In a previous report, I analyzed Thales S.A. (OTCPK:THLEF), which is a company that has quite a broad area of activity. The company is active in aerospace & defense, but also has other areas of activity including digital security, transportation, and communication. I have a buy rating on Thales stock, but since my first report covering the stock shares have only gained 1% compared to 8% for the broader market. Today’s stock price movement which removed almost 4.5% does not help the stock price performance.

I believe that in the European aerospace and defense industry there is significant upside, as the focus currently primarily is on U.S. peers, which I would attribute to investing being less embedded in income generation in Europe. What also does not help is that in Europe some companies report every quarter on order intake and sales, but a more complete view on profitability is only provided every six months.

In this report, I will be discussing the Thales H1 results, the outlook for 2023, and a stock price target for Thales.

Thales: A Diversified Aerospace Giant

ESA

Thales SA is a France-based technology company. It provides a wide range of solutions divided into three segments: Aerospace, Transport and Defense and Security. Aerospace provides onboard electronic equipment designed to increase flight safety and reliability, civil and military aircraft simulators, onboard connectivity and in-flight entertainment, onboard equipment and functions for aircraft piloting, navigation, and control as well as equipment, payloads, satellites, systems, and services for the space sector. Transport offers railway signaling, telecommunications, supervision systems, and ticketing solutions. Defense and Security offers radio communications products, network and infrastructure systems, protection systems, critical information systems, and cybersecurity.

When discussing a company, I always try to describe some of their core end markets or platforms. With Thales, that is difficult for the simple reason that it is such a big company with a diversified platform base. To give you an impression, the company is the #1 provider of air traffic management solutions, over 40% of the world’s aerospace is managed by Thales, and the company is the worldwide number 3 in avionics and the number 1 in Europe. In defense, the company says it is the global number one in air C4I (Command, Control, Communication, Computers, and Intelligence) and advanced air defense and the #1 in defense electronics in Europe.

So, it is highly likely that either when traveling by train or airplane you either touched something that was made by Thales, or some electronics either on the vehicle or the associated management system had a product from Thales involved, all while its defense solutions play an integral role in keeping everyone safe. That already sounds like something big that would be interesting for investment.

Key Metrics For Thales In H1 2023

Thales

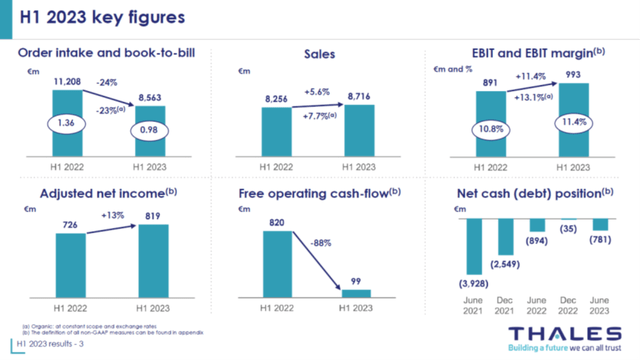

Before diving deeper into the H1 results, we first take a helicopter view on the key metrics. Order intake declined by 23% on organic basis, but this was driven by strong order inflow last year as the order for 80 Rafale fighter jets was added to the backlog of Dassault (OTCPK:DASTY), which also benefited Thales. Furthermore, the orders for Thales tend to be backloaded, so with a book-to-bill ratio of 1, there is confidence that this ratio will increase to >1 in the second half of the year. Organic sales growth was 7.7% despite a 1 percentage point forex headwind, and profit grew even faster at 13.1%, which is the same growth we saw in adjusted net income.

Where things did get worse for Thales is cash flow and net cash or debt position. The free cash flow declined by €821 million, and this was primarily driven by working capital requirement as Thales builds stock for critical components and materials to navigate ongoing supply chain challenges and due to inflation the input costs are higher. Furthermore, the CapEx increased to €272 million. So, H1 free cash flow was impacted by building stock but should normalize in the second half of the year.

Thales

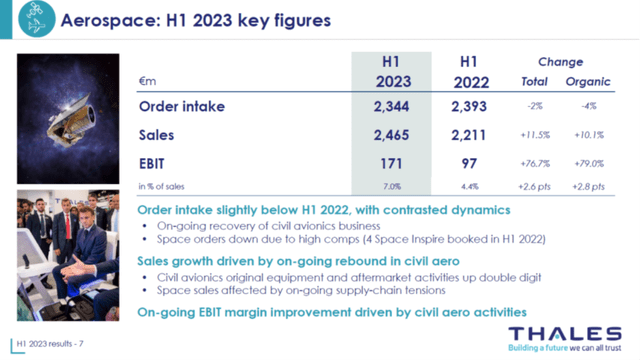

In Aerospace, order intake declined by 4% organically, but sales were up 10.1% on continued strength in in civil aerospace and aftermarket sales which also pushed the profit 79% higher and provided a 2.8 pts tailwind to margins. Within Aerospace, Space saw orders decline and suffered continued supply chain challenges, but things should be improving in the second half of the year.

