It was a wild week for Tesla, Inc. (NASDAQ:TSLA) shareholders. Ark Invest published its updated investment thesis on TSLA with an expected value of $2,600 per share in 2029, and TSLA shareholders rallied around Elon Musk as his compensation package passed as 77% of shareholders voted yes on their shares.

At the TSLA shareholder meeting, Elon addressed shareholders and discussed how full self-driving (“FSD”) was improving exponentially, outlined how the Robotaxi network would work, and discussed how autonomy and Optimus could add $25 trillion of value to TSLA as a company. I am a recently reformed TSLA bear who just added to my position again on Friday, 6/14, after shares retraced below $180. The Optimus platform has made me a super bull as I believe it’s going to become vastly larger than its entire automotive infrastructure even after FSD and Robotaxis are brought to market.

While I can’t get behind the valuation Ark Invest has published for TSLA in 2029, even though it would make me a substantial amount of money, I am extremely bullish on TSLA’s future now that Elon has a reason not to leave. I now own 6 companies in the Magnificent Seven and believe that TSLA has the most upside potential if everything goes right. I think that shares of TSLA have established a bottom, and there are several catalysts on the horizon that can take shares higher in the 2nd half of 2024, especially the unveiling of the Robotaxi on 8/8/24.

Seeking Alpha

Following up on my previous article about Tesla

My last article about Tesla was published in April (can be read here), and since then, shares have appreciated by 9.32% compared to the S&P 500 (SP500), increasing by 6.82%. I had discussed how I was looking past the current earnings because of how impactful I believe the Optimus platform will be for TSLA and society. I am following up with a new article now that TSLA’s shareholder meeting has occurred and Elon’s pay package has been approved by shareholders. Furthermore, I will be discussing why I am more bullish on Optimus than Robotaxis, why I can’t get behind the outlook from Ark Invest, and why I am adding to my position as shares of TSLA trade at 71.94 times 2024 earnings.

Seeking Alpha

Risks to investing in Tesla

The biggest risk to TSLA was just eliminated, and that was CEO Elon Musk leaving the company. While investors are celebrating, and Elon just delivered an impactful presentation at the 2024 shareholder meeting, there are many risks for investors to consider. I believe that TSLA has the most upside potential in the Magnificent Seven, but nothing is guaranteed, as so many pieces must fall into place with the slightest margin of failure.

Now that Elon seems refocused and re-energized, the biggest risks are execution and legislation. On the EV side, TSLA needs to perfect FSD and build out the Robotaxi platform. They will also need approval on a federal level and local level for autonomous vehicles to operate in different jurisdictions. TSLA will also need insurance carriers to figure out how they will insure vehicles that are driven without a human driver and how policies will be impacted if an accident occurs.

On the robotics side with Optimus, TSLA could also face legislative hurdles on the enterprise side if companies such as Walmart (WMT) and Amazon (AMZN) start replacing a significant number of employees with robots. We could see legislation drafted and passed that companies can only offset their workforce with robots by a certain percentage. On the execution side, there is a large risk if these projects are delayed as much of TSLA’s bull thesis revolves around generating incremental revenue from FSD, taking a percentage of ride-hailing services through the Robotaxi network, and the implementation of Robotics into everyday life. For all the reasons why investors are bullish on TSLA, there are just as many reasons to be skeptical, as many things need to fall into place for the bull thesis to play out.

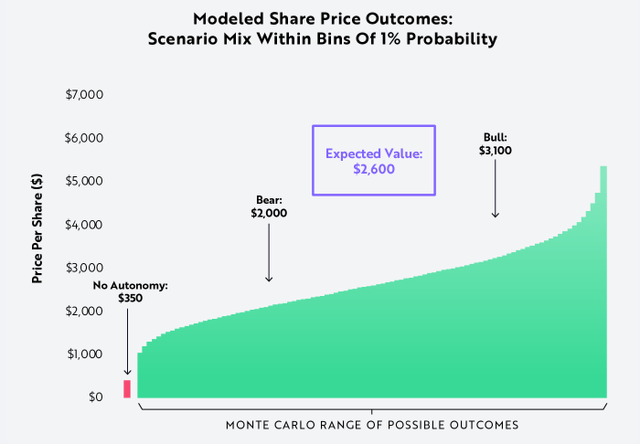

Ark Invest has a $2,600 base case for shares of Tesla in 2029, and I can’t get behind the numbers

