Overview

The nascent electric vertical takeoff and landing (eVTOL) aircraft market is receiving renewed attention in the wake of recent news reports and FAA releases. The conversation around this industry right now is one of progress and future integration of these small electric aircraft into existing transportation infrastructure. High-profile FAA administrators are putting their mark of approval on select companies by pivoting their careers there as well as taking on board seats.

Recent news should have the most significant impact on the two eVTOL frontrunners, companies that have steadily made progress in this early-stage market and continue to hold ahead of the pack. These are Joby Aviation (NYSE:JOBY) and Archer Aviation (NYSE:ACHR). Both have distinguished themselves by demonstrating market-leading levels of progress on licensure and compliance for their eVTOL vehicles, although I will note that this process is far from finished for either of them. They are also relatively well-capitalized and each has backing from prominent investors.

When last I looked, Joby and Archer were roughly at parity in terms of their progress across several critical domains, including product development and customer acquisition. Joby notably held the lead on Certification. Things may have changed somewhat over the last two quarters. Nonetheless, it still stands that these two are market leaders and warrant consideration apart from the rest of the companies in the space.

In this article, I will review both of these firms from a comparative lens, evaluating their relative performance across relevant financial and business metrics. This should establish a clearer picture about who’s really in the lead and who’s best positioned to win in this emerging aviation market.

Certification

The first thing to compare is how far along each of these companies is in terms of getting their aircraft certified by the Federal Aviation Administration. The FAA Certification process is intensely rigorous and involves fulfilling 4 distinct sets of regulatory requirements that cover the type, method of production, airworthiness, and operational criteria of the aircraft being brought to market. This compliance process occurs over the course of 5 stages, each of which relies on the previous stage and thus must be completed in order.

Joby Aviation is still in the lead when it comes to certification and appears to have added room to its lead over the last two quarters. As of its latest quarterly report, Joby is well into Stage 4 of the FAA Certification process. At this stage, they have had their aircraft design approved while also having finished submitting the means whereby they will test it (Stage 3). Now at Stage 4, Joby is at the stage where they are actively running tests, in conjunction with the FAA, on production hardware (functional aircraft).

Archer Aviation is only at Stage 3 of this process, presently working to align itself with regulators on how best to test its aircraft. It was delayed in its prior progress towards Stage 4 due to regulatory shifts that affected how it will need to build its aircraft. This has resulted in the need for Archer to go through a recertification process for its G-1 (Stage 4) Certification, a process which it is still working through.

At the moment, it looks like Joby will likely be the first eVTOL operator to get its planes licensed, which would be slated to occur about 2-3 quarters ahead of Archer. Archer’s timeline could also change, however, as the head administrator of the FAA is close to signing a contract to join Archer. Assuming this hire happens, it should make a difference in helping Archer regain momentum on its certification process. Nonetheless, Joby has significantly more traction right now and also appears to have a better cadence as to working with regulators. Ultimately, I expect this lead to persist.

Financials

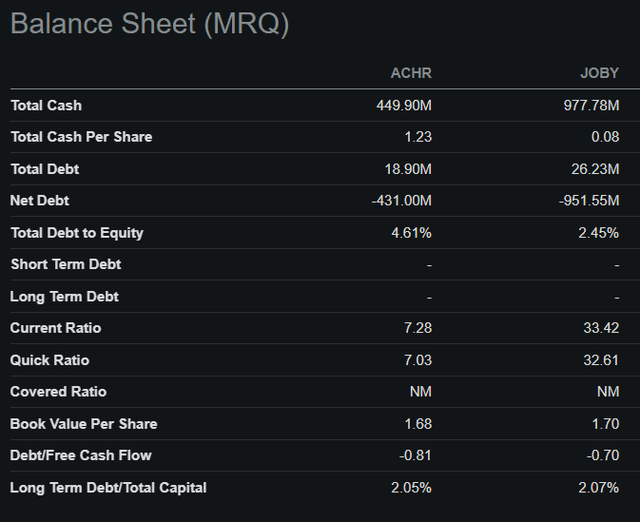

Having covered where things stand as to FAA Certification, we can now compare financials across these two companies. Neither company has revenue at the moment and must be looked at as a startup still developing product-market fit. This means that we are limited to looking at these firms’ balance sheets and respective capital structures in order to determine where they stand.