Thales

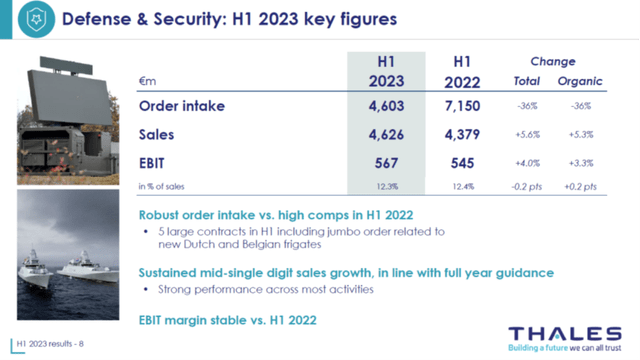

The Defense segment saw order intake decline by 36% which was driven by the Rafale order from the UAE in 2022. Excluding that order, order intake was comparable year-over-year with strength in frigate related orders. Sales grew by 5.3 percent on stable margins. So, Defense showed modest growth.

Thales

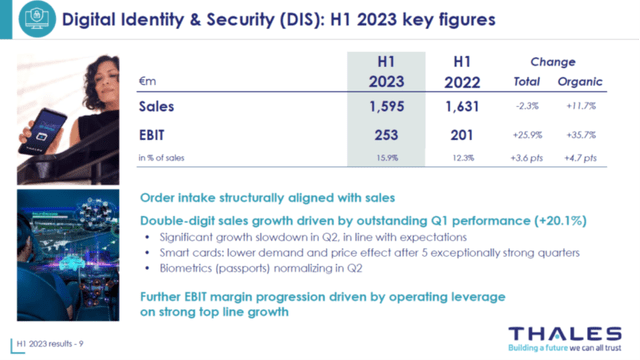

The Digital Identity & Security segment saw 11.7% growth in sales and a 35.7% increased in EBIT on an expanded margin. This pace of growth is, however, not set to continue as smart cards sales will be lower in H2 and the decline already started to Q2 and biometrics services will normalize against a higher comp. At the time of writing, the news just came in that Thales will be acquiring cyber security specialist Imperva in a deal worth $3.6 billion that will accelerate the sales growth as well as its margins.

Thales

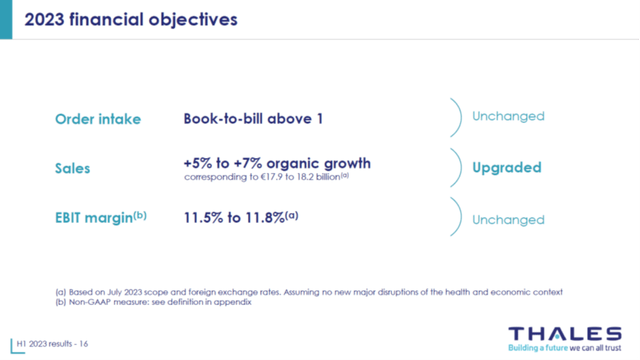

Despite €250 million to €300 million in forex headwind for the full year and supply chain challenges, Thales is still aiming for a book-to-bill above 1, and now aims for 5 to 7 percent organic growth and a 11.5% to 11.8% margin.

Is Thales Stock A Buy?

The Aerospace Forum

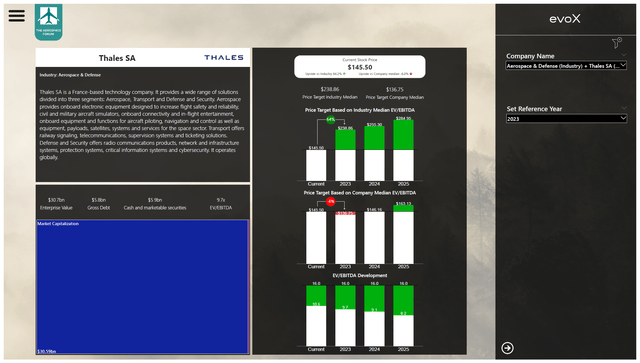

The news about the acquisition of Imperva is still too fresh to incorporate in our earnings and also has to be approved, so for now I will be providing my price target for Thales excluding the Imperva acquisition. What I like about Thales is not just their defense and commercial aviation exposure, but the fact that they also play an important role in connectivity and digital security. The company has a low net debt and pays a dividend.

Compared to its median EV/EBITDA, there is admittedly no upside when inserting the numbers into our evoX Financial Analytics model available to our subscribers. However, that ignores the prospects the company has in the current defense budget landscape, and compared to aerospace peers it is significantly undervalued which tend to have a 16x multiple while the digital solutions peers can trade at up to 25x EV/EBITDA. So, the EV/EBITDA of 9.7x for 2023 would suggest that the company is not at all valued in a way that reflects its peers or its prospects.

Conclusion: Thales Is An Attractive Business

Thales is a bit of an odd company to value because it is rooted in aerospace and defense as well as digital security, but its valuation is significantly lower compared to peers in both fields. While there are FX headwinds, scope changes and supply chain issues that result in higher working capital requirements, I don’t see any good reason why that should result in a 40% discount for Thales S.A. compared to peers in the aerospace industry. Furthermore, the newly announced cyber security acquisition that is set to close in early 2024 should positively affect the growth profile of Thales DIS segment. Even when we would value the company according to an Industrials sector company, there should be at least 25% upside from current Thales S.A. stock price levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here