As a TSLA shareholder, I would be ecstatic if shares traded for $2,600 in 2029. I truly hope that Ark Invest is correct. I am missing something, but I can’t back my way into their numbers with any degree of optimism. In their report (can be read here), ARK Invest estimates that nearly 90% of TSLA’s enterprise value and earnings will be generated by its Robotaxi business. The rest will consist of EV sales, energy, and insurance.

What I found quite odd is that the Optimus platform is not a key driver of their estimates, and Ark indicated that Optimus will have minimal impact on their targets. Ark Invest also excluded Tesla Semi, Supercharging Network, FSD Licensing, and AI-AS-A-Service from their model. In my bull thesis, Optimus is the largest focus, while FSD Licensing and the Supercharging network play significant roles.

Ark Invest

Ark Invest has placed a $7 trillion market cap on TSLA in their bear case at $2,000 per share, while their bull thesis has a market cap of $10.9 trillion at a $3,100 share price. In the bear case, TSLA would generate $853 billion in revenue ($250 billion EV, $603 billion Autonomous Ride-hail), and in their bull case, TSLA would generate $1.35 trillion in revenue ($394 billion EV, $951 billion Autonomous Ride-hail). Each scenario would have a 32% EBITDA margin, while the bear case would see a free cash flow (FCF) yield of 4.3%, and in the bull case, a FCF yield of 4.1% has been assigned.

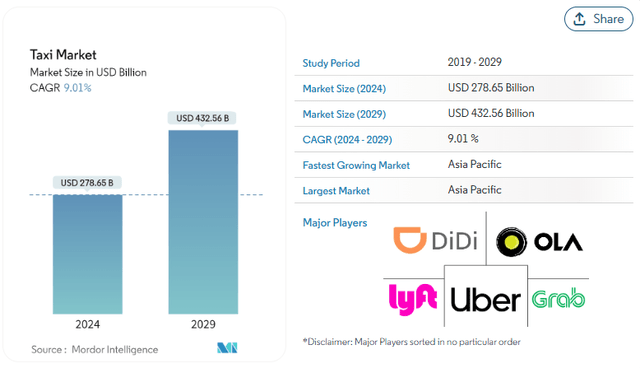

Mordor Intelligence

I cannot stress enough how much I want Ark Invest to be correct, but I can’t get behind their estimates. According to Mordor Intelligence, the entire global Taxi market, including Uber, Lyft, and DiDi is expected to be $278.65 billion in 2024 and grow to $432.56 billion in 2029. For either of Ark Invest’s revenue projections to materialize, TSLA would need to control 100% of the taxi market and have a substantial amount of car owners sell their vehicles and elect to utilize the Robotaxi network for transportation. Even if TSLA didn’t control 100% of the Taxi market, they would still need numerous car owners to elect not to pay for a vehicle and insurance and then allocate that money to use the Robotaxi network.

I have a hard time getting behind the idea that TSLA is going to generate between $603 billion and $951 billion from autonomous driving, considering that would be more than double what the entire taxi market is expected to generate in 2029. The fact that FSD licensing isn’t even part of this thesis makes the revenue projection from Autonomous even harder for me to wrap my head around. Part of my bull thesis is that rather than developing and maintaining their own network, Ford (F), General Motors (GM), and Stellantis (STLA) will license FSD from TSLA, and TSLA will generate reoccurring revenue from every sale in addition to ongoing monthly revenue from the software package.

