In May, the Federal Reserve (“Fed”) increased their benchmark rate for the 10th consecutive time to a range of 5% to 5.25%. That range marked a 16-year high. While the higher rates benefit some, such as cash holders and pension funds, it has proven to be a drag for most others.

With the June meeting on deck, the consensus view is that there will be a pause. In advance of this meeting, the S&P 500 (SPY) is up 4% over the past month, while the Nasdaq is up 8% over the same period, due primarily to the run-up in a select group of names. The Dow (DJIA), on the other hand, is up less than 2%.

Since there is a consensus on a pause, the market reaction will likely remain muted if that comes to fruition. But what will be more important is the commentary surrounding the future outlook. With the Fed set to meet again in July, it is my view that many participants have become complacent. While the pause is intended to provide time to assess their cumulative efforts, the window is short. And a strong labor market and an overall inflation rate still well-above targeted levels suggest the cycle still has a way to go. Any commentary following the decision to that effect, therefore, is likely to be viewed negatively. Given the outsized gains in several tech-focused stocks, the sector is viewed as being of heightened risk in advance of the meeting.

What Is The Current Economic Outlook?

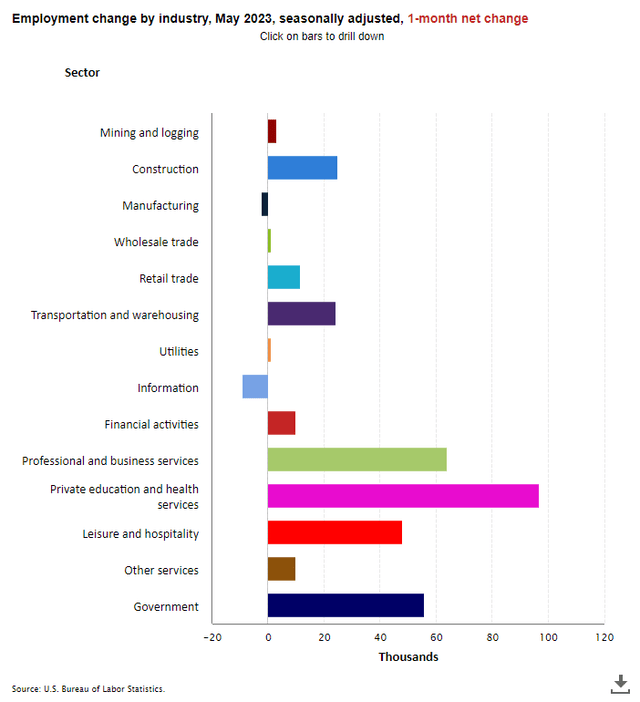

The strength in the U.S. economy has remained persistent. This is most clearly seen in the monthly unemployment report, which last revealed gains of 339K jobs in the month of May. This was nearly 150K greater than expectations. It was also an acceleration from the 294K added in April. The gains were also broad based across industry, with the exception of the information sector, whose losses were likely related to the writers’ strike.

U.S Bureau Of Labor Statistics – May 2023 Summary Of Job Gains By Industry

While data on retail spending is positive, the boots-on-the-ground reality is more mixed. In April, consumers boosted their spending for the first time in three months. In addition, reports on store traffic levels over the Memorial Day holiday suggested that the trends remain positive.

But recent reports from a wide swath of retailers indicated consumers were hesitant to spend in Q1 and choosier when they do. The sale of consumables, for example, figured more greatly into sales for diversified retailers, such as Walmart (WMT), as well as by discount stores, such as Ollie’s Bargain Outlet (OLLI) and Dollar Tree (DLTR). This is important, as these goods are lower cost to the consumer but lower margin items for retailers.

Despite the mixed picture between employment and retail sales, the World Bank still sees better than previously estimated global economic growth this year, due in part to a stronger U.S. economy, which remains propped up by strong levels of overall consumer spending.

How Are Markets Performing?

