This is my inaugural take on United Therapeutics (NASDAQ:UTHR), a commercial stage biotech with long growing earnings and a nice product portfolio. Its lead product generates more than 50% of its revenues. It has been fighting tooth and nail to prevent competitive products from entering the market.

So far, it has been successful in this respect; however, it is running out of options to continue this fight. In this article, I will discuss the general investment merits of United Therapeutics and its big competitive challenge.

In this article, I will reference its Q1, 2024:

- earnings call (the “CALL“);

- 10-Q (the “10-Q“);

- presentation (the “PRESENTATION“).

I also include several references to its latest 10-K (the “10-K“)

With increasing revenues, United Therapeutics has grown its market cap to ~$12 billion

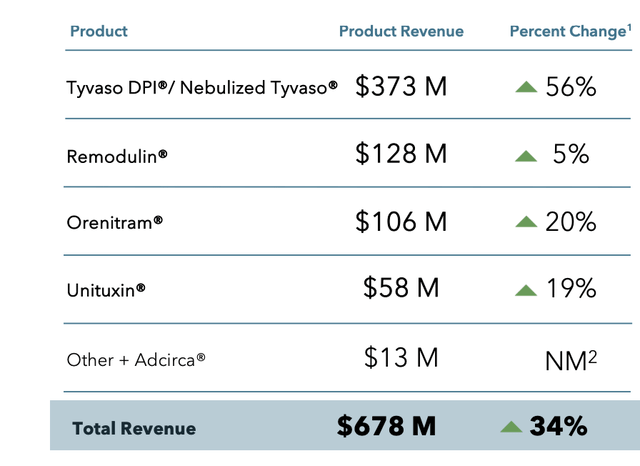

The excerpt below from presentation slide 10 sets out United’s Q1, 2024 product revenues with their percentage change from Q1, 2023:

ir.unither.com

Each of its top four products are in strong double-digit growth mode, with only Remodulin lagging in single digit growth. The Tyvaso (treprostinil) DPI and Nebulized pair lead United’s product franchise growth rates by a good margin. They are its largest revenue producer, making up more than 50% of overall product revenue.

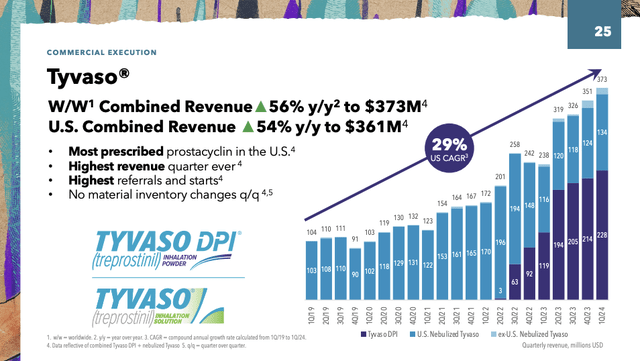

PRESENTATION slide 25 below provides a longer range view along with more overall granularity on this key product pair; this chart is helpful in distinguishing between the two available formats of Tyvaso.

ir.unither.com

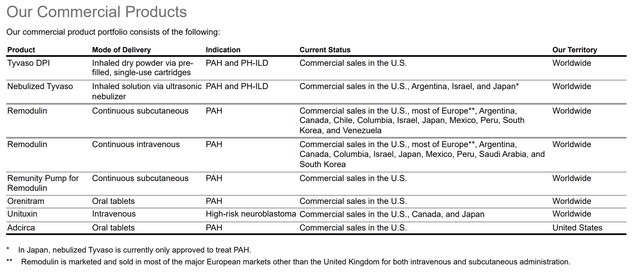

The following chart from the 10-K (p. 3) sets out key data for United Therapeutics’ commercial product franchise:

seekingalpha.com

It also shows how highly concentrated its medicines are in treatment of pulmonary arterial hypertension [PAH] in its various manifestations. As stated on United’s website:

PH-ILD stands for pulmonary hypertension associated with interstitial lung disease, a serious and progressive disease.

In terms of its near and intermediate future, its ambitions are limited, as reflected by the chart below from the 10-K (p. 8):

seekingalpha.com

IPF and PPF refer to two different manifestations of pulmonary fibrosis, idiopathic and progressive, also addressing lung diseases.

Moving to a more distant horizon, United Therapeutics’ ambitions explode to the highest of high-tech

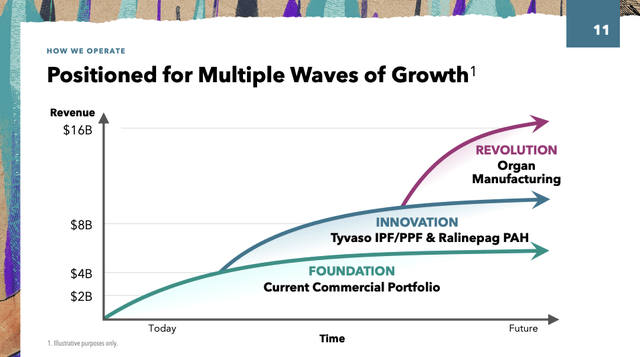

PRESENTATION slide 11 illustrates the full extent of United’s ambitions:

ir.unither.com

Over the next indeterminate medium-term future, it is satisfied with its pulmonary focused franchise. It pegs this as pointed towards revenue generation, aggregating $8 billion.