I compared Ark Invests numbers to what the rest of the Magnificent Seven are generating in the Trailing Twelve Months to see what the valuations look like, and this is where things get even more mystifying for me. TSLA currently has a 12.95% EBITDA margin and a 1.46% FCF yield. Ark Invest is expecting TSLA’s EBITDA margin to increase by 247% by 2029. In the bear scenario, TSLA would grow its EBITDA by 21.26x in the next 5 ½ years to $272.96 billion, and in the bull scenario, TSLA would grow its EBITDA by 34.09x to $430.4 billion from the $12.27 billion they have produced in the TTM. I just don’t think this is probable.

On the other hand, I think TSLA should have no problem getting their FCF yield to 4.3% over the next several years. Hypothetically, if TSLA did come in with a FCF yield of 4.3% and ARK’s revenue estimates were achieved, TSLA would generate $36.68 billion of FCF in its bear case and $55.15 billion of FCF in its bull thesis. I believe these FCF numbers are much more achievable than the EBITDA projections, especially since TSLA generated $7.56 billion of FCF in their 2022 fiscal year, which was a 9.28% FCF yield on the $81.46 billion of revenue produced.

On a valuation perspective, there are already 3 companies, Apple (AAPL), Microsoft (MSFT), and Alphabet (GOOGL), that are generating more than $60 billion in FCF, and none of them have a market cap that exceeds $3.3 trillion. In the TTM, GOOGL has generated $69.11 billion in FCF and trades at a multiple of 31.74x, while AAPL generated $101.92 billion in FCF and trades at 31.97x, and MSFT generated $70.58 billion in FCF and trades at a FCF multiple of 46.61x. ARK Invest is estimating that if TSLA is generating $36.68 billion in FCF the market will assign a 190.84x multiple to it, and if TSLA generates $55.15 billion in FCF they will get a 181.34x multiple on its FCF.

Anything can happen, and I want TSLA to get to a $10 trillion market cap, but I don’t believe they will have a $10 trillion market cap generating $55.15 billion in FCF, considering AAPL, MSFT, and GOOGL trade nowhere near this valuation and all generate over $60 billion in FCF. Not even Nvidia Corporation (NVDA) trades anywhere near these levels, as the market has assigned a 78.49x multiple on its $41.33 billion of FCF because of its unprecedented growth.

I truly wish that Ark Invest had incorporated Optimus, Supercharging, FSD licensing, energy, and AI-As-A-Service as part of its bull thesis. TSLA has so many more revenue streams to pull from, and I think this is a business that needs to be looked at as a sum of the parts rather than excluding important areas. I think TSLA has the most potential of any stock in the Magnificent Seven, and I think Elon could be correct that TSLA one day gets to a $30 trillion market cap, but I don’t think TSLA sees a $10 trillion valuation without all of its businesses being factored in and playing a critical role in TSLA’s future success.

Steven Fiorillo, Seeking Alpha

Why I went from Bear to Bull and just added to my position

As a relatively new shareholder, my biggest concern was shareholders not approving Elon’s pay package, and he either left or allocated less time to running TSLA. Without Elon at the helm, I would have exited my position immediately, regardless of who had taken over, as I wouldn’t have felt confident that even half of the roadmap would have been brought to market. I increased my position on 6/14 after the 2024 shareholder meeting because I am confident that Elon and his team will bring FSD and Optimus to market and that they will have a dramatic impact on society and TSLA itself. What I find interesting is that my bull thesis revolves around the opposite factors than what Ark Invest is basing theirs on.

Tesla

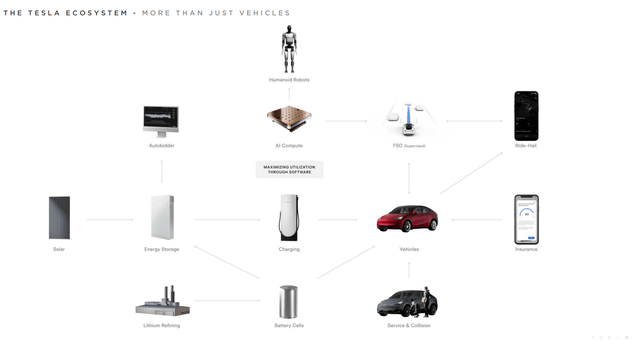

The TSLA ecosystem is so much more than Robotaxis and Ride-Hailing, and I believe that Robotaxis will be the hardest to capitalize on. AI is front and center, and for AI to work, it will require more infrastructure and electricity. There are estimates that 21% of the electricity produced globally will be allocated toward computing and communications technology by 2030, while Forbes indicated that the energy requirements for data centers powering AI utilize similar amounts of energy as small cities.

