- This is my third UroGen Pharma Therapeutics (NASDAQ:URGN) article after 03/2023’s “UroGen: All Eyes On UGN-102 (“Eyes”). I concluded the article, noting that:

Those interested in this name will be attuned to its ENVISION DOR data expected for release in Q2, 2024. Assuming positive data the next point to watch for will be an FDA submission late in Q3, 2024. Next will be the FDA’s response to UroGen’s NDA; did it accept the filing and grant priority review?

Now we are in Q2, 2024. True to its word on 06/13/2024 publicized extensive data on its ENVISION trial including:

- a press release captioned “UroGen Announces Unprecedented 82.3% Duration of Response at 12 Months in the ENVISION Trial Investigating UGN-102 as Potentially the First FDA-Approved Non-Surgical Treatment for LG-IR-NMIBC” (the “ENVISION Release”) and

- a 57-slide presentation titled “New Horizons in Bladder Cancer: UGN-102 Duration of Response Results from the ENVISION Study” (the “ENVISION Presentation”)

In this article, I evaluate UroGen’s investment merits considering both the above and its Q1, 2024 earnings as reported during its earnings call (the “CALL“).

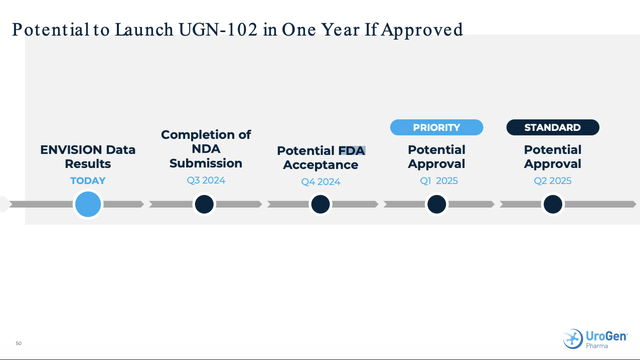

The ENVISION Release and Presentation map out UroGen’s planned FDA filing timeline.

The ENVISION Release reports:

In January 2024, UroGen initiated the submission of a rolling New Drug Application (NDA) to the U.S. Food and Drug Administration (FDA) for UGN-102 as a treatment for LG-IR-NMIBC. The latest DOR data are expected to support the UGN-102 NDA, which the Company plans to complete in the third quarter of 2024, with a potential FDA decision as early as the first quarter of 2025.

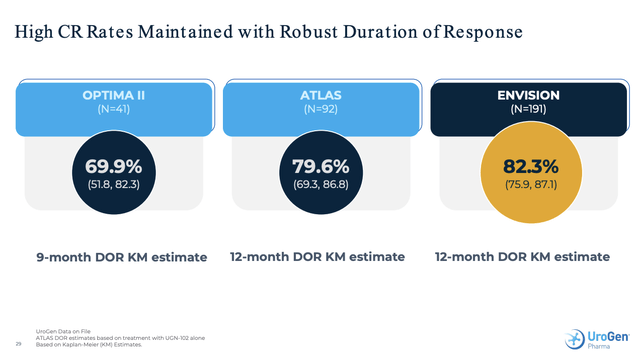

The ENVISION Presentation includes multiple slides addressing UGN-102’s Duration of Remission (DOR), as listed below:

- slide 21 – titled “ENVISION Single-Arm Pivotal Study Description” noting DOR was a key secondary endpoint, defining it as time from first documented CR until the earliest date of: Recurrence; Progression; Death;

- slide 23 – titled “DOR: 82.3% at 12 Months, Overwhelming Majority Remain Disease Free, followed by support graph and table;

- slide 24 – titled “Large Sample Size Resulted In Tight DOR Confidence Intervals”;

- slide 25 – titled “Median DOR Not Estimable Due to Patients Remaining in CR”

- slide 26 – titled “Predicted Median Duration Of Response (DOR) is 40.0 Months”.

