Overview

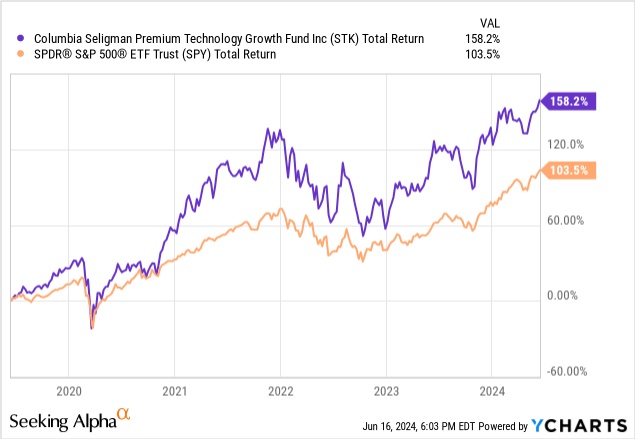

Columbia Seligman Premium Technology Growth Fund (NYSE:STK) has slowly become my largest closed-end fund to date, and it’s for a reason. I previously covered STK and discussed how its strong track record has outperformed the greater indexes such as the S&P 500 (SPY) and now the fund has become even more attractive. Since STK operates as a closed-end fund, the price can trade separately from the fund’s actual net asset value.

At the moment, the price trades at a more attractive discount than when I previously covered it back in December 2023. We can see that STK has outperformed the S&P 500 in total return over the last five-year period, and I believe that it has the potential to continue this outperformance due to its strategy and holdings. The fund has an inception dating back to 2000 and has an expense ratio of 0.94%.

Just for some context, STK operates as a closed-end fund that has a distinct focus on the technology sector by assessing each potential holding for future growth prospects, consistent earnings growth, and current valuation. Since the fund’s focus is mainly on the technology sector, this means that it has exposure to a lot of fast-growing companies, which translates to STK capturing more upside price growth than a typical CEF. Therefore, the total return has the potential to be made up of both price appreciation as well as a high distribution yield.

STK currently has a dividend yield of about 5.5%, which is higher than most other tech-focused funds out there in the market today. Since tech funds do not typically have larger yields, STK has to get a bit creative in order to generate the additional income needed to support the distribution. They do this by deploying an option writing strategy against the individual holdings within its portfolio. However, there are no set parameters for the deployment of options and management can use them as need be.

For example, the use of call options during bull runs may actually cap the upside price movement of STK if the underlying equity the call is based on gets executed at the strike price. To avoid this in bull runs, the management may avoid using as many call options. On the other end of the spectrum, in times of higher volatility, they may write more call options as a way to generate income from the premiums that can be collected. I really prefer this strategy as opposed to some covered call ETFs that follow a set formulaic method of operation that doesn’t fit all market conditions. I believe that this is what sets STK apart and what enables it to outperform.

On top of that, the holdings within STK gives solid exposure to some of the best companies in the world. A part of their strategy, according to the most recent factsheet, is to also pursue investments into high-growth companies that may see growth from tech innovation and advancements.

Holdings

Despite STK leaning more heavily on the tech sector, the fund’s approach is to strike a balance between secular growth and attractive value opportunities in the market. As a result, we get a blended mix of sector exposure alongside the tech allocation. Technology accounts for the majority of STK, accounting for 78%. I refer to STK as a technology-focused fund because of this large exposure, as each of the other remaining sectors accounts for less than 10% of the fund’s weight. Communication services makes up the second-largest slice of the holdings, accounting for only 9%. Financials make up 5% of the fund, Consumer Discretionary makes up 5%, Industrials account for 2%, and less than 1% of the exposure is to real estate.

