The following segment was excerpted from this fund letter.

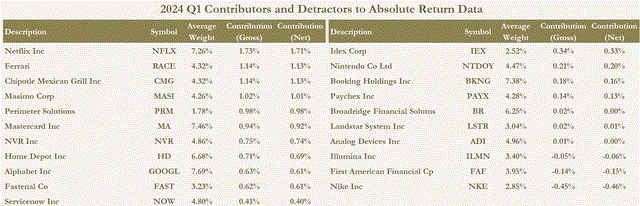

IDEX Corp (NYSE:IEX)

One of Ensemble’s newer positions is IDEX Corporation. IDEX is not a well-known company, and we believe it has the chance to be recognized as one of the next great serial acquirers like past Ensemble holdings TransDigm Group (TDG) and Heico (HEI).

One of the reasons IDEX is not well-known is because it sells decidedly mundane products, under many different brand names – mostly to distributors and other product manufacturers. It is highly diversified and owns over 50 subsidiary companies; these businesses typically sell niche parts and technology that help larger systems run smoothly in industrial and healthcare end-markets.

One of IDEX’s products is its Systec OEM MINI Degassing module. This module removes gases from fluids and can improve the accuracy of liquid chromatography equipment used to analyze the chemical composition of drugs in the pharma industry, for example. It is sold within IDEX’s Health and Science Technologies (‘HST’) segment, 40% of revenue. Another is its Sandpiper Heavy Duty Flap Valve Pump sold by its Warren Rupp business, counted within its Fluid and Metering Technologies (FMT) segment, 38% of revenue. The pump can be used in a larger Dissolved Air Floatation system that factories use to treat industrial wastewater. Its StreamMaster Fire Monitor is installed on fire trucks and used as a water cannon to extinguish fires. It is sold by the Akron Brass business within IDEX’s Fire and Safety / Diversified Products (FSDP) segment that is 22% of revenue. Flashy Ferraris these are not.

IDEX has been acquiring businesses that sell niche products like these for over three decades. In the last two calendar years, five acquisitions totaled over $1.2 billion. But why would we want to own a company that does so many acquisitions, when acquisitions so often fail, and for so many reasons? Roger L. Martin estimated in his 2016 Harvard Business Review article that “M&A is a mug’s game, in which typically 70- 90% of acquisitions are abysmal failures.” Some famous M&A failures include AOL’s $165 billion combination with Time Warner, Daimler-Benz’s $37 billion deal with Chrysler, and Sprint’s doomed $35 billion merger with Nextel.

There are many ways for an acquisition to fail, among them for an acquirer to overestimate strategic fit, to overpay, and to not recognize conflicts in business cultures or technologies. We believe, however, that IDEX is among a class of companies that can outperform via acquisitions, because acquisitions are its bread-and- butter. As opposed to an online service provider like AOL or a car company like Daimler-Benz overestimating the synergies of one big tie-up, acquisitions are what IDEX specializes in. Serial acquirers can be similar to great equity investors who have a disciplined process of buying good businesses at reasonable prices and do so repeatedly and at growing scale over time, much like Ensemble aims to do.

A strategy of serial acquisitions can compound above-average returns for decades if done right. Examples of successful serial acquirers include Constellation Software (CSU), TransDigm (TDG), Heico (HEI), Danaher (DHR) and Illinois Tool Works (ITW), all of which have outperformed the S&P 500 over the last 15 years.

IDEX’s stock has outperformed as well, with a 15% annualized total return since its IPO in 1989, about 4.5% above the S&P 500’s return over the same period.

IDEX’s path to its IPO started 10 years prior in 1979 as the first major leveraged buyout (‘LBO’) by famed private equity firm KKR. At the time it was a 50-year-old auto parts company called Houdaille Industries. Houdaille was taken over by the British-based TI Group PLC, which spun off several businesses it didn’t want into an entity that was again LBO’d by KKR in 1988. The resulting company was named IDEX – an acronym for Innovation, Diversity and Excellence, headquartered in the Chicago area. The LBO left IDEX with a pile of debt to pay off; according to Donald Boyce, the first CEO of IDEX, “It made us focus on cashflow.” Since 1990, IDEX’s operating cash flow has grown at a double-digit pace of 11% annualized, according to data from Bloomberg.