As it stands, Joby has more than double the cash on hand that Archer does. Neither company has too much debt, both having relied primarily on equity financing to date. Joby is still less leveraged than Archer overall and has superior leverage ratios. Book value per share is essentially identical across the two, differing only by $0.02. This means that the firms provide roughly identical per-share margins of safety in a liquidation scenario, although I don’t think that should concern us at present.

Seeking Alpha

Overall, the main highlight here is that Joby has a lot more cash than Archer. While this is obviously a plus, Archer’s balance sheet also looks excellent. Neither firm is leveraged to any meaningful degree, both have robust quantities of cash on hand, and both have maintained a positive book value per share. If anything, seeing these numbers gives me additional comfort in both of the companies’ near-term forward prospects.

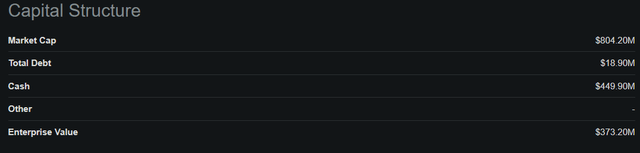

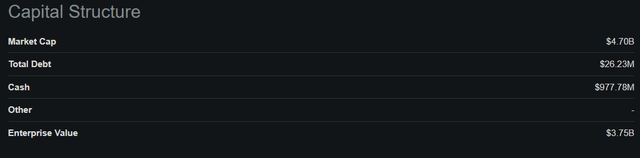

These healthy balance sheets are reflected in the capital structure for both companies. Joby is already much larger than Archer, with a market cap of $4.7B against Archer’s $804.2M. Joby is roughly 5.8x the size of Archer Aviation in terms of market cap.

Archer Aviation

Seeking Alpha

Joby Aviation

Seeking Alpha

This has resulted in Joby trading at a materially higher premium than Archer.

As of right now, Joby has a 4.10 TTM price/book ratio while Archer only trades at a 1.93. This equation flips when we look at the 1 yr. forward price/book ratio for each. Joby trades at 4.02 while Archer trades at 4.26.

Given the limited utility of the price/book ratio in this instance, however, we aren’t able to deduce anything about relative valuation. If anything, we can conclude that both companies properly reflect their per-share book values for the year ahead, demonstrated by the small spread between the forward P/B multiple between the two.

The most informative metric we have right now is each company’s respective market capitalization. Given how much larger Joby already is, it is clear that the market has already priced it as the leader. I’m not sure that it deserves to be this much larger than Archer at a time when neither company is doing any business. While some disparity may be warranted, Joby being nearly 6 times larger at this stage seems speculative.

Risks

The main risk to these two firms is being unable to get their businesses off the ground. This can happen for several reasons, including failed certification or running out of money. These two processes are related because a longer certification process means a longer time without getting a shot at revenue, increasing the likelihood of burning through available resources without making it to market. While robust in terms of their balance sheets, both companies must continue to spend money without making it for the foreseeable future.

Furthermore, these companies are attempting to establish an entirely new consumer transportation market and could fail to do so. While modes of travel such as helicopters exist, eVTOL is distinct from helicopters and are expected to be much more economic, which in turn is expected to allow for much broader utilization amongst consumers. This market could simply not exist in the form that these entrepreneurs believe.

There is significant uncertainty here, along with a highly capital-intensive business model. Buying into these stocks at this stage is a speculative and high-risk proposition.

Conclusion

I think these stocks are entering a period in which they could trade well and appreciate on the basis of momentum and progress toward getting to market. The story of these two firms is one of Innovative technology that is designed to undergird an entirely new consumer transportation market. As these companies increase in their profile and more investors learn about them, I expect that their story will catch the eye of a group of investors that are future believers in its business. This could then create a span in which these stocks generate significant returns, well prior to the companies even getting their products into the market. This momentum trade is my preferred way to trade these stocks for now. I would say that both are a buy for a 6-month investment horizon.

Read the full article here