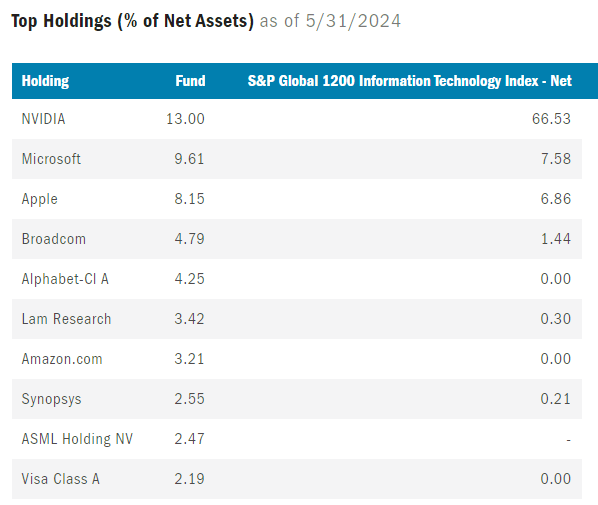

Another part of the fund’s strategy is to always assess the potential valuation of each of their holdings and make adjustments accordingly. Management has an internal analysis process where they determine what companies are likely to reap the rewards of technological growth and innovations and shift its weighting as need be. As a result, we’ve seen some changes from the last time I covered STK.

The most notable is that NVIDIA (NVDA) is now the largest position, accounting for 13% of the net assets. For reference, when I covered STK back in December, the largest holding was Lam Research (LRCX). NVDA has been crushing it lately as they are the leading company when it comes to the AI technological forefront, and I am glad to see that STK shareholders are benefitting from its growth. There are about 104 individual holdings within STK and the top ten holdings make up 53.64% of the total net assets. Therefore, it’s safe to conclude that the top ten holdings have the most influence and pull when it comes to the price performance of STK.

Columbia Thread Needle

In addition, Amazon.com (AMZN) is a new addition to the top holdings, accounting for 3.21% of net assets. Microsoft (MSFT) and Apple (AAPL) both got a slight buff in weighting, accounting for 9.61% and 8.15% respectively. While NVDA was the major change here, it’s still reassuring to see that management continues to implement rebalances to the holdings so that shareholders can get the best possible performance.

Dividend Income

As of the latest declared quarterly dividend of $0.4625 per share, the current dividend yield sits at 5.5%. While one wouldn’t normally a large amount of dividend income from a tech fund, STK is an outlier because it has managed to provide a growing stream of income of the decade. According to the distribution history, it looks like most of the distribution is funded by capital gains within. As a result, there could be some tax consequences associated with the income received from STK.

Columbia Thread Needle

Since the distribution is affected by the actual performance of the fund, STK seems to benefit when tech has a strong performance year. There have been instances, such as last year, when STK has provided investors with a large year-end special dividend payment. Last December, STK paid out a special dividend amounting to $0.2669 per share.

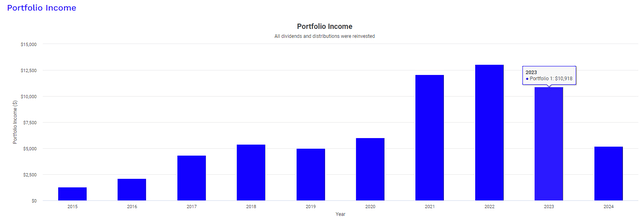

Despite the growth trajectory not being as consistent as a traditional dividend growth stock, there is still some solid dividend income growth that can be created over time. To better display the level of growth, I ran a backtest with Portfolio Visualizer to see what an original investment of $10,000 in 2015 would look like today. This visual assumes that a monthly fixed contribution of $500 was added to your position every single month. It also assumes that all dividends received were reinvested back into STK to help accumulate more shares.

Portfolio Visualizer

The results were that in 2015, your dividend income would have totaled $1,299 annually. Through consistency and a long-term outlook, this total would have now grown to nearly $11,000 annually by 2023 while your position size would now be valued over $185,000. Tech had a really strong year in 2021 and 2022 as interest rates remained at near-zero levels. As a result, we can see that the total amount of dividend income received in 2022 was actually higher than in 2023 due to better performance of the tech sector.