The ENVISION Presentation also includes slide 50 which provides a timeline for its anticipated FDA filing and launch of UGN-102, anticipating a Q3, 2024 NDA filing:

investors.urogen.com

The likelihood of UGN-102 (mitomycin) receiving priority review is a known unknown. Uro-Gen’s JELYMYTO was granted priority review. However, the FDA had already given it Orphan Drug, Fast Track and Breakthrough Therapy designations. The FDA has not done so for UGN-102.

UGN-102 has met its primary endpoint in each of its three late-stage trials.

ENVISION is UroGen’s second successful completed phase 3 trial for UGN-102 in treatment of Low-Grade Intermediate-Risk Non-Muscle Invasive Bladder Cancer. The first was its ATLAS trial (NCT04688931) summarized on clinicaltrials.gov as a:

…global, randomized, controlled, open-label Phase 3 study … designed to assess the long-term efficacy and safety of UGN-102 (mitomycin) for intravesical solution with or without (±) transurethral resection of bladder tumors (TURBT) versus TURBT alone for the treatment of patients with low-grade intermediate-risk non-muscle invasive bladder cancer (LG-IR-NMIBC).

ATLAS with 282 enrolled patients had an actual study completion date of 03/17/2023.

The ENVISION trial’s (NCT05243550) clinicaltrials.gov summary provides:

This Phase 3, multinational, single-arm, multicenter study will evaluate the efficacy and safety of UGN-102 as primary chemoablative therapy in patients with low grade intermediate risk non-muscle-invasive bladder cancer (LG IR NMIBC).

ENVISION had an estimated 220 enrolled patients with an actual study primary completion date of 04/26/2023 and an estimated study completion date of 02/2028.

ENVISION Presentation slide 3 gives an overview of its initial phase 2 UGN-102 trial (OPTIMA II, NCT03558503), ATLAS and ENVISION as follows:

investors.urogen.com slide showing Consistently High Complete Response Rate At 3 Months

This combination provides an excellent scaffold on which to base its anticipated NDA. UGN-102 met its primary endpoint in both of its phase 3 trials, as it did in OPTIMA II.

Uro-Gen has high ambitions for UGN-102, pegging it as a mega-blockbuster.

During the Call, CEO Barrett talked up the benefits of UGN-102. She advised that it would do away with standard of care repetitive bladder resectioning TURBT surgeries for low-grade intermediate-risk non-muscle invasive bladder cancer. It would replace them with a “minimally invasive routine non-surgical option”.

She went on to note that its:

…research reflects overwhelming support from both urologists and patients with the intent to use by over 90% of survey urologists and over 90% of surveyed patients in the ENVISION study preferred UGN-102 to a TURBT.

In terms of the market opportunity, she was unrestrained in her enthusiasm. She estimated it conservatively (her word, not mine) at $3 billion. In terms of cost, she said that initial analysis and market researched suggested pricing it in the $16,000 to $19,000 range per dose.

Barrett wasn’t the only executive weighing in on the benefits of UGN-102. CMO Schoenberg spoke to the benefits of its method of action. He noted:

…UGN-102[‘s] … innovative RTGel delivery mechanism … provides sustained release treatment directly to the bladder tissue for up to six hours. This extended dwell time facilitates treatment of both visible lesions and underlying abnormal cells that predispose to disease recurrence. This attribute is critically important because despite their expertise urologists may not be able to detect all such cells during surgical procedures. We believe UGN-102 offers a clinically meaningful improvement over surgery in reducing recurrence risk and prolonging disease-free intervals for patients while lowering the overall treatment burden on patients.

CCO Bova explained why UGN-102 would fit conveniently (for both urologist and patients) into routine office visits. He stated;

UGN-102 also has the advantage of being easy to administer, either by the doctor, nurse or extender, offering a substantial benefit in terms of patient and doctor convenience. This streamlined approach enhances the experience for the patient and simplifies the treatment process considerably.

Challenges aplenty await UroGen as it moves towards FDA approval for UGN-102.