It provides no product breakdown or helpful timeline for achieving this goal. Accordingly, it is a weak underpinning for an actionable calculation, particularly when one considers its competitive environment as discussed below.

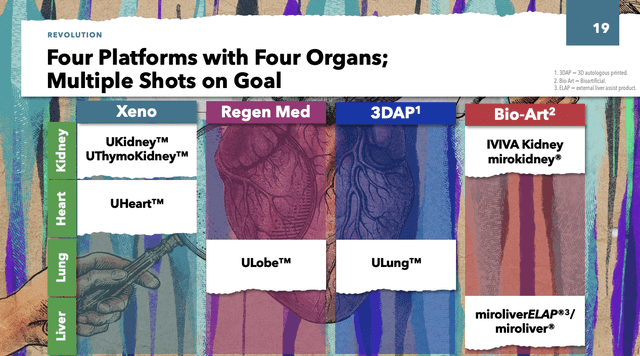

On a longer-term basis, slide 11 references “REVOLUTION Organ Manufacturing”; it pegs upwards of $16 billion in revenue generation potential. This seems to be the stuff of science fiction. United Therapeutics is seriously focused on advancing its technologies into the clinic and beyond.

PRESENTATION slide 19 summarizes the breadth of its programs directed towards this end:

ir.unither.com

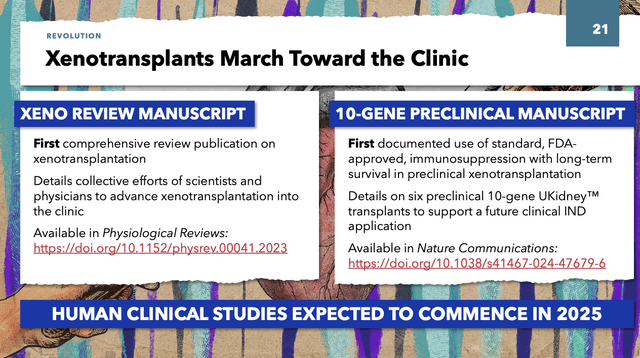

PRESENTATION Slide 21 captioned “Xenotransplants March Toward the Clinic” focuses on what I presume to be its most advanced organ program:

ir.unither.com

With human clinical trials not expected to begin until 2025, this program is obviously in early days.

Feisty competition raises ugly question marks as to Tyvaso’s future

Tyvaso is United’s largest grower by a giant margin. New competition in this market can’t help but damage United’s prospects. It has been fighting such threats for a long time. A strongly worded article by a Seeking Alpha analyst earlier this year posited Liquidia’s (LQDA) YUTREPIA as a particularly dangerous competition.

United has been fending off this threat with some success since back in 2020. Its 10-Q devotes a full page under the heading “Litigation with Liquidia Technologies, Inc” explaining this complicated battle. The explanation is replete with obscure technical terms that defeat ready summarization.

There are multiple lawsuits covering multiple patents, with multiple motions, rulings on motions and judgements and appeals. It is difficult to assess when competition will start to hit home. In Liquidia’s Q1 2024 earnings call, it explains how it is fully ready to launch its YUTREPIA as soon as it is freed from its legal restraints.

Judging by a recent Seeking Alpha news report after hours on 05/31/2024 the time when it may face competition is drawing inexorably closer. Most recently, a district court denied United Therapeutics’ request for a preliminary injunction over Tyvaso competitor YUTREPIA.

During its recent conference call, Liquidia was confident that YUTREPIA’s mechanism for delivering treprostinil was superior to both those available for Tyvaso. Liquidia CEO Jeffs noted it is not the molecule treprostinil which leads to discontinuance of use but rather its administration. It believes:

…physicians and patients are eager for a new choice, one that delivers a readily titratable and durable inhaled formulation of treprostinil using a portable, patient-friendly, low-resistance dry powder inhaler with demonstrated high patient preference and satisfaction. YUTREPIA is that choice and has the very real potential to become the first in choice in best-in-class process cyclin in this growing market opportunity.

Conclusion

Effective 06/01/2024 United Therapeutics scores a buy on its metrics as calculated by Seeking Alpha’s Quant ratings with a B+ for value, a C+ for growth and an A+ for profitability. I would normally be loath to demur from such a ranking.

However, in United Therapeutics’ case, the uncertainty attendant upon its long battle with YUTREPIA gives me pause. Tyvaso is both its >50% revenue generator and its strongest grower.

YUTREPIA provides credible threats to both metrics. United has been holding it sufficiently at arm’s length to protect itself from serious revenue impact for many years. The time will come when this tactic will no longer be effective.

I submit that the time is sufficiently close to render United Therapeutics unattractive for new money. Accordingly, I rate it a Hold.

Read the full article here