Nu Holdings’ (NYSE:NU) Nubank emerged in Brazil as an alternative to the credit cards of large banks, relying mainly on technology, a simple and intuitive interface and a high standard of customer service marked by minimal bureaucracy in the banking sector.

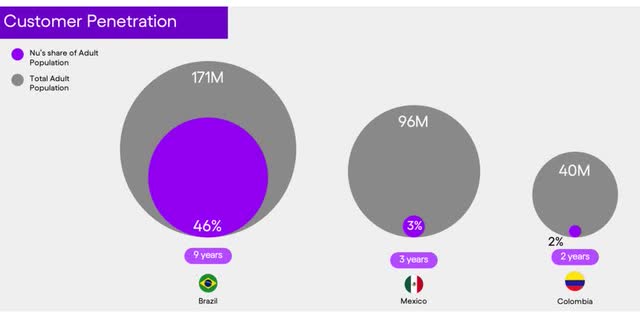

Today, the Nubank brand is one of the most popular in the country, having already reached such a significant number of customers that it implies that about 46% of the Brazilian adult population has an account with the digital bank. The bank is also quickly expanding its customer base in Latin America to Mexico and Colombia.

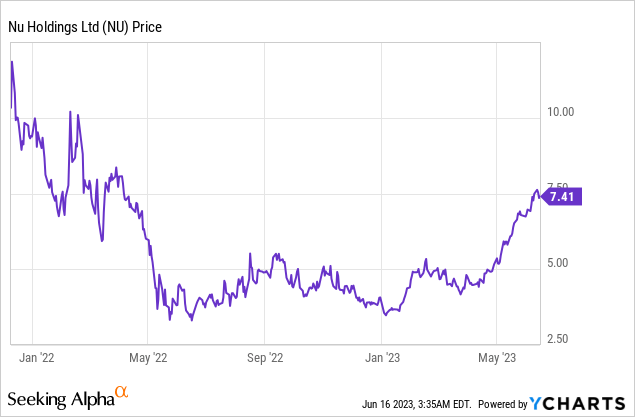

As of December 2021, Nubank went public in an IPO with a market value of $41 billion, about $60 billion short of its target valuation – including raising $500 million from Berkshire Hathaway. Still, it looked like the Brazilian digital bank was managing to post a good value.

However, shares of Nubank ended up having their market value fall as much as 70% by mid-2022 amidst tense macroeconomic times marked by high inflation and rising interest rates, importing the target and investors to growth companies.

Currently trading almost 40% below its IPO share price, Nubank’s shares are still trading at valuation multiples well below their historical peak.

Although its stretched valuation suggests great sensitivity around the stock in an environment that should be increasingly challenging as the global economy slows, Nubank continues to show every quarter avenues of growth and market expansion that make promises of future profits more and more feasible.

Undergoing rapid and substantial expansion

Nubank is today the world’s most prominent digital banking platform, with a customer base of about 80 million customers, of which 82% are currently active. Since 2021, the Brazilian digital bank has already doubled its customer base, and more recently, in its last quarter; Nubank grew more than a third of its customers.

How did Nubank achieve such fast growth? It is simple, offering a high-quality service, fully digital, without bureaucracy, and without charging fees from its customers. Nubank now has the highest Net Promotor Score (NPS) of any company in the sector, at an incredible 87, about 12.5 points ahead of traditional banks.

One could say it is relatively easy to attract millions of customers by offering free services but monetizing them would be another story.

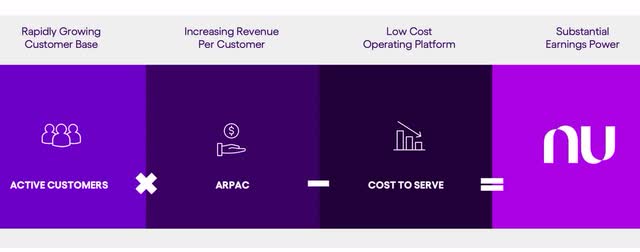

But Nubank has been following a concrete formula for generating substantial earnings power in the long term, which consists of active customers multiplied by average revenue per active user (ARPAC), subtracted by cost to serve, totaling a substantial earnings power.

Nu Holdings Investor Relations

- Active customers: Nubank has a rapidly growing customer base (CAGR of 46% in the last two years) and early-stage penetration in Mexico and Colombia.

- Increasing revenue per user: ARPAC is growing by 30% YoY. Even though these figures are well below the average of traditional banks like Itaú (ITUB) and Bradesco (BBD), which have ARPACs between 35 and 38, the growth of the ARPAC shows that the bank’s strategy to accelerate personal loans with solid credit card performance is making good progress.

- Low-cost operation platform: Nubank’s cost per customer is below one dollar, precisely 80 cents, highlighting its capacity to scale its all-digital platform through sustainable cost advantages. This cost amount is approximately one-third of what Brazil’s top traditional banks incur.