General

It is always important to balance the pros and cons of an investment before moving ahead. This article has already pointed to sundry pros underpinning UGN-102, most notably its two successful phase 3 clinical trials and its $3 billion market potential. In this section, I will point to the countervailing cons.

Without minimizing any of the innumerable risks set out at pp 3-23 of UroGen’s latest 10-K, this article focuses on the following:

- financial risks

- approval risk

- marketing risks.

Financial risks

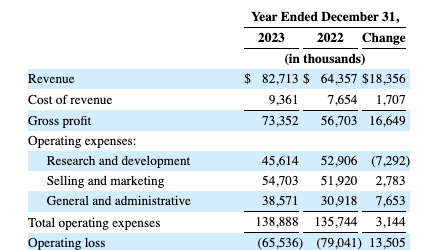

The table below from UroGen’s latest 10-K (p. 68) gives an overview of its financial operations:

seekingalpha.com

For 2024 in the CALL it is guiding for:

- net product revenue in a range of $95 million to $102 million and

- operating expenses in the range of $175 million to $185 million, including non-cash share-based compensation expense of $6 million to $11 million, subject to market conditions.

As of 03/31/2024 it had cash, cash equivalents and marketable securities of $164.5 million. It had a cash burn of $31.7 million for Q1, 2024. In terms of a cash runway, during the CALL it reported:

… Our latest financial projections, assumptions and sales forecast affirm our belief that our current balance sheet is robust enough to sustain our operations through anticipated breakeven. So we do not need to raise additional capital with our current plan.

Approval risk

With its NDA set to be filed in Q3, 2024, the issues with which I closed my discussion in Eyes come to the fore, to wit what:

…will be the FDA’s response to UroGen’s NDA; did it accept the filing and grant priority review?

I expect that the FDA will accept the filing, I have no opinion on whether or not it will grant priority review. As for the biggie, whether or not it will approve UGN-102, I am cautiously optimistic. The caution is born of many unexpected disappointments over the years, the optimism is based on the uniformly positive OPTIMA II, ATLAS and ENVISION results.

Marketing risk

If one assumes, as I think should be the case, but daren’t assume, that UGN-102 will be approved for marketing by the FDA, the next question is: How will it fare on the market? In this regard, I note the following from CCO Bova during the CALL:

For UGN-102, the pre-commercialization plan is well underway, targeting an early 2025 launch. As we get closer to the approval date, we will add a modest number of additional reps to our existing field sales force. There’s approximately a 95% prescriber overlap with JELMYTO and we plan on leveraging our commercial organization to execute a streamlined launch.

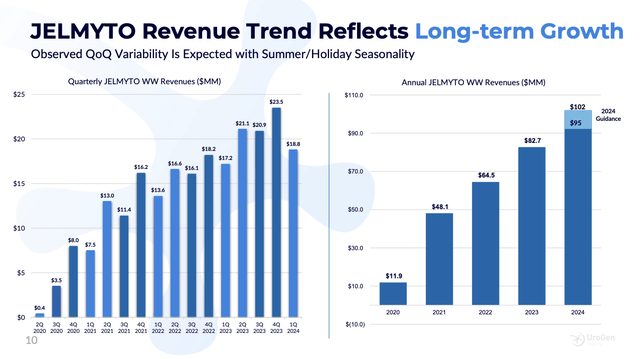

Certainly, that sounds admirably thrifty, but is it the wise choice? As shown by slide 10 from UroGen’s Q1, 2024 presentation, after four years on the market, JELMYTO’s revenues haven’t exactly set the world on fire:

investors.UroGen.com

Bulls have to expect UGN-102 to do far better. In fact, it will have some advantages over JELMYTO. Its use is simpler, reps will be more experienced and will have more than a single product to offer.

Conclusion

I rate UroGen as a Strong Buy. It stands a decent chance of reeling in a near term FDA approval. If it does so, it is quite attractive. It has adequate liquidity, and a potential of $3 billion in UGN-102 revenues; its current market cap of ~$700 million sets it up as a bargain.

Read the full article here