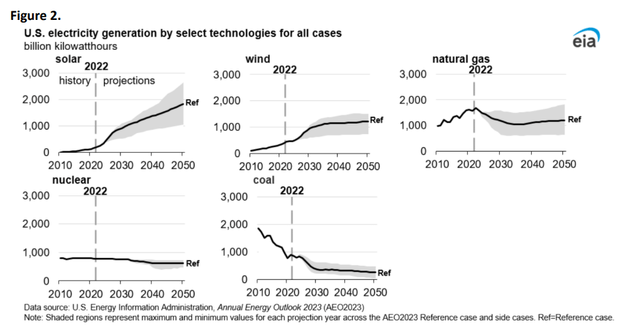

TSLA’s energy business is scaling and driving gross profit margins. Energy generation and storage are TSLA’s highest margin businesses currently, and their storage deployments increased to 4.1 GWh in Q1. TSLA’s Energy generation and storage business segment generated a gross profit margin of 24.65% as it generated $1.64 billion in revenue in Q1, and the cost of revenue was $1.23 billion. In the most recent U.S. Energy Information Administration (EIA) Annual Energy Outlook, the amount of electricity produced from solar is expected to increase by roughly 3x by 2030 while generation from wind is expected to double.

As more AI infrastructure is needed and more EVs are on the road, the demand for energy is expected to grow. I think that TSLA’s energy business could be flying under the radar as there will be a large demand for their Megapacks and solar panels. TSLA is also expected to get into the software side of deploying and selling generated energy from renewable sources. This side of the business has generated $6.14 billion over the TTM, and there is no reason why this can’t turn into a revenue stream that generates more than $20 billion on an annualized basis as more solar and wind are deployed. At $20 billion in revenue with the current gross margins, the Energy generation and storage business would generate $1.51 billion in gross profit alone. TSLA could also build a large-scale utility business where they can sell back the energy they produce from operating their own solar farm to the largest data center markets in the U.S.

EIA

FSD and the Supercharger network are a large component of my bull thesis. In 2023, there were an estimated 1.2 million EVs sold in the U.S., and TSLA accounted for 55% of the market. Ford (F) sold 72,608 EVs in 2023, which was an increase of 18% YoY. TSLA has 6,249 supercharger stations equipped with 57,579 superchargers. They also have an additional 40,000 wall connectors at destination charging sites. As companies such as Ford (F) adopt TSLA connector, they will be able to utilize TSLA’s supercharger network across the country. I think it’s likely that Ford and others, such as General Motors (GM) will license TSLA’s FSD package rather than building and maintaining their own. The FSD package currently costs $8,000 with a $99 monthly subscription. Hypothetically, if TSLA were to wholesale FSD to Ford, GM, and other manufacturers at $4,000 upfront and then charge the consumers $99 per month, it would be a home run.

Based on the current 2023 numbers, outside of TSLA’s portion, there were roughly 540,000 EVs sold in the U.S. If TSLA were to get 50% of these EVs on a licensing deal at $4,000 per unit, it would generate $1.1 billion in revenue. They would also generate an additional $320.76 million from the $99 subscription model. While this is just a hypothetical scenario, it is entirely possible that TSLA could generate billions in annualized revenue from licensing deals in addition to selling directly to their own customers as the EV market expands.

Out of everything TSLA is doing, I am the most bullish on Optimus. Elon recently said that Optimus could add $25 trillion in value to TSLA, and I think he is correct. At a $20-$25,000 price point, I think there are many homes in America and across the globe that would purchase Optimus if it could do laundry, clean, and mow the lawn. Some people have argued this point with me, but my theory is that Optimus will be able to be financed over a 5-year period the same way as a TSLA EV. Over a 5-year period, if the price was $22,500, the monthly payment would be $375-$425, depending on the interest rate. People have realized that the most valuable asset is time because we can never get it back.