Valuation & Catalyst

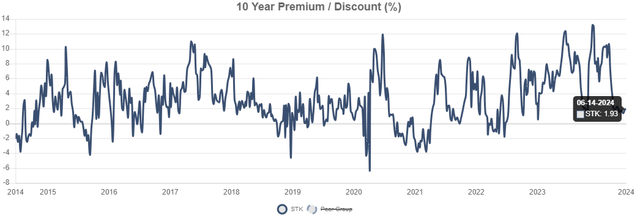

Since STK operates as a closed-end fund, the price trades at a variance to the fund’s NAV (net asset value). Therefore, the most ideal and preferable entry would be when STK’s price is trading at a discount to NAV. However, as you’ll see from the graphic below, STK has rare moments where it dips into that discount territory. In fact, we can see that STK trades at a premium more frequently and on a consistent basis. Trading at a premium doesn’t necessarily mean that it’s a bad time to start or add to a position by the way. Sometimes high-quality funds consistently trade at premiums because of the consistent performance of competent management.

CEF Data

In late 2021, STK peaked at all-time high levels slightly over $37 per share. As the price currently climbs back up towards these previous high levels, investors may start to get cautious and await for a better entry point. However, I believe that STK currently sits at a more attractive price point than when I wrote about this fund six months ago.

For instance, STK currently trades at a premium to NAV of 1.93%. This represents a slight decrease from the last time I covered STK when it traded at a premium to NAV of 6%. Additionally, STK has actually traded at an average premium to NAC of 4.85% over the last three-year period.

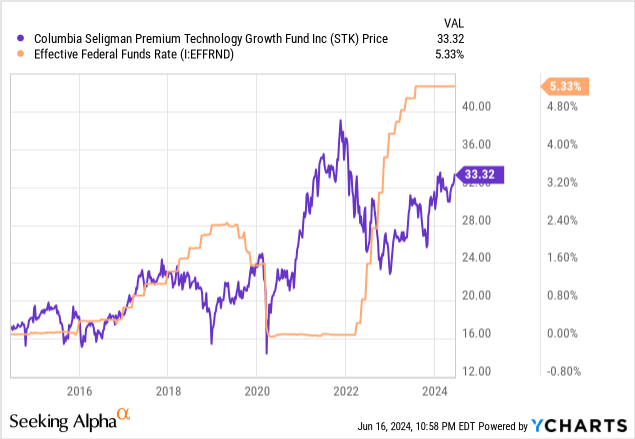

I also believe that we may have a potential catalyst with talks of interest rate cuts on the horizon. We can see that when interest rates were cut to near zero levels following the covid-pandemic, STK’s price quickly rose as companies had access to cheaper debt that could be used to fund operational growth, capital expenditure spend, acquisitions, and other growth initiatives. Conversely, we can see that the price of STK sharply fell around Q2 of 2022 as interest rates began to get aggressively hiked. Higher interest rates slow the growth of these tech companies as the cost of borrowing rises and margins get smaller.

As of the latest meeting, the Fed has decided to leave rates unchanged. The Fed estimates that there will be one rate cut to take place by the end of 2024, but for now, they are awaiting more economic data to roll in around inflation, the labor market, and consumer spending levels. As inflation finally begins to cool and the unemployment rate slowly creeps above the 4% level, I believe that we are on the brink of the next rate cuts happening. As interest rates are cut, I believe that this will be a growth indicator for the market and STK should be able to benefit as tech companies are likely to see higher valuation from the more attractive cost of borrowing that can fuel growth within.