We attribute IDEX’s success to three things: Its 1. Discipline 2. De-centralization and 3. Scale.

IDEX is disciplined in the types of investments it targets and in its financial management. IDEX generally acquires businesses that have #1 or #2 share in small, fragmented markets uninteresting to larger competitors. The businesses IDEX acquires typically sell components or technology that are small portions of the overall cost of their customers’ systems, but that also must be counted on to work. For example, its BAND-IT fasteners, such as steel bands and clamps, are used to hold together objects on everything from ships to aircraft where the cost of failure could be disastrous. These types of parts, once trusted to work and to be supplied quickly and reliably, create a switching cost for customers who don’t want the risk or inconvenience of designing such a part out. This gives IDEX pricing power with its customers.

Management also has a minimum financial return it expects to achieve on its capital invested by year five after an acquisition, and regularly passes on deals that are too expensive. There is a minimum incremental EBITDA margin target of 25% for IDEX that discourages a lot of dilutive acquisitions, and it aims to consistently pay out 30-35% of its net income in dividends.

A second key aspect to IDEX’s success is its decentralization. Unlike the rationale for most acquisitions talked about in the press, IDEX does not expect much synergy between its businesses. While IDEX does buy businesses in certain areas it calls its “business platforms” — such as pumps, valves, water, scientific fluidics & optics, and fire & safety, these businesses are not usually integrated with each other. IDEX gives its general managers performance targets specific to their business and enough leeway to empower them to achieve its goals. It is the antidote to micromanagement.

Lastly, we believe IDEX is successful because it operates at a scale that’s differentiated. It has gained talent, experience, and capital the last 35 years. Acquisitions have been part of IDEX’s DNA from the beginning, having got its start as a collection of businesses spun off from private equity firm KKR; KKR’s co-founder Henry Kravis served on IDEX’s board for the first 14 years (1988-2002.) In the last several years, IDEX has built up a team that specializes in sourcing deals for each of its segments, and in greenfield areas.

The company has also been influenced by the culture of Danaher, another successful serial acquirer whose stock price has returned almost 20% annualized the past 15 years. The past three CEOs of IDEX have been Danaher alums, including current CEO Eric Ashleman and the previous CEO Andrew Silvernail who adopted the “IDEX Difference” that is similar in concept to the Danaher Business System (DBS.) Danaher calls DBS a process for continuous improvement, lean manufacturing, and innovation. The IDEX Difference is a strategy with three pillars – Great Teams, Customer Obsession, and Embracing 80/20.

IDEX helps its general managers apply its 80/20 system of optimization upon acquisition and over time. IDEX’s 80/20 system asks the managers to focus on the 20% of causes that lead to 80% of the desirable outcomes. An example of 80/20 optimization would be to concentrate resources like money, time, and talent, on the 20% of products that account for 80% of profits. This is a simple and well-known principle used for over 30 years also by Illinois Tool Works (ITW), another serial acquirer whose stock has returned 18% annualized the last 15 years. David Parry, the former vice chairman of Illinois Tool Works, has served on IDEX’s board of directors since 2012 and we believe was influential in bringing this system to IDEX.

While IDEX mostly operates as a de-centralized entity, with each business having its own HR, finance, and marketing teams, for example — IDEX does offer some services at the corporate level that add value versus a simple holding company. IDEX has an office of business optimization that implements the 80/20 processes, and a talent academy to train and promote leadership internally. The talent academy gives employees opportunities for career growth not usually available within smaller firms. IDEX also supports its businesses’ growth initiatives, giving them access to IDEX’s large pool of capital if a project is considered worthy.

So what are some of the risks we face as shareholders of IDEX? Like with any serial acquirer, the company must continue to find acquisitions to execute, while being prudent in the quality and valuation of deals. We also expect IDEX to monitor shifting technologies and trends, and to respond appropriately in its capital allocation priorities, for example via divestitures and acquisitions. The company seems to be doing so by investing in faster growing areas recently like medical applications, optical devices, and specialty materials over traditional industrial pumps.

