Summary

Readers may find my previous coverage via this link. My previous rating was a buy, as I believed S&P Global (NYSE:SPGI) should continue to see positive growth in the rating segment and that the drop in share price was a good buying opportunity. I am reiterating my buy rating for SPGI as the growth outlook remains bright and visibility to growth is now much clearer.

Financials/Valuation

In the recent 3Q23 quarter, SPGI saw total revenue growth of 7.8% to $3.084 billion, beating consensus estimate by almost 200bps. Notably, the strength of the beat was supported by all segments. Ratings revenue grew 20.3%, driven by healthy global debt issuance volumes in 3Q23. Market Intelligence revenue grew 8.1% y/y, Commodity Insights grew 10.9%, Indices revenue rose 6.0% y/y, and Mobility revenue increased 9.5% y/y. As a result of the strong top-line performance, SPGI EBIT reached $1.45 billion, beating estimates by 50 million. EBIT margin also expanded to 47%. EPS came in at $3.21, beating consensus estimates of $3.04.

Based on author’s own math

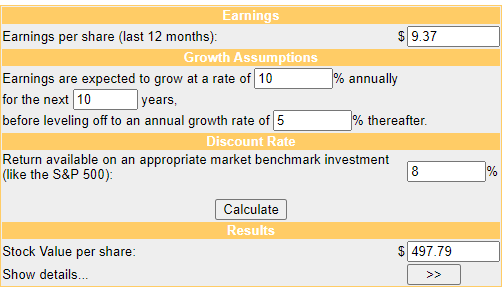

Based on my view of the business, I continue to use the two-stage DCF model to derive my price target for SPGI, given the long-term visibility of growth. There is no change to my growth assumptions, as I believe SPGI can continue to grow just as it did historically. Especially with the Ratings segment growth now expected to normalise back to 9% in 4Q23, I see that as an indication that things are gradually normalizing. With the updated EPS figure, my price target is now $497.80, a modest increase from my previous price target of $479.20. I remain bullish on the stock, as the upside is still attractive.

Comments

SPGI 3Q23 performance was nothing but spectacular. I reiterate my buy rating for the stock, as I think the positives significantly outweigh all the minor negatives in the quarter.

For the positives, the growth outlook for SPGI remains very strong as Ratings revenue continues to perform just as I expected, accelerating to 20% y/y growth from 6.9% in 2Q. Notably, the growth was faster than Moody’s (MCO) MIS (Moody’s Investor Service) growth of 18%, suggesting that SPGI is executing much better and capturing share. Importantly, for investors, management’s communication with the investor community gave better visibility into near-term growth. FY23 Ratings revenue guidance was raised to 6-8% from 5-7%, and the billed debt issuance growth assumption was revised to 5-7% from 4-8%, both of which suggest stronger performance ahead. This also effectively suggests that FY23 is going to end strongly and that FY24 is going to be a very strong year when compared to FY23, given the easy comps.

A similar dynamic is seen in the Market Intelligence segment, where the segment did really well (growth accelerated to 8.2% vs. 4.8% in 2Q23 and 4.3% in 3Q22), and that growth outlook remains bright (annual contract value [ACV], which is a good indicator of future revenue, growth outpacing desktop sales). Similarly, management guidance for the segment also points to growth acceleration in 4Q23, which was a pivotal guide as it dismissed the concern that growth is going to continue decelerating (2Q23 growth of 4.8% vs. 1Q23 growth of 5.1%). Looking ahead, there is also an ongoing catalyst-revenue synergies from cross-selling IHS Markit products-that could further accelerate growth. Revenue synergies execution is progressing very well; as of the latest quarter, run-rate revenue synergies have reached $112 million, roughly 30% of management FY26 target of $350 million.

Growth was evident across the board, including in the smaller segments like Mobility and Commodity Insights, thanks to the introduction of new products, increased cross-selling, and a better pricing strategy. While their contribution to the overall business is small, it was encouraging to know that the management execution level was not compromised to drive growth in its larger segment. In my opinion, this is a good thing because, particularly in the present macroclimate, these smaller segments serve to cushion the larger business from volatility.

Not only is the growth outlook very positive for SPGI, but management is also executing at a very high level to drive profitability improvements. As of 3Q23, management has already realised nearly all $600 million of run-rate cost synergies from the IHS Markit merger. With the combination of strong top-line growth that comes with strong operating leverage and the completion of cost synergies, I believe the margin expansion outlook is very bright as well.

For negatives, firstly, management noted that sales cycles remained elongated, consistent with past quarters. While this is definitely not a positive comment, I take comfort in knowing that deal sizes are larger, which somewhat compensates for the lower volume of deals (due to a longer sales cycle). Secondly, while SPGI raised its full-year guidance for rating revenue growth, the midpoint of the guide implies rating growth will decelerate from 20% year over year in 3Q to 9% in 4Q23. The latter point might seem bad from a headline perspective, but I note to investors that if you go back in history, SPGI Ratings segment growth averages high single-digits. Hence, growth at 9% suggests to me that growth is back to a normalised level, which is a positive thing.

“In the third quarter, sales cycles were consistent with the longer cycle we’ve seen in the last few quarters, though we are encouraged that these conversations with customers are often leading to larger deals.

Risk & Conclusion

I reiterate my risk for SPGI that its growth is still largely tied to the macro cycle, despite the contribution from its smaller segments. Further increase of interest rates will definitely impact debt issuance volume and SPGI growth, no matter how well SPGI could execute.

In summary, SPGI showcased an exceptional 3Q23 performance, reinforcing my buy rating. With revenue growth across segments and expanded margins, SPGI’s outlook remains robust. The raised Ratings revenue guidance and strong billing projections for debt issuance signify continued strength. While extended sales cycles persist as a concern, larger deal sizes offset this headwind. The forecasted normalization of Ratings growth to 9% in 4Q23, though seemingly a deceleration, reflects historical growth averages and signals a return to normalized levels.

Read the full article here