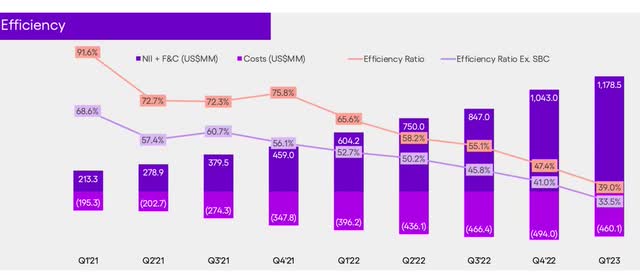

Efficiency levels are another essential metric highlighting Nubank’s capacity to grow and monetizing its customer base.

Within two years, Nu has reduced its efficiency ratio from 91.6% to 39%. The reduction means that the bank has significantly decreased its operating expenses concerning its revenues, which is considered an excellent efficiency level. To get an idea, Itaú, the market leader in Brazil with the most extensive credit portfolio among banks, currently has an efficiency level of 39.8%, lower than that of Nubank.

Nu Holdings Investor Relations

Valuations

When analyzing Nubank’s valuation metrics, it is easy to see that the digital bank trades at a premium. But we should clarify that the market decided to put it in a premium category since Nubank is disrupting the banking industry regarding growth and accessibility.

Compared to other traditional Brazilian banks like Itaú, Bradesco, Banco do Brasil (OTCPK:BDORY), and Santander (BSBR), investors have overvalued Nubank, considering the revenues presented by the bank in the last twelve trailing months.

| Market Cap | Active Clients | Revenues (TTM) | Price/Active Clients | P/S | |

| Nubank (NU) | $34,650,000,000 | 65,000,000 | 2,214,000,000 | $533.08 | 15.56 |

| Itau (ITUB) | $52,340,000,000 | 56,000,000 | 22,711,000,000 | $934.64 | 2.53 |

| Bradesco (BBD) | $34,470,000,000 | 38,300,000 | 15,694,000,000 | $900.00 | 2.38 |

| Banco do Brasil (OTCPK:BDORY) | $28,840,000,000 | 24,000,000 | 18,410,000,000 | $1,201.67 | 1.57 |

| Santander (BSBR) | $23,340,000,000 | 31,700,000 | 7,718,000,000 | $736.28 | 3.21 |

| Inter & Co (INTR) | $1,300,000,000 | 13,554,500 | 519,600,000 | $95.91 | 2.51 |

Increasing the comparative base, Nubank trades at much higher revenue multiples than its other Brazilian digital bank peer that trades in the U.S., Inter & Co (INTR). The difference between the price/active clients ratio between Nubank and Inter & Co, for example, makes evident the high expectations for the bank’s growth potential and future profitability even though Inter & Co has a very similar business model, albeit on a much smaller scale.

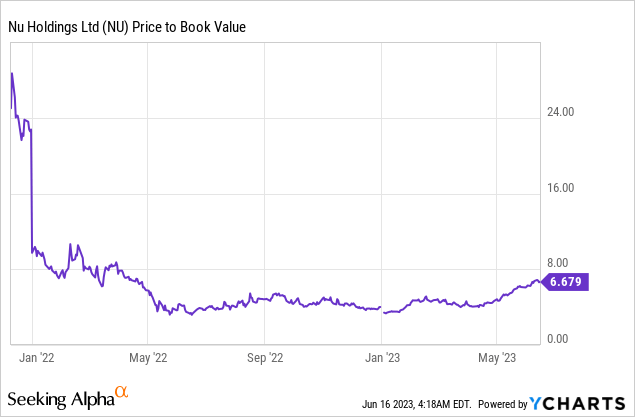

The only discount that Nubank currently has is concerning its valuation at the time of its IPO. Compared to the price-to-booking multiple of over 24 times that Nubank was trading as soon as it debuted on the American stock exchange, the current multiples are heavily discounted, trading 6.68 times.

Currently, Nubank shares trade at a forward price-to-earnings ratio of 56.39 times. Given that the consensus indicates that Nubank should have a 261% increase in its EPS over the next three years, the stock would be trading at a much more modest valuation multiple of 15.6 times its forward price-to-earnings – something much closer to the reality of today’s banking sector.

The revenue consensus for Nubank for 2025 is for the bank to reach figures of $11.9 billion, implying a 63% increase in revenues over the 2023 projection – Which is not too far off considering growing revenues in the last two years at a CAGR of 146%. This projected increase would result in a forward price-to-sales ratio of 2.91 times, which aligns with today’s banking sector average.

Growth avenues to support premium valuation

To justify the stretched valuation multiples, Nubank needs to report earnings growth over the years consistently, and this naturally requires a greater capacity to expand its customer base and ways to monetize it.