And what are some potential positive catalysts? IDEX has proven its ability to generate attractive returns from acquisitions in the past, and this could bode well for its chance to further compound shareholder value. We think IDEX could ramp the cash it deploys into acquisitions and it has gained the ability to do bigger deals. It generated over $600 million in free cash flow in 2023, and we think it could add significantly more debt to its balance sheet without damaging its creditworthiness. IDEX could also report improving sales growth as its customers are mostly through their de-stocking phase from inventory built-up amid the pandemic. Along with a new CFO, Abhi Khandelwal, who re-joined IDEX in November 2023, we think IDEX might be ready to fire on all cylinders.

|

Disclosures  PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities listed above. The performance information shown above has been calculated using a representative client account managed by the firm in our core equity strategy and represents the securities held for the quarter ended 03/31/2024. The individual quarterly net contribution to returns are calculated by reducing the gross contribution to return by 1/4 of the weighted average of the firm’s highest management fee, which is 1.00% per year. Information on the methodology used to calculate the performance information is available upon request. The performance shown in this chart will not equal Ensemble’s composite performance due to, among other things, the timing of transactions in Ensemble’s clients’ accounts. ADDITIONAL IMPORTANT DISCLOSURES Ensemble Capital is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Ensemble Capital does not become a fiduciary to any reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content. Ensemble’s Equity strategy is intended to maximize the long-term value of the underlying accounts. The strategy generally invests in U.S. common stocks, but from time to time the underlying accounts may hold cash and/or fixed- income investments in an attempt to maximize capital gains. The strategy holds mostly large and medium-capitalization stocks, although accounts may also hold small-capitalization stocks. Performance results for the Ensemble Equity composite since the composite’s inception on December 31, 2003, are unaudited and are subject to change. The Ensemble Equity composite includes realized and unrealized gains and losses, the reinvestment of dividends and other earnings, and is net of management fees, brokerage transaction costs and other expenses. Taxes have not been deducted. Net of fee performance was calculated using actual management fees. Management fees for an Ensemble Equity account range from 1.00% to 0.50% on an annual basis and are typically deducted quarterly. Fees are negotiable, and not all accounts included in the composite are charged the same rate. Results are based on fee paying, fully discretionary, unconstrained accounts managed with an Ensemble Equity objective and include those Ensemble Equity accounts no longer with the firm. Accounts must exceed $500,000 to be included in the composite. Accounts with assets below $500,000 and accounts with objectives other than Ensemble Equity are excluded. Unless otherwise stated, returns for periods exceeding 1 year are annualized. The comparative benchmark is the Standard and Poor’s Total Return Index of 500 Stocks (“S&P 500”), an index of 500 large capitalization equities, generally considered a comprehensive indicator of market performance. The S&P 500 Total Return Index includes realized and unrealized gains and losses, the reinvestment of dividends and other earnings and is not subject to fees and expenses. It is not possible to invest directly in an index. The holdings in the Ensemble Equity strategy may differ significantly from the securities that comprise the benchmark. All investments in securities carry risks, including the risk of losing one’s entire investment. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor’s financial situation or risk tolerance. Some securities rely on leverage which accentuates gains & losses. Foreign investing involves greater volatility and political, economic and currency risks and differences in accounting methods. Future investments will be made under different economic and market conditions than those that prevailed during past periods. Past performance of an individual security is no guarantee of future results. Past performance of Ensemble Capital client investment accounts is no guarantee of future results. In addition, there is no guarantee that the investment objectives of Ensemble Capital’s equity strategy will be met. Asset allocation and portfolio diversification cannot ensure or guarantee better performance and cannot eliminate the risk of investment losses. As a result of client-specific circumstances, individual clients may hold positions that are not part of Ensemble Capital’s equity strategy. Ensemble is a fully discretionary adviser and may exit a portfolio position at any time without notice, in its own discretion. Ensemble Capital employees and related persons may hold positions or other interests in the securities mentioned herein. Employees and related persons trade for their own accounts on the basis of their personal investment goals and financial circumstances. Some of the information provided herein has been obtained from third party sources that we believe to be reliable, but it is not guaranteed. This content may contain forward-looking statements using terminology such as “may”, “will”, “expect”, “intend”, “anticipate”, “estimate”, “believe”, “continue”, “potential” or other similar terms. Although we make such statements based on assumptions that we believe to be reasonable, there can be no assurance that actual results will not differ materially from those expressed in the forward-looking statements. Such statements involve risks, uncertainties and assumptions and should not be construed as any kind of guarantee. Readers are cautioned not to put undue reliance on forward-looking statements. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here