Opening

Owens Corning (NYSE:OC) is a global company that operates in the home building products industry and specializes in manufacturing and marketing insulation, roofing, and fiberglass composite materials. The company operates in three segments: Composites, Insulation, and Roofing. Owens Corning distributes its products to various customers, including parts molders, fabricators, and contractors among others. The company was founded in 1938 and is headquartered in Toledo, Ohio.

This article aims to comprehensively evaluate OC’s financial performance and growth potential. We will closely examine the company’s revenue and profitability trends, its capacity to generate free cash flow, and the overall financial stability depicted in its balance sheet. Furthermore, we will utilize a discounted cash flow analysis to estimate OC’s intrinsic value, offering valuable insights to investors who are contemplating OC as a prospective investment opportunity in the present market.

Performance

A strong financial track record is important when analyzing a stock because it provides evidence of a company’s ability to generate consistent revenue, profitability, and cash flow. It indicates financial stability and suggests that the company is well-managed, increasing the likelihood of future success and potential returns for investors. Over the years, OC has established such a record.

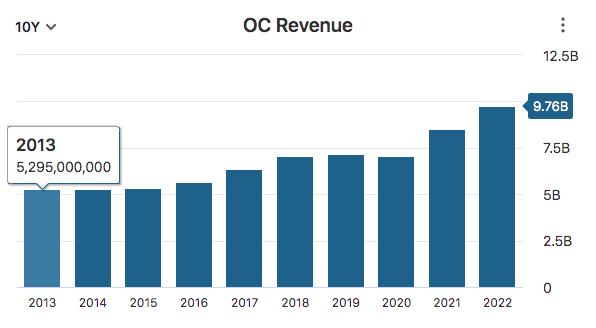

Over the past ten years, OC has maintained a steady growth trajectory, achieving a remarkable 84.4% increase in revenue while only experiencing two years of declines throughout the period.

Data by Stock Analysis

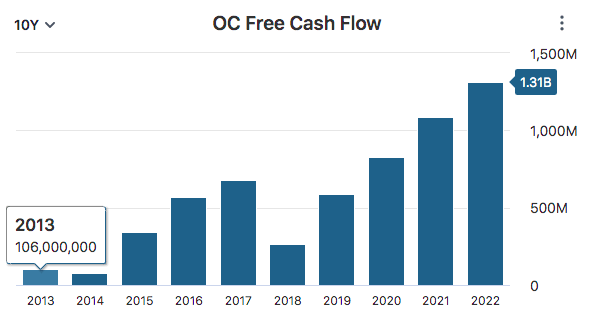

Furthermore, OC has achieved a remarkable 1139% growth in free cash flow over this duration. This substantial increase in free cash flow is a compelling testament to OC’s ability to generate a substantial amount of cash from its operations. This generated cash can be effectively utilized for various purposes, including reinvesting in the company, debt reduction, shareholder dividend distribution, and the pursuit of strategic initiatives.

Data by Stock Analysis

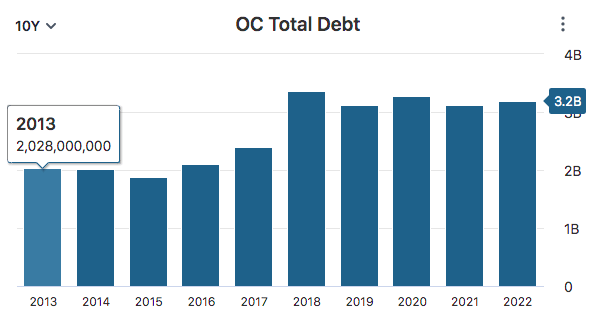

Despite the significant growth in OC’s free cash flow, it is important to highlight that this achievement has not been accompanied by a substantial increase in debt. In fact, the company’s total debt has only risen from slightly over $2.02 billion in 2013 to $3.20 billion, representing a modest increase of just 58.4%. This increase in debt is relatively insignificant compared to the rapid growth of OC’s free cash flow during the same period.

