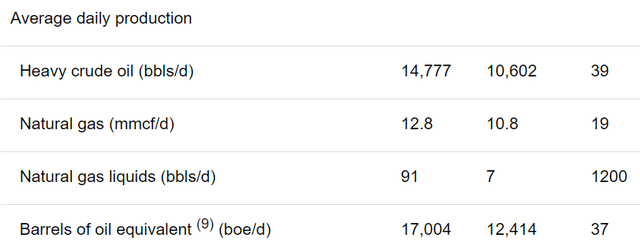

Headwater Exploration Inc. production tells the tale largely. It is heavily oil-weighted, ~80%, in part due to the shallow nature of many of the Clearwater horizons they are tapping. In the table below, you can see they are deploying capex very efficiently and have grown production of liquids almost 40% YoY, and full spectrum production 37%.

HWX production table (HWX)

The wells they drill are generally low cost and returned capital quickly-(a well with an IP30 of 295 paid out in about 3 months as an example). In the year ended Mar-31, 2023, for an incremental capex investment in their overall~$175-$200 mm budget, HWX grew production by 4,590 BOEPD. At their AFF(Adjusted Funds Flow) Netback of $38.75 per barrel, that production will generate ~$475 mm of future AFF over a ten year span, using a 6% decline rate.

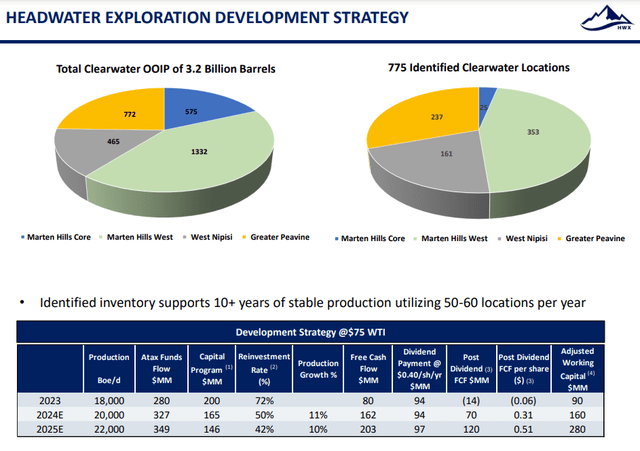

At last year’s Netback of $62.75, future investments could yield even greater returns. Their fairly high reinvestment rate of 72%, will fall in coming years as less capex is necessary to maintain output, as percent of total production.

The slide below shows the impact of declining capex on their reinvestment rate and after tax funds flow-atax. This money will go straight to the bottom line and be available for new M&A or shareholder distributions.

HWX Development strategy (HWX)

Catalysts on the horizon

Headwater Exploration Inc.’s acreage in West Nipisi and Greater Peavine combined make up about 60% of the Clearwater OOIP and 70% of the identified Clearwater drilling locations. West Nipisi in particular shows promise, with 6 wells drilled and completed, with IP30 rates in the best wells of ~300 BOEPD and IP60 rate of 282-285. This is a much better decline curve than a typical shale well. HWX also has a candidate for a Fishbone well that will increase reservoir exposure 50-75% over a standard horizontal.

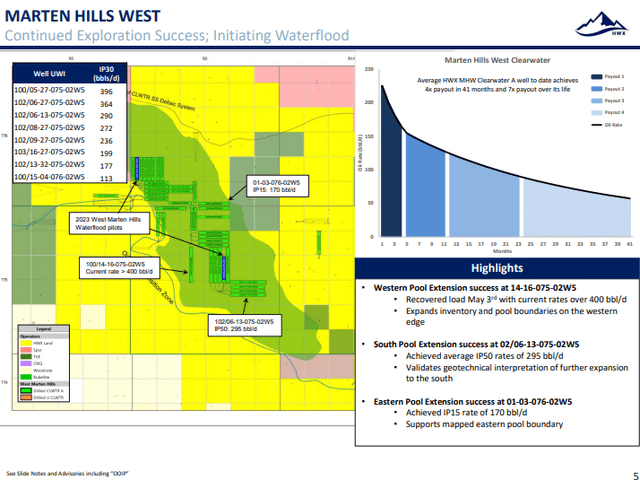

The Clearwater geology makes secondary recovery techniques feasible and economic and HWX is increasing their efforts in this form of recovery. Marten Hills West is one example of waterfloods contributing to HWX’s cash flow. Waterflooding is one of the cheapest forms of oil extraction. You can see from the slide below, the first payout comes in three months of production, and by the time the well waters out in 3.5 years, it’s returned 4X the cash required to drill it.