Vulnerabilities

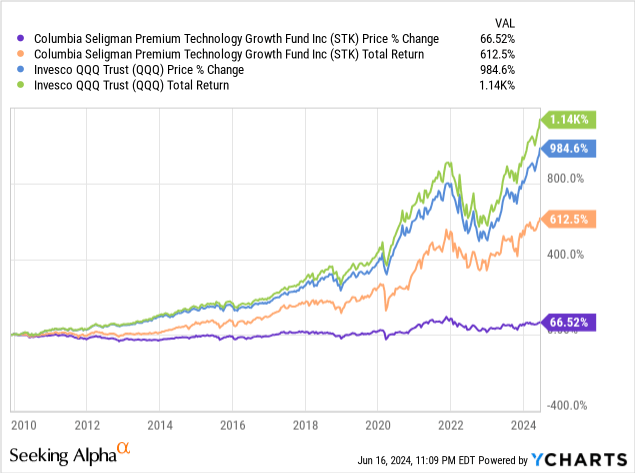

If you are not an investor that absolutely needs the income generated from your portfolio, and you’d rather focus on obtaining the highest total return, you may be doing yourself a disservice by buying into shares of STK. While STK has the compounding power to help growth your dividend income over time, the inclusion of the option strategy also means that some upside is likely being limited. Therefore, I would expect more traditional technology focused funds such as Invesco QQQ Trust (QQQ) to outperform over longer periods of time.

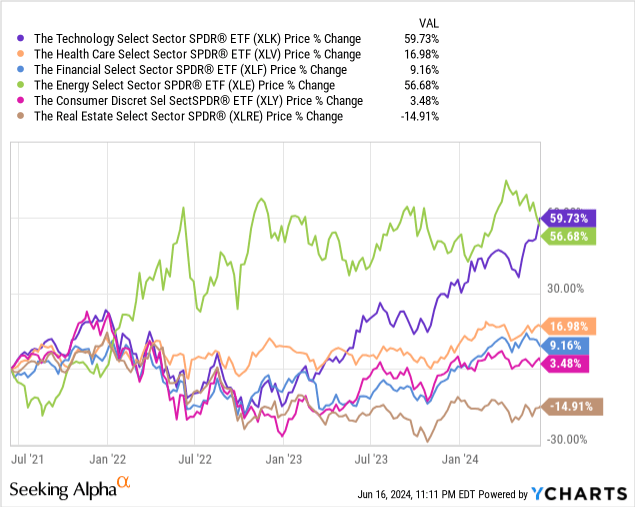

Additionally, STK does maintain a very small portion of real estate exposure. Real estate has been one of the hardest-hit sectors because of its sensitivity to interest rate changes. We can see that the real estate sector (XLRE) remains one of the only sectors that has failed to produce price upside since interest rates started to get hiked. While STK’s exposure is small, the weighting it does have may be suppressing the price movement and taking away from the price gains of other areas of the portfolio.

Lastly, the majority focus on tech works both ways. What I mean is that if the technology sector sees some huge downfall, the large concentration of the sector would leave STK holders vulnerable to the downward price movements. Since the other sectors which make up STK’s portfolio of holdings are so small, I fear that it would not be able to offset any potential losses that are experienced due to the tech sector.

Takeaway

In conclusion, STK’s methodology is unique by allowing flexibility with the option strategy and the inclusion of this helps enable a higher level of income generated in terms of a higher yield. STK seems more attractive now than when I previously covered it since it trades at a smaller premium to NAV of only 1.95%. The holdings shift includes NVDA now making up the largest weight percentage, as well as slight buffs to MSFT and AAPL. STK’s management has the flexibility to allocate more weighing towards companies that they believe are capable of capturing the most upside potential through new innovations and attractive valuations.

Additionally, STK has the ability to compound a dividend income stream when held over a long period of time. However, if you are an investor that is looking to make the highest total return possible, you would likely be better off with a more traditional fund such as QQQ since the option strategy can limit upside growth potential. In addition, this option strategy inclusion also means that the distributions received are likely to have tax consequences, which may not be the case for regular ETFs.

Read the full article here