Data by Stock Analysis

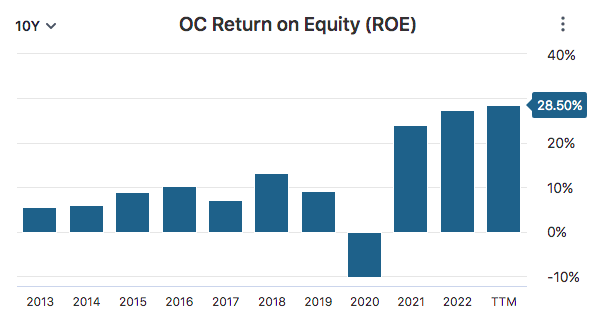

One concerning aspect of OC’s track record is its inconsistent performance in terms of return on equity (ROE). Over the past decade, OC has only achieved an ROE above 20% on three occasions. Moreover, the company even reported a negative ROE in 2020, although this can be attributed to the impact of the COVID-19 pandemic on the building product industry. Inconsistent ROEs are worrisome because they indicate a lack of stability and predictability in the company’s profitability, making it challenging for investors to assess its long-term financial performance. Additionally, such fluctuations may raise concerns about the company’s ability to generate sustainable returns and effectively allocate resources.

Data by Stock Analysis

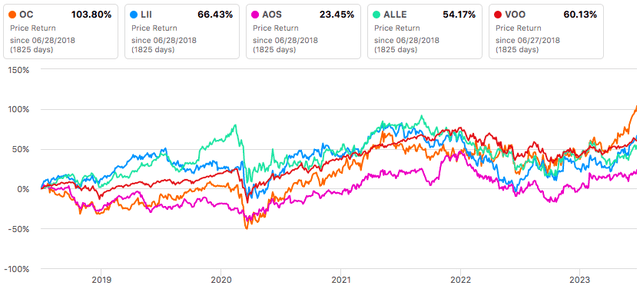

Overall, OC has put together a strong track record of financial performance over the last few years, leading to the stock outperforming its peers in the building products industry as well as the broader market over the past five years. However, investors are now pondering whether OC can sustain this exceptional level of outperformance in the future.

Data by Seeking Alpha

Forecast

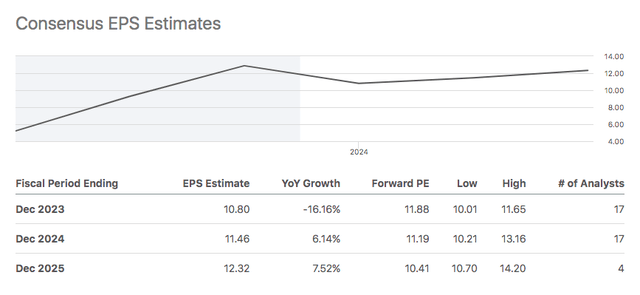

Analysts hold a pessimistic outlook for OC in the near term, as they anticipate a decline in earnings for 2023 to $10.80, representing a 16.2% decrease compared to the previous year. However, there is positive news as the company is expected to recover over the next two years, eventually reaching an estimated earnings per share (EPS) of $12.32 in 2025, although this would still be slightly lower than the $12.85 EPS reported by the company in the previous year.

Data by Seeking Alpha

OC’s gloomy prospects can be attributed to the ramifications of persistent inflation, elevated interest rates, and ongoing geopolitical tensions. These factors are causing a deceleration in global economic growth and diminishing demand across several of OC’s key markets.

Higher inflation, elevated interest rates, and geopolitical tensions can significantly impact companies in the home building products industry. These factors contribute to increased costs, as inflation drives up expenses related to raw materials, labor, and transportation. This can squeeze profit margins for companies as they struggle to pass on these higher costs to customers.

Additionally, elevated interest rates make borrowing more expensive, reducing affordability for potential buyers. This can dampen demand for home building products as higher mortgage rates discourage investment in new homes or renovation projects. Additionally, geopolitical tensions and uncertainties create economic instability and lower consumer confidence, leading to decreased spending on discretionary items like home building products.

The company is actively responding to the ever-changing business landscape by undertaking strategic investments aimed at enhancing its future earnings potential. These investments primarily focus on optimizing manufacturing networks, improving cost positions, and supporting long-term growth objectives. As part of the network optimization initiative, the Santa Clara insulation facility in California was closed in Q4 and sold in March as planned.

