Editor’s note: Seeking Alpha is proud to welcome David Sommer Jr as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Invesco S&P 500 Equal Weight Energy ETF (NYSEARCA:RYE) is an excellent combination of high dividend yield and significant future growth potential. One of the key advantages and differentiators of this ETF is its equal-weighted approach. This allows for substantial growth potential from the smaller stocks since they make up a larger portion of the holdings as compared to a traditional market-cap-weighted index.

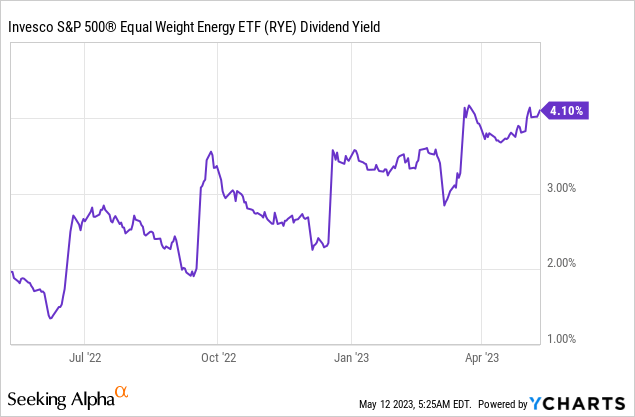

RYE also boasts an impressive dividend yield that has shown a steady uptrend, thanks to a decline in most stocks in this sector. Currently, the ETF has a 12 Month Distribution Rate of 4.0%. In today’s volatile market conditions, having a strong dividend yield from RYE can provide stability and comfort to a portfolio, particularly in a sector like energy, where prices typically gyrate over shorter time periods, given its visibility and importance to global market participants.

However, RYE may be bottoming around a familiar range of underperformance, which has represented a buying opportunity in the past, relative to the S&P 500. I rate RYE a Hold for now.

Strategy

RYE aims to track the S&P 500 Equal Weight Energy Plus Index by utilizing a full replication technique, meaning its holdings are identical to the actual index. It invests in both large-cap growth and value stocks across the energy sector. With approximately $495M AUM, RYE can be classified as a mid-sized ETF.

RYE holds every energy stock in the S&P 500, with each company being equally weighted at approximately a 4% portfolio position. This approach offers the investor more balanced diversification compared to a market-cap-weighted ETF. The fund and its index undergo quarterly rebalancing, at which point all holdings are rebalanced back to that equal weighting.

Strengths

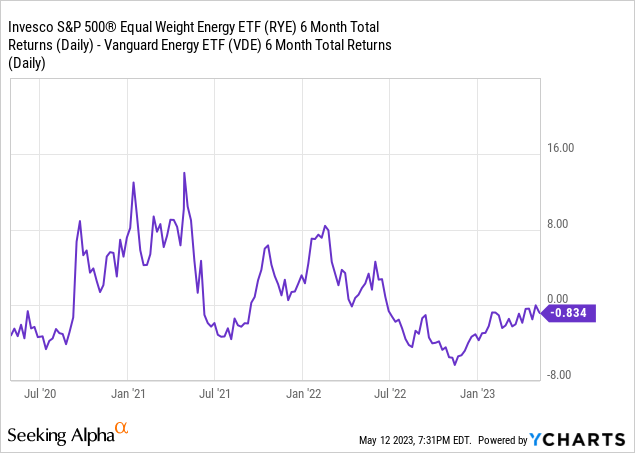

The greatest strength of RYE lies in its equal-weighted methodology. In contrast, a comparable fund like Vanguard Energy Index Fund ETF (NYSEARCA:VDE) is heavily skewed towards a pair of top holdings, with Exxon Mobil (NYSE:XOM) and Chevron (NYSE:CVX) comprising around 40% of that ETF. In RYE, these two stocks account for only 8%, as is the case with any two stocks, given the equal weighting mandate. Over the past 3 years, RYE’s equal-weighting strategy has outperformance VDE in the majority of 6 month time periods. Currently, it is underperforming by about 1%, making this ETF even more attractive. As the chart shows, in the past this has been a buying opportunity for RYE.

Weaknesses

“Recent oil price volatility” is truly an oxymoron. Investors know that this is a notoriously volatile sector, and any single-sector ETF is going to have concentration risk. But with the energy sector, the list of ever-present risk factors is especially long. This sector is heavily influenced by geopolitical conflicts, inflation, and the global shift towards sustainable energy sources, any or all of which, can significantly impact the profitability of RYE’s holdings. The ongoing transition of companies away from oil and toward alternative sources of fuel could potentially affect this ETF’s returns. Currently stated US government policies also pose a threat to the oil industry. While the government may not directly halt oil production, handing out incentives for electric vehicles and other “clean” energy sources can have a long-term impact on the price of oil. These policies, combined with other factors, contribute to the extreme volatility of oil, which may make it too unpredictable for very risk-averse investors to handle. The impact of new technologies is headline-worthy in that industry, though the ultimate trickle-down to long-term revenue and earnings growth is far from determined. The article pictured below discusses some of the potential changes, such as the US being a major supplier of liquified natural gas and new technology helping to limit greenhouse gas emissions.

