Last quarter, in light of increasingly attractive fixed-income options and a renewed frenzy from retail investors, we became skeptical of some equity valuations. We began hedging our equity exposure by shorting a number of high multiple stocks, primarily in the technology sector. Unfortunately, this strategy proved quite costly as the stocks we believed were significantly overvalued increased at a rate far faster than our long holdings.

| Q2 2023 | Year to Date | Since Inception (Jan 21, 2020) | Since Inception CAGR | |

| TIDEFALL LP (Net) | -8.2% | -2.4% | 179.1% | 34.7% |

| S&P (Tr) | 8.7% | 16.9% | 41.3% | 10.6% |

| TSX (Tr) | 1.1% | 5.8% | 27.6% | 7.3% |

We have previously successfully hedged our portfolio during the initial covid crash in 2020 by shorting economically sensitive stocks and again in 2022 by shorting high multiple tech stocks. However, we have now covered all of our individual shorts. As a Portfolio Manager, I realize that I have been too distracted by short selling and need to focus more on asymmetric long ideas which is where I have excelled historically and where nearly all great fund managers over their career have made their returns. Although there are a number of individual stocks that we believe are trading significantly above their intrinsic values, it is far wiser to just ignore them, instead of betting on rationality returning any time soon. Live and let live.

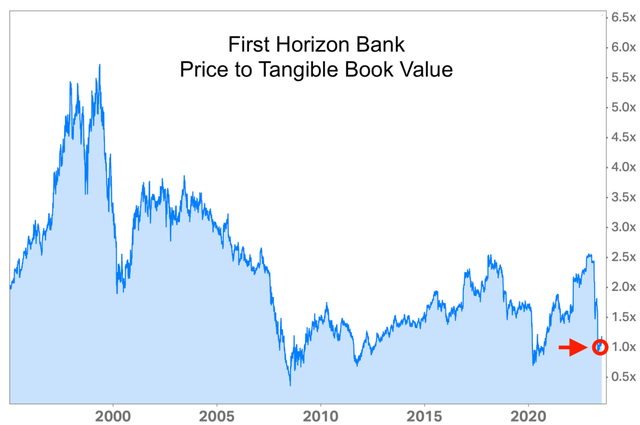

Thankfully, there are many old economies, and small-cap stocks that are trading at attractive valuations. Last quarter we took a small position in First Horizon Bank (FHN). Although the stock only has a $6b market capitalization, the name might be familiar to some Canadian investors since it was an acquisition target of TD Bank (TD) which agreed to purchase the company in February 2022 at $25 per share.

The rapid rise in interest rates over the past year, reduced the value of long-term bonds, creating a massive drop in the equity of some regional banks which led to fears of a bank run because customer accounts are only officially insured to $250,000. The large depositors at the most vulnerable regionals rapidly moved their savings to the larger “too big to fail” national banks. The resulting turmoil saw TD get cold feet and walk away from the acquisition of First Horizon (although TD officially blamed it on “regulatory uncertainty”). With the TD deal off, First Horizon stock then crashed alongside the regional bank sector to $10 per share; less than its tangible book value.

We believe First Horizon is being unfairly grouped in with its more troubled peers, despite having industry-leading metrics and capital ratios (which are further improved by TD’s $225m break fee payment). The bank is well funded with only 1/3rd of deposits uninsured and well diversified with the top 15 depositors representing just 1% of the total. First Horizon is focused in the US Southeast, which is experiencing 2.6x GDP growth and 4x the population growth versus the US national average. The two biggest investor concerns of US regional banks today are their bond portfolio losses and their exposure to office real estate (due to work from home). First Horizon performs excellently on both measures.

As previously mentioned, the US regional banking crisis was primarily caused by falling bond values. Thankfully, unlike recent bank failures, First Horizon has no significant bond losses hidden by held-to-maturity accounting (fair value vs book value for all assets is just a $383m difference or 4% of equity). With the termination of the TD acquisition, deposits have rebounded strongly with the company having its best month in May with deposits increasing by nearly half a billion dollars. In regards to wider regional banking concerns, we do not believe that US regulators and both political parties are willing to risk a widespread banking collapse, and should even larger fears reemerge, they will quickly step into preemptively insure all deposits.

In regards to commercial real estate, First Horizon has minimal exposure with just $2.8b in office loans outstanding, representing 21% of their CRE loan portfolio and 3% of total assets. Nearly half of this exposure is medical offices which have traditionally been recession resistant. Furthermore, the remaining non-medical office loans are also conservatively financed with a 59% loan-to-value ratio.

We acquired our shares in First Horizon below tangible book value and at 6x trailing earnings. With the exception of the depths of the GFC in 2008 and the initial covid panic in 2020, this is the cheapest the stock has traded on these metrics in the past 30 years. Even with the Fed tightening and a possible recession, we believe this is an attractive valuation in light of our expected long-term mid-teens return on equity. Five directors have acquired shares in the open market since the merger was called off in May, with no insider sales.

Trevor Scott

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here