Marten Hills Waterflood (HWX)

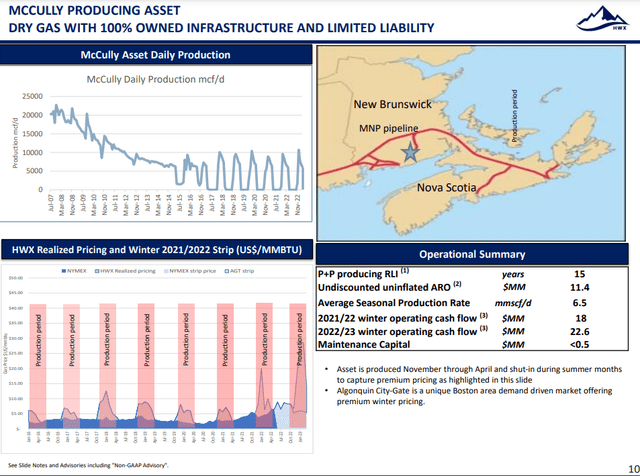

McCully gas field is another cash cow that operates seasonally as shown below. In a 6-month operating window that captures premium pricing at the Algonquin City Gate, McCully generates $22.6 mm in OCF.

McCully gas field (HWX)

Q1 2023 (CAD) and guidance

Revenues were down slightly at $88 mm from $90 mm in Q-4, 2022. AFF ran to 59.1 mm, down from $70 mm as 2022 closed out. Capex also fell to $69 mm from $88.5 mm, with seasonality in Canada playing a role there. Full year Capex for HWX ran to $231 mm and $69 mm in Q-1. The company carries no debt and has $154 mm cash on the books. HWX declared a $0.10 dividend for Q-1, payable 90 days in arrears.

The company hit 17K BOEPD in Q-1, and expects to exit 2023 at 18K BOEPD with a capex budget of $200 mm.

Risks

WTI prices and the WCS discount are the key risks to the thesis for HWX. Further declines in WTI and an expansion of the WCS discount could impair shares from present levels. We think these risks are moderate at this point, but are there none-the-less.

Your takeaway

In USD, Headwater Exploration Inc. is trading at 5X TTM EV/EBITDA and $61K per flowing barrel, using YE 2023 production estimates. In the zone, but not crazy cheap either.

2022 P2 reserves sit at 21.1 mm BOE, up from 15.7 mm BOE in 2021. HWX estimates future cash flows from these reserves to be $676 mm using a P-10 discount. With an enterprise value of ~$1.3 bn, we are quite a bit underwater using this metric as well. But perhaps for a low decline, low cost producer like HWX we should be a little more patient and allow for increased production and lower costs to justify these metrics.

Should HWX hit their production targets of 20K BOEPD in 2024, and 22K in 2025, we could see some growth in the stock price from a couple of sources. The first on valuation. HWX is forecasting $349 mm on ATAX Funds Flow for 2025. To keep the multiple the same the stock would have to rerate to $6.25 per share, or about 35% growth would be justified.

The second area would be capital returns in the form of increased dividends and stock buybacks. In particular, HWX has a lot of shares outstanding ~276 mm, and I expect as FF increases management will begin reducing the share count. Shares of Headwater Exploration Inc. could become very remunerative as the capital intensity of HWX operations declines. Patience is the key for this company to deliver the goods.

On that basis, I would give Headwater Exploration Inc. a buy rating at current for investors with modest risk tolerance. We would wish for a slightly better entry point to boost overall return, but accept that may not occur. For what it’s worth, the analyst cadre also ranks Headwater Exploration Inc. stock a buy with price targets ranging from $5.12 to $6.08 per share, so our targets appear reasonable.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here