Nubank, with its substantial customer base encompassing half of the adult population in Brazil, is recognizing the growing challenges of further expansion in the domestic market. As a result, the bank has intensified its focus on investing in growth opportunities in Mexico and Colombia. The initial outcomes of this strategic shift have been noteworthy, as evidenced by Nubank’s investment of $330 million to expand operations in Mexico by the end of last year, totalling more than $1 billion in the past three years.

I see a great opportunity still not fully appreciated by the markets regarding the expansion potential of Nubank in the Mexican and Colombian markets – which, together with Brazil, comprises two-thirds of Latin America. Both countries have historically had an underpenetrated demand for financial services, far behind Brazil.

The low penetration rate of credit cards, for example, which stands at only 10% among the adult population in Mexico, makes clear the size of the opportunity that Nubank can explore. And the past year has been a consolidation as the digital bank expanded to 3.2 million customers.

Since Nubank late last year received regulatory authorization to start offering savings accounts and debit cards in Mexico, new account growth in the country is up 52% year-over-year, as the latest quarter pointed out. Nubank’s management has already stated that the Mexican operation may become more relevant than the Brazilian one.

In Colombia, although on a smaller scale, 636 thousand customers were reported in the most recent quarter, which comprised an increase of 200% compared to last year.

Currently, Nubank has a market penetration of 3% and 2% of the total population in Mexico and Colombia, respectively.

Nu Holdings Investor Relation

Another point that could become a game changer for Nubank’s credit portfolio and an essential source of future revenues is the bank’s participation in payroll loans. This type of credit, deducted directly from the employee’s salary or benefits, such as retirement or pension, is considered one of the banking sector’s most secure and coveted credits. And Nubank aims to expand in this area as management has been signalling.

This market has a more complex dynamic due to the need for an intermediary. However, Nubank plans to pass better efficiency to the client with better rates. Currently, the bank’s credit portfolio divides between credit cards – representing more than 80% of the bank’s portfolio – and personal loans.

Risks

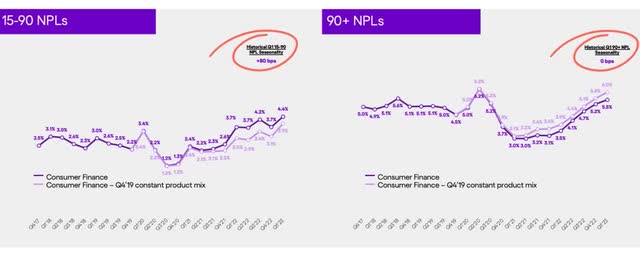

As reported in its latest quarterly results, Nubank’s NPLs are lower than those of traditional Brazilian banks. However, when looking at current NPL 90+ levels, Nubank’s indicators have jumped from 3% in Q1 2021 to 5.5% in the last quarter.

Nu Holdings Investor Relations

While this is not a significant problem for the bank for now, the long-term maintenance of delinquency and the desire to expand the credit portfolio in search of growth may be critical factors.

Macroeconomic risk considering the global economic slowdown, also presents a significant risk. With efficiency likely to play an increasingly determining role in a more adverse macroeconomic scenario, Nubank will need to maintain its investments in the Mexico and Colombia operations with a more focused eye on its efficiency ratio, which is currently the lowest in the industry.

Investors should remain alert because most of Nubank’s revenues come from Brazil, a country of high political and economic risk. The high-interest rate scenario in Brazil should stay until 2025, according to the Brazilian Central Bank’s projection of 9%. This high-interest rate scenario could contribute to raising default to more dangerous levels.

Finally, the high-interest rate in Brazil and the US increases the future general discount given to companies. The technology sector applied to fintech has taken this discount very heavily over the last few years – even though the first half of this year has shown otherwise. With the Federal Reserve’s ongoing fight against inflation, one should not rule out the possibility of recessionary pressures returning over the second half of this year.

The bottom line

Nubank is an exceptional growth case; that is still in the early stages of Latin America expansion. Despite being traded at very high valuation multiples compared to other traditional and digital Brazilian banks, Nubank has easily attracted customers spending very little capital and has been gradually increasing monetization on top of them, as the company’s most recent results have shown.

I see an excellent opportunity for future growth, mainly in the Mexican and Colombian markets, which are still underpenetrated. I estimate that in a few years, Nubank has plenty of capacity to replicate its Brazilian operation in these other two countries and multiply its revenues progressively.

Also, the bank’s further steps to exposure to other types of credit, such as payroll loans, should bring a significant competitive increase in the credit portfolio going forward.

I believe these bold growth prospects for the Brazilian digital bank offset the stretched valuation relative to its peers, even though the market had heavily discounted the current valuation from just over a year and a half ago when the bank had its IPO.

Read the full article here