lke.com

Opportunities

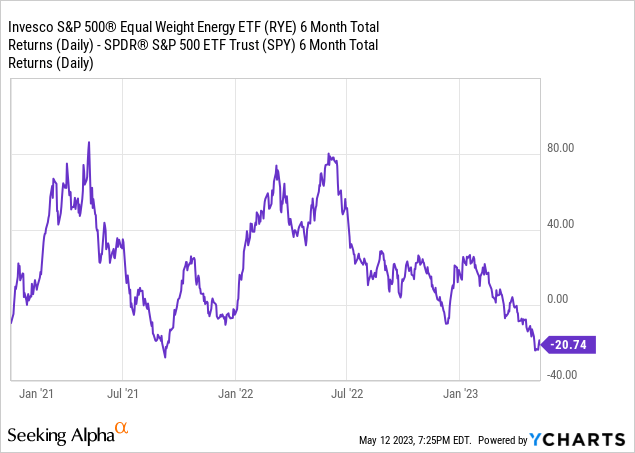

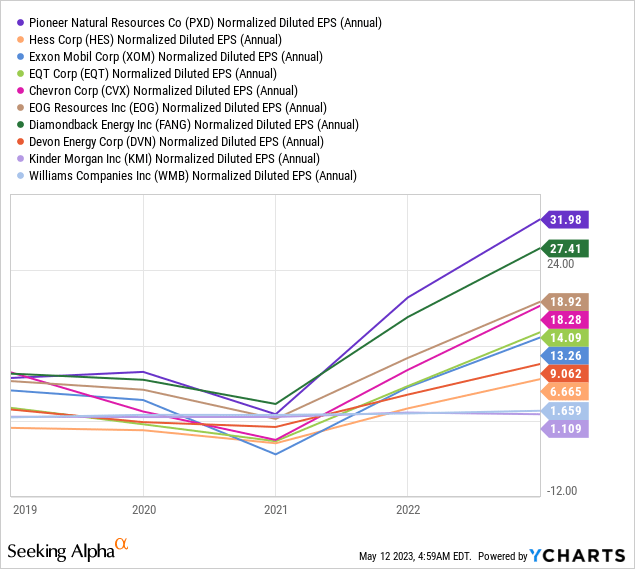

Since smaller energy companies have the opportunity to drive the returns of RYE to a much greater extent than in a typical market-cap weighted ETF, when stocks in this sector other than the very largest produce strong returns, RYE is a potential outperformer, perhaps significantly so. While the average energy stock has declined by about 15% since late November of last year, trailing the S&P 500 by more than 20% in the past 6 months (chart below) stocks in this sector have shown impressive resilience in recent years.

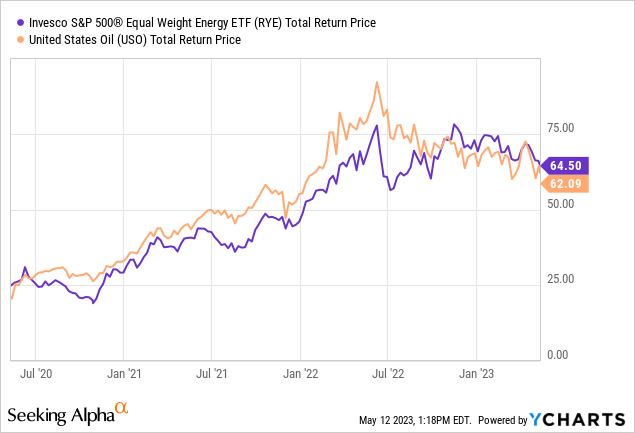

As the chart shows, since the start of 2021, RYE has rotated from dramatic outperformance to large underperformance of the broad stock market. However, RYE may now be bottoming around an underperformance level of 18-20% on that measure. This could very well represent a buying opportunity relative to the S&P 500, similar to what occurred in mid-2021. Energy companies have been reporting record profits (shown below), leading to higher dividend yields. If oil prices remain high, RYE ought to be a notable outperformer.

Ycharts

Threats

RYE is naturally heavily correlated with the price of oil, but that relationship is likely to be even stronger than usual in the short term. The possibility of an upcoming economic recession would likely cause a decline in oil prices, due to reduced consumer demand for energy products. Inflation has also contributed to higher oil prices. However, with inflation gradually trending downward and potentially becoming more manageable, oil prices stand a good chance of falling as well.

ETF Quality Opinion

I am watching RYE closely, with an eye toward turning more bullish on it if further evidence emerges that it is again closing the performance gaps with the S&P 500 and the highly-concentrated ETF, VDE. In a market environment starved for ETFs that can offer both growth potential and a high dividend yield, RYE may be poised to deliver both in a unique and sensible way.

ETF Investment Opinion

RYE is currently a Hold for me because of the volatile market, both broadly and in the energy sector. The recent decline in oil prices is a good start toward my considering RYE for a higher rating. I’d just like to get it even cheaper. If the economy does go into recession, that could very likely be the opportunity to do so.

Read the full article here