Furthermore, OC is actively investing in expanding its production capacity for key product lines. In support of the company’s roofing business, a significant investment is planned for the Medina, Ohio facility to enhance its laminate manufacturing capacity, specifically for its highly regarded duration shingles.

Additionally, OC has solidified its previously announced plans to construct the new Foamular NGX manufacturing plant in Russellville, Arkansas. Scheduled to commence operations in 2025, the state-of-the-art facility will cater to the increasing demands of its extruded polystyrene insulation customers, serving both residential and commercial construction needs.

Finally the company is busy with several new product launches. In the first quarter alone, OC successfully launched 11 new or refreshed products across the roofing, insulation, and composites businesses. During the company’s first-quarter earnings call, Brian Chambers, Chairman, President, and Chief Executive Officer of CO, shared insights on how the company is strategically allocating its capital.

These investments in additional capacity and product innovation, help our customers when they grow in the market, improve our operating efficiencies, and create new growth opportunities for our company, further strengthening our market-leading positions. As we continue to grow our company, we remain committed to operating at the highest standard and winning in the market the right way.

Based on the strategic initiatives and investments OC is making, the future may be brighter than analysts anticipate. The company’s focus on expanding production capacity, optimizing manufacturing networks, and launching new products demonstrates a proactive approach to addressing market challenges and capitalizing on growth opportunities. These efforts aim to improve operating efficiencies, strengthen market positions, and create new avenues for growth. Brian Chambers emphasized during the earnings call that these investments are intended to support customer needs, enhance operational performance, and unlock further potential for the company. With a commitment to operating at the highest standard, OC aims to position itself for success and strive to outperform market expectations in the coming years.

Valuation

We will employ the discounted cash flow (DCF) analysis, our preferred method for evaluating company value, to assess OC’s true worth. This analysis involves determining the present value of the company’s projected future cash flows to derive its intrinsic value.

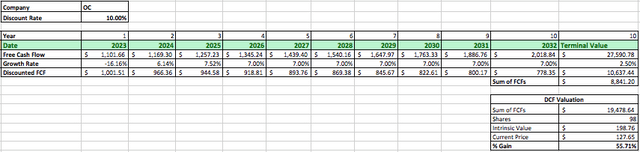

To initiate the analysis, we will start with OC’s free cash flow of $1.31 billion from the previous year. Considering the average analyst earnings growth rate of -16.2 for 2023, we will use growth rates of 6.14%, and -7.52% for the subsequent two years based on average analyst earnings estimates. Predicting OC’s future free cash flows beyond the next seven years presents challenges due to uncertainty and limited visibility. However, considering the company’s strong historical performance, which exhibited an average annual free cash flow growth rate of 32.2% over the past decade, a more conservative growth rate of 7% for the following seven years appears reasonable.

In order to calculate the terminal value, we will employ a conservative perpetual growth rate of 2.5%. Using a discount rate of 10%, which accounts for the long-term return rate of the S&P 500 with dividends reinvested, we ascertain OC’s intrinsic value to be $198.76. This indicates that OC may currently be undervalued, potentially leading to a gain of 55.7% for investors compared to the company’s current market price.

Author’s Work

Final Word

In conclusion, despite the pessimistic near-term outlook for OC due to various economic factors, the company’s track record of steady growth and strong financial performance over the past decade instills confidence. OC has demonstrated consistent revenue growth and a substantial increase in free cash flow, all while maintaining manageable levels of debt. Although return on equity has been inconsistent, it can be attributed to industry-wide challenges and the impact of the COVID-19 pandemic.

Moreover, OC’s strategic initiatives and investments position the company for future success. By expanding production capacity, optimizing manufacturing networks, and launching new products, OC aims to enhance its market positions and improve operating efficiencies. The company’s commitment to meeting customer needs and operating at the highest standard bodes well for its long-term prospects.

Considering the company’s historical performance and its ongoing investments, the future may be brighter than analysts anticipate. OC’s proactive approach to addressing market challenges and capitalizing on growth opportunities suggests that the company is well-positioned to outperform market expectations in the coming years.

Read the full article here