I will be purchasing Optimus when it can do these tasks without a question, I’ll probably purchase more than 1 as I will get one for my parents also, so they can enjoy retirement without having to do household chores. On the enterprise side, I can envision a scenario where corporations such as United Parcel Service (UPS), FedEx (FDX), Walmart (WMT), Amazon (AMZN), and Home Depot (HD) utilize Optimus for many labor-intensive jobs such as packing and unpacking pallets in the warehouses. This doesn’t include the number of businesses that will be created utilizing bots, from commercial cleaning to landscaping.

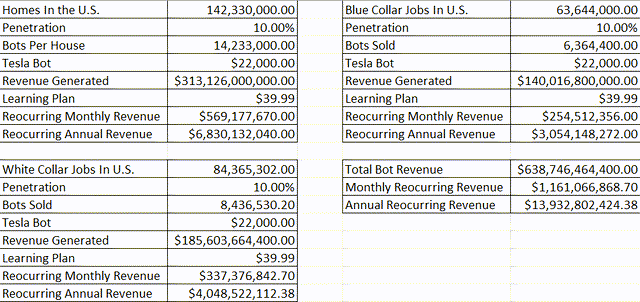

There are roughly 63.6 million blue-collar jobs, 84.37 million white-collar jobs, and 142 million homes in the United States. If TSLA grabs a 10% market share and implements a $39.99 per month learning plan where each Optimus is hooked up to the TSLA network and learns as each task from each robot is performed, not only will they get better by the minute, TSLA will generate a tremendous amount of revenue. In the U.S. alone, that could be worth $638.75 billion in revenue from the sale of Optimus and $13.93 billion in reoccurring annualized revenue from the learning plan. This is also a business that is scalable worldwide, and the difference between TSLA and everyone else is that TSLA has the engineering proficiency to mass produce Optimus and independent locations from which to sell them.

Steven Fiorillo

The analyst community has TSLA trading at 35.57 times 2027 earnings and 19.35 times 2030 earnings. TSLA is only expected to earn $2.54 per share in 2024, putting them at a 71.94 P/E. If you want to value TSLA on what they are doing today, the stock looks expensive. This is what I got wrong for so many years, and I am more than willing to admit it, as I am not sure if there is a good way to actually value TSLA today. So much depends on what they bring to market, legislation, and adoption throughout the marketplace. I also don’t believe that many of the analysts have Optimus priced into their valuation models.

As a long-term investor, I have no problem holding TSLA until 2040 or beyond. Some may think that’s crazy, but holding a stock for decades is quite normal for some. It’s entirely possible that Elon is correct in his vision, and I am investing in TSLA because I see mass adoption playing out in Optimus’s enterprise and consumer sectors. If Elon can continue to pull off what others constantly said wasn’t possible, then TSLA could reach a $10 trillion valuation at some point, and potentially more.

Seeking Alpha

Conclusion

I can breathe much easier now that the shareholder meeting is over and Elon’s pay package passed by a super majority. Investing in TSLA is definitely not for the faint of heart, as the stock may look expensive based on the current fundamentals, but the future potential is off the charts. A lot has to go right, and part of TSLA’s future success will depend on how regulation is crafted and implemented, so there are many risk factors to consider.

As a reformed bear, I am now super bullish on TSLA, and it’s predominantly because of Optimus. I agree with Elon and believe that Optimus will be larger than anything else TSLA does. If Ark Invest is correct with Ride-Hailing, then my bullishness won’t be enough, as I am still skeptical about that segment. While TSLA is probably the most risky due to uncontrollable variables, I believe it has the most upside potential out of the Magnificent Seven, and I intend to be a long-term shareholder. My only regret is that I wasn’t this late to the party, but I am glad I came later rather than not investing.

Read the full article here