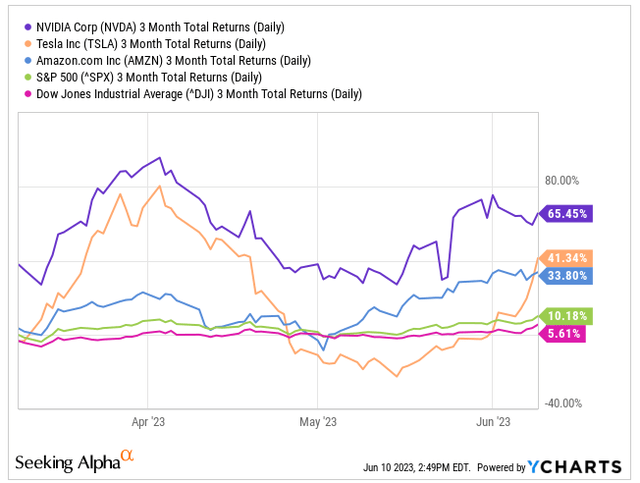

In the week ended June 9, 2023, the S&P secured its fourth consecutive weekly gain. And on the Thursday right before the end of the week, gains in several notable names, such as Amazon (AMZN), Tesla (TSLA), and Nvidia (NVDA), helped propel the S&P to the start of a new bull market.

YCharts – Summary Of 3-Mth Returns Of Select Tech-Focused Stocks In Relation To Broader Markets

With the gains in place, the S&P is now up 12% on the year. Though up, these gains are heavily skewed to just a few select names. When considered from an equal-weighted perspective as opposed to market capitalization, for example, the index is up just 2%. This disparity can also be seen in the DJIA, whose gains are also muted in relation to both the S&P and the Nasdaq.

Most of the gains pertain to newfound enthusiasm in tech-focused stocks due to the recent buzz surrounding generative AI. Whether these gains can hold is debatable. But one can reasonably surmise that this group is at heightened risk of a pullback due to their rapid run-up over the last several weeks.

Why Would The Fed Pause Their Rates Hikes?

The last rate increase represented the 10th consecutive increase. In some circles, this was viewed as too aggressive, especially when considered against the recent banking failures.

Board of Governors of the Federal Reserve System (US), Federal Funds Effective Rate [FEDFUNDS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FEDFUNDS, June 9, 2023.![Board of Governors of the Federal Reserve System (US), Federal Funds Effective Rate [FEDFUNDS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FEDFUNDS, June 9, 2023.](https://wealthbeatnews.com/wp-content/uploads/2023/06/49921492-16864230933514764.png)

Already, many small businesses have noted challenges in securing financing in the current environment. In addition, an increasing number of startups are failing due to an inability to raise money for their ventures. Furthermore, many lenders face additional threats resulting from a coming wave of potential defaults in more challenged sectors, such as office-focused real estate.

With the full consequences of these headwinds yet to play out in real time, many, understandably, want to wait and see how this fans out across the broader economic environment.

What To Expect Moving Forward?

A rate pause is just that. It doesn’t necessarily mean the Fed will be done with their campaign. But it, nevertheless, may suggest the cycle is near its end. It will also allow the cumulative effects of their past efforts to trickle through various subsectors of the economy.

Transactional markets in the real estate sector, for example, have been dry for numerous operators due to the wide bid/ask spreads between buyers and sellers. And much of this gap in expectations is attributable to the continuously evolving rate environment. Small businesses have also been disproportionally affected by the higher rate environment, with many experiencing longer wait times and tougher questions from their lenders. Delinquency rates on consumer loans, especially on auto-specific originations, have also been on the rise.

By pausing on further rate hikes, officials would get a closer look as to how these various shortcomings ultimately play out. The window to assess, however, won’t be long, considering the next meeting is in July. And at that time, it’s probable there will be an increase. Current estimates peg the chance of an increase then at 65%.

In my view, I see the chances as even higher, given inflation is still running well above targeted levels. The labor market also remains tight, as evidenced by the historically low unemployment rate, the surplus of job openings, and continued nominal wage growth, particularly in the service sector.

And at this juncture, I believe markets are underestimating the threat of the July increase. With reports of a pause the predominant thought, many investors may have become complacent and are betting on a more expedient end to the cycle or even a shift into a rate cutting mindset. Commentary to the contrary in this upcoming meeting could, thus, result in a reversal in the current sentiment. This could hit the tech-heavy Nasdaq harder, considering its current run-up.

Looking ahead, I expect the economic data to continue coming in ahead of expectations. Though consumers are increasingly stretched, the state of their finances is holding up well due in part to continued nominal wage growth and an abundance of opportunities in the labor market. This enables them to spend their dollars on where it matters, such as in travel and entertainment. And if this continues, the current rate campaign is unlikely to reverse course.

Read the full article here