Snowflake (NYSE:SNOW) is finding itself in a challenging position as management forecast a slowdown in top-line growth for FY25 paired with tighter margins resulting from higher operating costs. Snowflake has also found itself in the middle of a major security breach at the customer level that has resulted in major data leakages out of these companies’ Snowflake databases. Though Snowflake’s security posture was not compromised, I believe that the association with the security breach may have a negative effect on new customer acquisition and may lead to current customers rethinking their use of cloud storage with Snowflake. Given these factors, I reiterate my SELL recommendation with a price target of $114.47/share at 10.58x FY26 price/sales.

Please review my previous report covering Snowflake here:

Snowflake’s High Growth Days Could Be Numbered

Tearing Off The Band-Aid

Snowflake finds itself in a peculiar position as a data lake turned AI/LLM analysis company. The firm realized continued heightened growth at the top line with an increase of 33%; however, management’s guidance for the duration of FY25 appears relatively lackluster as the firm transforms its offerings with Cortex AI and other new additions. On top of this, Snowflake customers experienced a significant data breach that affected 160 customers across its platform with no indication of any wrongdoing on Snowflake’s part. According to a joint statement provided by Snowflake, Mandiant (GOOG, GOOGL), and CrowdStrike (CRWD), no vulnerabilities, misconfiguration, nor breach were detected on Snowflake’s platform. The breach was detected on May 23, 2024, the day after Snowflake reported their Q1’25 earnings; the firm detected an increase of threat activity at the beginning of April 2024. The breach originated from users of the platform that rely on single-factor authentication, a risk that management is recommending customers to mitigate by enforcing MFA across their users. Though the breach affected only a small subset of Snowflake customers, the customers affected are no small players. For instance, Ticketmaster and Advance Auto Parts (AAP) were two of the customers affected by the breach, resulting in customer data exposure. According to TechCrunch, QuoteWizard, a subsidiary of LendingTree, was potentially impacted by the incident, whether directly or through manifestation.

Though large data breaches are relatively common occurrences in this day and age, the connection with Snowflake, a cloud-data storage provider, may differentiate this breach from others and ultimately affect the firm’s future growth more than others. Despite there being no evidence of any wrongdoing on Snowflake’s part, the association and the “what if” factor may lead to current customers questioning just how secure their own data is on the platform and may make new customer acquisition an uphill battle. Though this may not necessarily affect overall sales going forward, it may elongate the sales cycle as Snowflake must now assure new customers that their data is safely stored. I believe that the public impact of the breach may lead to an even slower growth rate than management’s forecast for FY25 and may further impact the already low forecast margins.

Management’s guidance for FY25 as of Q1’25 is a major drop-off from the previous year, with tighter adjusted operating margins and free cash flow. Much of the pressure to margins will be the result of the increased cost of GPUs and the firm’s AI/LLM initiatives paired with their recent acquisition of TruEra.

Corporate Reports

Looking to management’s guidance, the forecast for FY25 is $3.3b in product revenue with a 4% adjusted operating margin. Given the recent events, I believe there may be some challenges that will result in a slower acquisition rate. I believe new customers will take a wait-and-see approach to onboarding and await further details of the breach. Morgan Stanley analyst Keith Weiss believes the breach will have a minimal impact to the firm as Snowflake was not directly responsible for the incident; however, I believe that the risk of spread, even if nonexistent, will be in the back of CISOs and CIOs minds when considering Snowflake as a data lake option. As a result, I believe top-line growth will slow at a slightly quicker pace than what management has guided and fall short of the $3.3b target for FY25. In addition to a revenue miss, I anticipate margins to come in below management’s forecast as the firm digests additional operating costs resulting from AI developments and their acquisition of TruEra.

Corporate Reports

Management discerned that some of the margin pressure will be the result of the 35 new employees brought in through their acquisition of TruEra. Given the nature of TruEra’s business, these personnel may be vital to integrating their AI LLM analysis platform into Snowflake’s products to ensure a seamless transition. TrueEra’s business is significantly differentiated from Snowflake’s core operations and made for a good bolt-on acquisition. Given that management made it a point to mention employee retention through the acquisition, I believe the 35 employees’ compensation may be at a relatively high level given the tightness in the employment market for data scientists doing this work, leading to a significant change in OPEX going forward.

Snowflake may also be in a position of higher capital investments and operating costs in future periods as the next generation of Nvidia GPUs come to market. Between the H200 and Blackwell GPUs, Snowflake may need to make additional investments to remain competitive with their hyperscaler competitors, such as Oracle Corp. (ORCL), as AI factories and data base services continue to expand. Given the optionality offered by firms like Oracle for on-prem, hybrid, and cloud OCI, Snowflake may quickly become a high-cost, cloud-based one-trick pony. My core thesis on this matter is that once enterprises reach inference, AI applications will likely be moved to private data centers to ensure a secure environment for their data.

Overall, I maintain my negative outlook for Snowflake, despite their AI initiatives. Though the core product offerings may be a differentiated cloud-based database service, I do not believe that the platform will be leveraged for the long-term by cost-conscious enterprises once AI/LLM neural networks are trained and in production. Given the debottlenecking of Nvidia’s H100 GPUs, there may be more purchasing opportunities available for enterprise customers to expand their private data centers in making them AI-ready. If this is the case and plays out, Snowflake may need to diversify their database offerings beyond a cloud-based environment. This transition from cloud to on-prem thesis is in part based on my expectations for Oracle and Intel (INTC). I do not anticipate this phenomenon to begin occurring until the second half of calendar year 2025 at the earliest.

Valuation & Shareholder Value

Corporate Reports

Do note that the share count is Snowflake’s non-GAAP diluted shares outstanding.

Snowflake trades at a price multiple of 15.34x TTM sales, a relative premium to its peer enterprise data storage competitors.

Corporate Reports

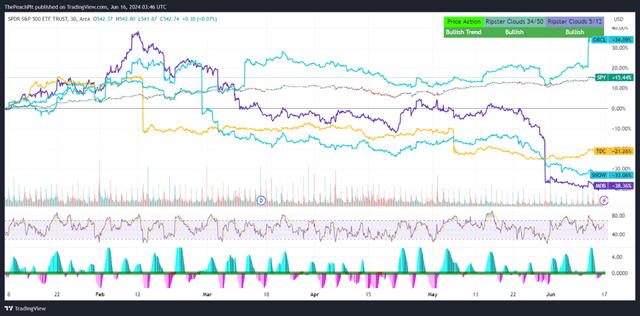

The overall database storage services companies have significantly underperformed YTD with SNOW declining -33%. Though I do believe the firm offers a phenomenal product, I do not believe it will realize the same level of growth going forward given the competitiveness of Oracle’s OCI.

TradingView

In turn, Snowflake may be moving into a strong position as an acquisition target for firms like Dell Technologies (DELL) or Hewlett Packard Enterprise (HPE) to offer an all-in-one infrastructure, storage, and AI application product.

TrendSpider

In terms of valuation, I am weighing more heavily on the downside risk in my probability model below given the recently reported security incident paired with the more challenging operating environment going forward. I reiterate my SELL recommendation for SNOW with a price target of $114.47/share at 10.58x FY26 price/sales.

Corporate Reports

Read the full article here